RBS 2009 Annual Report Download - page 289

Download and view the complete annual report

Please find page 289 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Financial statements

Notes on the accounts

287RBS Group Annual Report and Accounts 2009

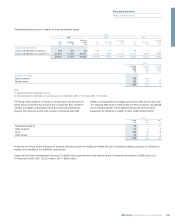

The Group has used the following reasonably possible alternative

assumptions in relation to those inputs that could have significant effect

on the valuation of the APS CDS:

•correlation: +/- 10%

•expected losses on covered assets that have triggered: +/- £1 billion

•range of possible recovery rates on non-triggered assets: +/- 10%

•credit spreads: +/- 10 basis points

Using the above reasonably possible alternative assumptions, the fair

value of the APS derivative could be higher by approximately £1,370

million or lower by approximately £1,540 million.

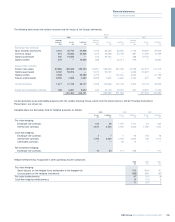

Credit derivatives – other

The Group’s other credit derivatives include vanilla and bespoke

portfolio tranches, gap risk products and certain other unique trades.

The bespoke portfolio tranches are synthetic tranches referenced to a

bespoke portfolio of corporate names on which the Group purchases

credit protection. Bespoke portfolio tranches are valued using Gaussian

Copula, a standard method which uses observable market inputs (credit

spreads, index tranche prices and recovery rates) to generate an output

price for the tranche via a mapping methodology. In essence this

method takes the expected loss of the tranche expressed as a fraction

of the expected loss of the whole underlying portfolio and calculates

which detachment point on the liquid index, and hence which

correlation level, coincides with this expected loss fraction. Where the

inputs into this valuation technique are observable in the market,

bespoke tranches are considered to be level 2 assets. Where inputs are

not observable, bespoke tranches are considered to be level 3 assets.

However, all transactions executed with a CDPC counterparty are

considered level 3 as the counterparty credit risk assessment is a

significant component of these valuations.

Gap risk products are leveraged trades, with the counterparty’s

potential loss capped at the amount of the initial principal invested. Gap

risk is the probability that the market will move discontinuously too quickly

to exit a portfolio and return the principal to the counterparty without

incurring losses, should an unwind event be triggered. This optionality is

embedded within these portfolio structures and is very rarely traded

outright in the market. Gap risk is not observable in the markets and, as

such, these structures are deemed to be level 3 instruments.

Other unique trades are valued using a specialised model for each

instrument and the same market data inputs as all other trades where

applicable. By their nature, the valuation is also driven by a variety of

other model inputs, many of which are unobservable in the market.

Where these instruments have embedded optionality it is valued using a

variation of the Black-Scholes option pricing formula, and where they

have correlation exposure it is valued using a variant of the Gaussian

Copula model. The volatility or unique correlation inputs required to

value these products are generally unobservable and the instruments

are therefore deemed to be level 3 instruments.

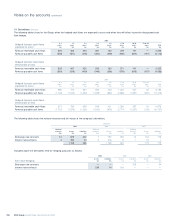

Equity derivatives

Equity derivative products are split into equity exotic derivatives and

equity hybrids. Equity exotic derivatives have payouts based on the

performance of one or more stocks, equity funds or indices. Most

payouts are based on the performance of a single asset and are valued

using observable market option data. Unobservable equity derivative

trades are typically complex basket options on stocks. Such basket

option payouts depend on the performance of more than one equity

asset and require correlations for their valuation. Valuation is then

performed using industry standard valuation models, with unobservable

correlation inputs calculated by reference to correlations observed

between similar underlyings.

Equity hybrids have payouts based on the performance of a basket of

underlyings where the underlyings are from different asset classes.

Correlations between these different underlyings are typically

unobservable with no market information for closely related assets

available. Where no market for the correlation input exists, these inputs

are based on historical time series.

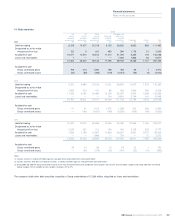

Interest rate and commodity derivatives

Interest rate and commodity options provide a payout (or series of

payouts) linked to the performance of one or more underlying, including

interest rates, foreign exchange rates and commodities.

Exotic options do not trade in active markets except in a small number

of cases. Consequently, the Group uses models to determine fair value

using valuation techniques typical for the industry. These techniques can

be divided, firstly, into modelling approaches and, secondly, into

methods of assessing appropriate levels for model inputs. The Group

uses a variety of proprietary models for valuing exotic trades.

Exotic valuation inputs include correlation between interest rates, foreign

exchange rates and commodity prices. Correlations for more liquid rate

pairs are valued using independently sourced consensus pricing levels.

Where a consensus pricing benchmark is unavailable, these instruments

are categorised as level 3.

Debt securities in issue

The carrying value of debt securities in issue is represented partly by

underlying cash and partly through a derivative component. The

classification of the amount in level 3 is driven by the derivative

component and not by the cash element.

Other financial instruments

Other than the portfolios discussed above, there are other financial

instruments which are held at fair value determined from data which are

not market observable, or incorporating material adjustments to market

observed data. These include subordinated liabilities and write downs

relating to undrawn syndicated loan facilities.