RBS 2009 Annual Report Download - page 284

Download and view the complete annual report

Please find page 284 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Notes on the accounts continued

RBS Group Annual Report and Accounts 2009282

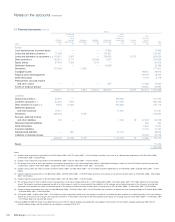

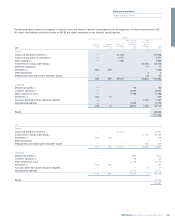

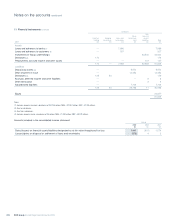

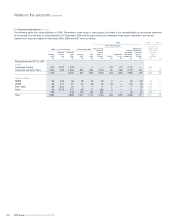

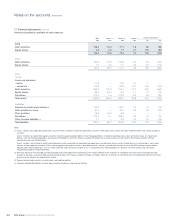

Total Level 1 Level 2 Level 3 Level 3 sensitivity (2)

2009 £bn £bn £bn £bn £m £m Level 3 valuation technique and related assumptions

Assets

Loans and advances:

– banks 45.4 — 45.4 — — — n/a

– customers 44.3 — 43.2 1.1 80 (40) Proprietary model: credit spreads, indices

Debt securities

Government 146.8 130.1 16.7 — — — n/a

RMBS 57.7 — 57.2 0.5 30 (10) Industry standard model: prepayment rates,

probability of default, loss severity and yield

CMBS 4.1 — 4.0 0.1 30 — n/a

CDOs 3.6 — 2.6 1.0 130 (80) Proprietary model: implied collateral valuation,

default rates, housing prices, correlation

CLOs 8.8 — 8.0 0.8 80 (50) Industry standard simulation model: credit

spreads, recovery rates, correlation

Other ABS 6.1 — 5.2 0.9 120 (40) Proprietary model: credit spreads,

Corporate 11.4 — 10.8 0.6 70 (20) Proprietary model: credit spreads

Other (3) 18.9 0.2 18.5 0.2 10 (30) Proprietary model: credit spreads

257.4 130.3 123.0 4.1 470 (230)

Equity shares 19.5 15.4 2.6 1.5 280 (220) Valuation statements: fund valuation

Derivatives

Foreign exchange 69.4 — 69.2 0.2 10 — Proprietary model: volatility, correlation

Interest rate 323.6 0.3 321.8 1.5 80 (100) Proprietary model: volatility, correlation

Equities 6.5 0.4 5.8 0.3 20 (20) Proprietary model; volatility, correlation,

dividends

Commodities 0.3 — 0.3 — — — n/a

Credit – APS 1.4 — — 1.4 1,370 (1,540) Proprietary model: correlation, expected losses,

recovery rates, credit spreads

Credit – other 40.3 0.1 37.2 3.0 420 (360) Proprietary, industry option and correlation

models: counterparty credit risk, correlation,

volatility

441.5 0.8 434.3 6.4 1,900 (2,020)

Total assets 808.1 146.5 648.5 13.1 2,730 (2,510)

Liabilities

Deposits:

– banks 53.6 — 53.6 — — —

n/a

– customers 61.4 — 61.3 0.1 — (10) Proprietary model: credit spreads correlation

Debt securities in issue 45.5 — 43.2 2.3 50 (10) Proprietary model: volatility, correlation,

Short positions 40.5 27.1 13.2 0.2 10 (20) Proprietary model: credit spreads, correlation

Derivatives

Foreign exchange 63.9 — 63.9 — — — n/a

Interest rate 311.4 0.1 310.5 0.8 40 (60) Proprietary model: volatility, correlation,

Equities 9.5 1.0 8.3 0.2 20 (70) Proprietary model: volatility, correlation

dividends

Commodities 0.2 — 0.2 — — — n/a

Credit 39.1 — 38.1 1.0 80 (100) Proprietary CVA model, industry option and

correlation models: counterparty credit risk,

correlation, volatility

424.1 1.1 421.0 2.0 140 (230)

Other financial liabilities (4) 1.3 — 1.3 — — — n/a

Total liabilities 626.4 28.2 593.6 4.6 200 (270)

11 Financial instruments continued

Valuation hierarchy

The tables below show the financial instruments carried at fair value by

hierarchy – level 1, level 2 and level 3. The valuation techniques, main

assumptions used in the valuation of these instruments and reasonably

possible increases or decreases in fair value based on reasonably

possible alternative assumptions for level 3 financial instruments are set

out below.