RBS 2009 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

91RBS Group Annual Report and Accounts 2009

Business review

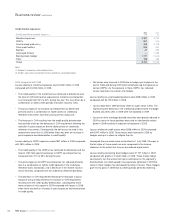

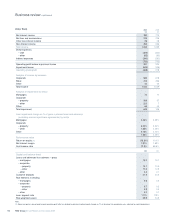

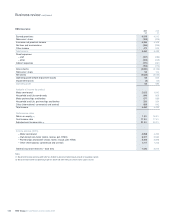

£bn £bn

Capital and balance sheet

Total assets 114.9 121.0

Loans and advances to customers – gross

– Banks and financial institutions 5.2 5.4

– Hotels and restaurants 5.6 6.1

– Housebuilding and construction 3.4 5.2

– Manufacturing 3.7 5.3

– Other 42.0 38.1

– Private sector education, health, social work, recreational and community services 7.4 7.4

– Property 28.0 31.8

– Wholesale and retail trade, repairs 7.8 9.1

– Asset and invoice finance 8.5 8.5

Customer deposits 87.8 82.0

Risk elements in lending 2.3 1.3

Loan:deposit ratio 126% 142%

Risk-weighted assets 90.2 85.7

Note:

(1) Return on equity is based on divisional operating profit after tax, divided by divisional notional equity (based on 8% of divisional risk-weighted assets, adjusted for capital deductions).

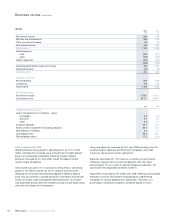

2009 compared with 2008

Operating profit of £1,125 million was £656 million lower than in 2008,

largely due to an increase of £608 million in impairments.

Net interest margin levels were rebuilt during the second half as asset

pricing was amended to reflect increased funding and credit costs. For

the year as a whole net interest margin was 18 basis points lower than

in 2008, reflecting higher funding costs and continued competitive

pricing for deposits.

Gross new lending to customers remained resilient in 2009, with a

noticeable acceleration of lending activity in the second half of the year.

However, as customers have deleveraged and turned increasingly to

capital markets, repayments have accelerated even more sharply. Loans

and advances to customers, therefore, declined by 5% to £111.5 billion.

Initiatives aimed at increasing customer deposits have been successful,

with balance growth of 7%, although margins declined as a result of

increased competition for balances.

Non-interest income was flat, with stable fee income from refinancing

and structuring activity.

A reduction in costs of 7% was driven by lower staff expenses as a

result of the Group’s restructuring programme, together with restraint on

discretionary spending levels.

Impairment losses increased substantially reflecting both a rise in the

number of corporate delinquencies requiring a specific impairment and

a higher charge to recognise losses not yet specifically identified.

Risk-weighted assets grew 5% despite the fall in customer lending,

reflecting the impact of procyclicality, which was most pronounced in

the first half of 2009.