RBS 2009 Annual Report Download - page 281

Download and view the complete annual report

Please find page 281 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

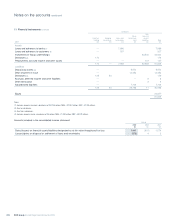

Financial statements

Notes on the accounts

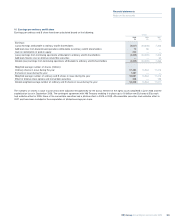

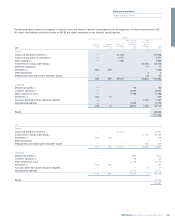

279RBS Group Annual Report and Accounts 2009

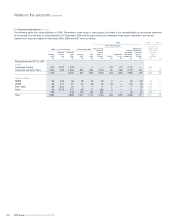

Valuation techniques

The Group uses a number of methodologies to determine the fair values

of financial instruments for which observable prices in active markets for

identical instruments are not available. These techniques include: relative

value methodologies based on observable prices for similar instruments;

present value approaches where future cash flows from the asset or

liability are estimated and then discounted using a risk-adjusted interest

rate; option pricing models (such as Black-Scholes or binomial option

pricing models) and simulation models such as Monte-Carlo.

The principal inputs to these valuation techniques are listed below.

Values between and beyond available data points are obtained by

interpolation and extrapolation. When utilising valuation techniques, the

fair value can be significantly affected by the choice of valuation model

and by underlying assumptions concerning factors such as the amounts

and timing of cash flows, discount rates and credit risk.

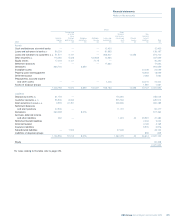

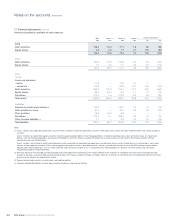

•Bond prices – quoted prices are generally available for government

bonds, certain corporate securities and some mortgage-related

products.

•Credit spreads – where available, these are derived from prices of

CDS or other credit based instruments, such as debt securities. For

others, credit spreads are obtained from pricing services.

•Interest rates – these are principally benchmark interest rates such

as the London Inter-Bank Offered Rate (LIBOR) and quoted interest

rates in the swap, bond and futures markets.

•Foreign currency exchange rates – there are observable markets

both for spot and forward contracts and futures in the world’s major

currencies.

•Equity and equity index prices – quoted prices are generally readily

available for equity shares listed on the world’s major stock

exchanges and for major indices on such shares.

•Commodity prices – many commodities are actively traded in spot

and forward contracts and futures on exchanges in London, New

York and other commercial centres.

•Price volatilities and correlations – volatility is a measure of the

tendency of a price to change with time. Correlation measures the

degree to which two or more prices or other variables are observed

to move together. If they move in the same direction there is positive

correlation; if they move in opposite directions there is negative

correlation. Volatility is a key input in valuing options and the

valuation of certain products such as derivatives with more than one

underlying variable that are correlation-dependent. Volatility and

correlation values are obtained from broker quotations, pricing

services or derived from option prices.

•Prepayment rates – the fair value of a financial instrument that can

be prepaid by the issuer or borrower differs from that of an

instrument that cannot be prepaid. In valuing prepayable instruments

that are not quoted in active markets, the Group considers the value

of the prepayment option.

•Counterparty credit spreads – adjustments are made to market

prices (or parameters) when the creditworthiness of the counterparty

differs from that of the assumed counterparty in the market price (or

parameters).

•Recovery rates/loss given default – these are used as an input to

valuation models and reserves for ABS and other credit products as

an indicator of severity of losses on default. Recovery rates are

primarily sourced from market data providers or inferred from

observable credit spreads.

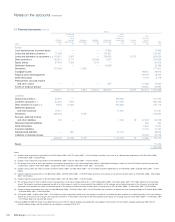

In order to determine a reliable fair value, where appropriate,

management applies valuation adjustments to the pricing information

gathered from the above sources. These adjustments reflect the Group’s

assessment of factors that market participants would consider in setting

a price, to the extent that these factors are not reflected in that pricing

information. Furthermore, on an ongoing basis, the Group assesses the

appropriateness of any model used. To the extent that the price

provided by internal models does not represent the fair value of the

instrument, for instance in highly stressed market conditions, the Group

makes adjustments to the model valuation to calibrate to other available

pricing sources. Where unobservable inputs are used, the Group may

determine a range of possible valuations derived from differing stress

scenarios to determine the sensitivity associated with the valuation.

When establishing the fair value of a financial instrument using a

valuation technique, the Group considers certain adjustments to the

modelled price which market participants would make when pricing that

instrument. Such adjustments include the credit quality of the

counterparty and adjustments to compensate for any known model

limitations.

On initial recognition of financial assets and liabilities valued using

valuation techniques incorporating information other than observable

market data, any difference between the transaction price and that

derived from the valuation technique is deferred. Such amounts are

recognised in profit or loss over the life of the transaction; when market

data become observable; or when the transaction matures or is closed

out as appropriate. At 31 December 2009, net gains of £204 million

(2008 – £102 million; 2007 – £72 million) were carried forward in the

balance sheet. During the year net gains of £127 million (2008 – £89

million; 2007 – £67 million) were deferred and £25 million (2008 – £65

million; 2007 – £10 million) recognised in the income statement.