RBS 2009 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009138

The global automotive industry continues to face long-term structural

challenges of overcapacity, weakened consumer demand owing to

economic conditions, reduced credit availability and high input costs.

The global OEMs are experiencing changing demand patterns with a

greater focus on developing markets versus their established markets.

Shifting production capacity to lower cost overseas locations remains a

priority but one that risks labour force issues. The industry is also

challenged by increasingly stringent environmental legislation that is

forcing a shift to smaller, lower emission vehicles. In 2009 the automotive

industry benefited from considerable government support in the form of

direct intervention (US manufacturers) and other forms (for example, car

scrappage schemes). Whilst there are some emerging signs of recovery

and stability, albeit with volumes at historically low levels, the outlook

remains fragile as government support is withdrawn and underlying

demand is likely to remain subdued.

The portfolio has been reduced in size by a third since 31 December 2008

and whilst average credit quality was impacted by the restructuring of

the large US manufacturers at the start of 2009, this restructuring

provided a degree of stability to the portfolio that was largely

maintained for the remainder of the year. Impairment provisions to date

have not been material.

Credit risk continued

Credit risk assets*continued

Corporate sectors continued

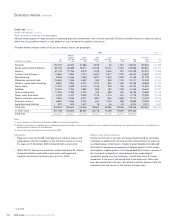

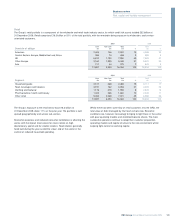

Transport and storage

The automotive, shipping and aviation portfolios form part of the transport

and storage industry sector, which stood at £46.2 billion at 31 December

2009, down 22% during the year. The remainder of the portfolio largely

comprises land-based freight, storage and logistics companies.

Automotive

Exposure to the automotive sector decreased from £13.3 billion at 31

December 2008 to £8.9 billion at 31 December 2009.

2009 2008

Core Non-Core Total Total

Segment £m £m £m % £m %

Original equipment manufacturers (OEMs) 1,204 60 1,264 14 2,681 20

Captive finance companies 609 84 693 8 1,131 9

Component suppliers 750 81 831 9 1,854 14

Retailers/services 4,040 766 4,806 54 5,099 38

Rental 1,150 147 1,297 15 2,533 19

7,753 1,138 8,891 100 13,298 100

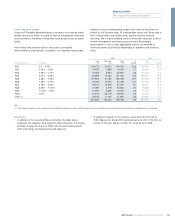

2009 2008

Core Non-Core Total Total

Domicile of obligor £m £m £m % £m %

Americas 1,325 402 1,727 19 3,520 26

Central Eastern Europe, Middle East and Africa 373 152 525 6 872 7

UK 3,530 426 3,956 45 3,884 29

Other Europe 1,949 97 2,046 23 4,098 31

Asia 576 61 637 7 924 7

7,753 1,138 8,891 100 13,298 100

* unaudited