RBS 2009 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009164

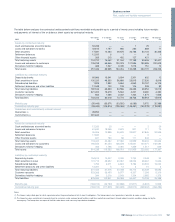

Market risk continued

The 2008 and 2009 data on trading VaR in the tables on the previous

page excludes exposures to super-senior tranches of asset backed

CDOs, as VaR does not produce an appropriate measure of risk for

these exposures due to the illiquidity and opaqueness of the pricing of

these instruments over an extended period. For these exposures, the

maximum potential loss is equal to the aggregate net exposure, which

was £910 million as at 31 December 2009.

The 2009 data in the tables on the previous page also excludes the

exposures relating to CDPCs from the end of August 2009 when they

were excluded from VaR and were capitalised under a Pillar II

approach.

RBS Sempra Commodities LLP (Sempra), the commodities-marketing

joint venture between RBS and Sempra Energy, was formed on 1 April

2008, and its trading risks were included in the disclosed VaR from that

date. Sempra is designated as Non-Core in the 2009 data.

The trading and non-trading VaR for 2007 is shown on the basis it was

previously disclosed at a 95% confidence level and using a normalised

scaling factor to convert to 99% confidence level.

Non trading VaR in the tables on the previous page does not include

structural interest rate risk which is covered on page 165.

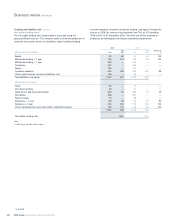

Back-testing, stress testing and sensitivity analysis

The Group undertakes a programme of daily back-testing, which compares

the actual profit or loss realised in trading activity to the VaR estimation. The

results of the back-testing process are one of the methods by which the

Group monitors the ongoing suitability of its VaR model.

The Group undertakes daily stress testing to identify the potential losses

in excess of VaR. Stress testing is used to calculate a range of trading

book exposures which result from exceptional, but plausible market

events. Stress testing measures the impact of abnormal changes in

market rates and prices on the fair value of the Group’s trading portfolios.

The Group calculates historical stress tests and hypothetical stress tests.

Historical stress tests calculate the loss that would be generated if the

market movements that occurred during historical market events were

repeated. Hypothetical stress tests calculate the loss that would be

generated if a specific set of adverse market movements were to occur.

Stress testing is also undertaken at key trading strategy level, for those

strategies where the associated market risks are not adequately

captured by VaR. Stress test exposures are discussed with senior

management and are reported to GRC, ERF and the Board. Breaches in

the Group’s market risk stress testing limits are monitored and reported.

In addition to VaR and stress testing, the Group calculates a wide range

of sensitivity and position risk measures, for example interest rate

ladders or option revaluation matrices. These measures provide valuable

additional controls, often at individual desk or strategy level.

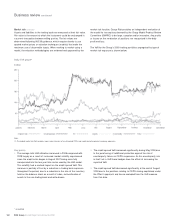

Model validation governance

Pricing models are developed and owned by the front office. Where

pricing models are used as the basis of books and records valuations,

they are all subject to independent review and sign-off. Models are

assessed by GMPRC as having either immaterial or material model risk

(valuation uncertainty arising from choice of modelling assumptions),

the assessment being made on the basis of expert judgement.

Those models assessed by the GMPRC as having material model risk

are prioritised for independent quantitative review. Independent

quantitative review aims to quantify model risk (i.e. the impact of missing

risk factors in the front office model or the possibility that we may be

mismarking these products relative to other market participants who may

be using an alternative model) by comparing model outputs against

alternative independently developed models. The results of independent

quantitative reviews are used by market risk to inform risk limits and by

finance to inform reserves. Governance over this process is provided by

GMPRC, a forum which brings together front office quantative analysts,

market risk, finance and QuaRC (Quantitative Research Centre, Group

Risk’s independent quantitative model review function). Risk (market risk,

incremental default risk, counterparty credit risk) models are developed

both within business units and by Group functions. Risk models are also

subject to independent review and sign-off. Meetings are held with the

FSA every quarter to discuss the traded market risk, including changes

in models, management, back testing results, other risks not included in

the VaR framework and other model performance statistics.

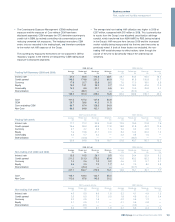

Risk control

All divisions that are exposed to market risk in the course of their

business are required to comply with the Group’s Market Risk Policy

Standards (MRPS). The main risk management tools are delegated

authorities, hard limits and discussion triggers, independent model

valuation, a robust and efficient risk system and timely and accurate

management information.

Limits form part of the dealing authorities and constitute one of the

cornerstones of the market risk management framework. Upon

notification of a limit breach, the appropriate body must take one of the

following actions:

•Instructions can be given to reduce positions so as to bring the

Group within the agreed limits;

•A temporary increase in the limit can be granted to pursue an

agreed short-term strategy; and

•A permanent increase in the limit can be granted if consistent with

the strategy and supported by the business and Risk Management.

Non-traded portfolios

Risks in non-traded portfolios mainly arise in retail and commercial

banking assets and liabilities and financial investments designated as

available-for-sale and held-to-maturity.

Group Treasury is responsible for setting and monitoring the adequacy and

effectiveness of management, using a framework that identifies, measures,

monitors and controls the underlying risk. GALCO approves the Group’s

non-traded market risk appetite, expressed as statistical and non-statistical

risk limits, which are delegated to the businesses responsible.