RBS 2009 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

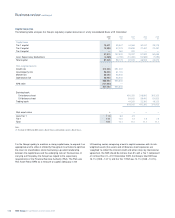

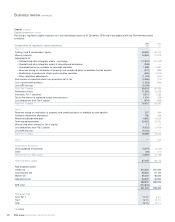

Business review

Risk, capital and liquidity management

Risk, capital and liquidity management

On pages 117 to 206 of the Business review certain information has

been audited and is part of the Group’s financial statements as

permitted by IFRS 7. Other disclosures are unaudited and labelled with

an asterisk (*). Key points within this section generally relate to the

Group before RFS Holdings minority interest.

Overview*

Conditions during the year continued to prove challenging as the

ongoing deterioration in economic conditions and financial markets seen

during 2008 continued into 2009. Market stress peaked during the first

quarter of 2009 with broad improvement since then. This reflects a

global effort by many governments and central banks to ease monetary

conditions, increase liquidity within the financial system and support

banks with a combination of increased capital, guarantees and

strengthened deposit insurance. One resulting benefit for banks

generally has been a significant improvement in the liquidity of money

and debt markets. At the same time, regulatory oversight of the banking

sector has increased globally and is expected to continue at a

heightened level.

More recently, the major economies have started to demonstrate a

gradually improving macroeconomic position, although conditions

remain fragile. Areas of particular uncertainty include possible effects

from governments ending their financial stimulus initiatives and central

banks moving to exit from positions of historically very low interest rates,

as well as reversing quantitative easing. These look likely to occur

against a backdrop of heightened personal and corporate insolvency as

well as rising unemployment.

The Group has been developing and adapting to an evolving economic

environment, against a background of the strategic review which

includes a clearly stated ambition to achieve standalone strength. The

core aims of the strategic plan are to improve the risk profile of the

Group and to reposition the balance sheet around the Group’s core

strengths. The Group level risk appetite statements and limits have been

reviewed to ensure they are in line with the strategy. Any potential areas

of misalignment between risk appetite and the Group strategy have

been discussed by the Executive Risk Forum and remediation plans

have been put in place.

Enhancements have been made to a number of the risk frameworks,

including:

•A new credit approval process has been introduced during the year,

based on a pairing of business and risk managers authorised to

approve credit. This replaced the former credit committee process;

•Exposure to higher risk countries has been reduced and a new risk

limits framework has been implemented across the Group;

•Single name and sector wide credit concentrations continue to

receive a high level of attention and further enhancements to the

frameworks were agreed in the fourth quarter of the year;

•In addition to the move to value-at-risk (VaR) based on a 99%

confidence level, from 95%, the Group has improved and

strengthened its market risk limit framework increasing the

transparency of market risk taken across the Group’s businesses in

both the trading and non-trading portfolios;

•The Group’s funding and liquidity profile is supported by explicit

targets and metrics to control the size and extent of both short-term

and long-term liquidity risk; and

•An improved reporting programme has been implemented to

increase transparency and improve the management of risk

exposures.

Credit impairments in 2009 were materially higher than the previous

year. As the year progressed, the level of impairments moderated, with

the highest quarterly charge incurred in the second quarter. It is

expected that the results for 2010 and 2011 will continue to be affected

by a heightened level of credit impairments as exposures in the Non-

Core division are managed down and the economic environment

continues to impact the Core business. The risk weightings applied to

assets are also expected to increase due to procyclicality and as a

result the amount of capital that banks generally are required to hold

will increase. Future regulatory changes are also expected to increase

the capital requirements of the banking sector. Against this background,

the Non-Core portfolio is reducing and the Group has materially

strengthened its capital base through the B share issuance in

December 2009.

117RBS Group Annual Report and Accounts 2009

* unaudited