RBS 2009 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009132

Credit risk continued

Credit risk assets*continued

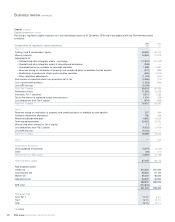

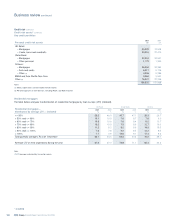

Asset quality by industry and geography

Industry analysis plays an important part in assessing potential concentration risk in the loan portfolio. Particular attention is given to industry sectors

where the Group believes there is a high degree of risk or potential for volatility in the future.

The table below analyses credit risk assets by industry sector and geography.

2009 2008

Western

Europe North Asia Latin of which

UK (excl. UK) America Pacific America Other (1) Total Core Total

Industry sector £m £m £m £m £m £m £m £m £m

Personal 120,720 23,530 37,680 2,948 63 1,361 186,302 165,562 197,888

Banks and financial institutions 38,775 66,698 18,817 13,158 10,216 5,305 152,969 133,900 180,504

Property 61,779 27,736 8,315 2,478 2,924 507 103,739 57,073 112,980

Transport and storage (2) 14,565 7,954 7,514 5,841 2,917 7,370 46,161 30,863 58,995

Manufacturing 9,309 14,646 7,965 3,627 1,643 3,948 41,138 31,199 67,846

Wholesale and retail trade 15,584 7,458 5,497 945 829 1,704 32,017 25,180 35,180

Telecom, media and technology 8,956 7,956 5,312 2,232 804 1,528 26,788 18,554 42,374

Public sector 11,091 4,448 6,016 2,109 279 760 24,703 21,823 39,890

Building 10,303 7,494 1,852 836 183 1,098 21,766 16,642 29,297

Tourism and leisure 11,396 3,268 2,700 755 586 481 19,186 15,583 19,528

Power, water and waste 4,745 6,197 3,502 1,179 1,215 941 17,779 12,055 26,628

Natural resources and nuclear 2,554 3,546 5,511 1,861 844 2,895 17,211 12,479 25,318

Business services 8,981 2,056 2,324 675 1,029 588 15,653 13,395 14,497

Agriculture and fisheries 921 618 1,671 18 64 82 3,374 3,214 3,951

2009 Total 319,679 183,605 114,676 38,662 23,596 28,568 708,786 557,522 854,876

of which Core 271,758 133,824 89,487 28,718 14,048 19,687 557,522

2008 Total 326,639 225,870 178,139 56,074 31,235 36,919 854,876

Notes:

(1) ‘Other’ comprises Central and Eastern Europe, Middle East, Central Asia and Africa.

(2) Excludes net investment in operating leases in Shipping and Aviation portfolios as they are accounted for as part of property, plant and equipment; however operating leases are included in the

monitoring and management of these portfolios.

(3) Certain sector and sub-sector classes were refined in 2009.

Key points

•Exposures have decreased materially across industry sectors and

geographies, with the exception of the UK where exposure is only

2% lower at 31 December 2009 compared with a year earlier.

•Within the UK, exposure to corporate sectors was down 8%. Banks,

financial institutions and public sector were unchanged and

exposure to personal customers was up 6% in 2009.

Single name concentrations

During the first half of the year, the Group implemented an enhanced

framework to address the risk arising from concentrations of exposure

to related groups of borrowers. Despite market illiquidity that reduced

the scope for exposure management strategies against certain assets,

and negative credit migration, that created additional cases in excess of

the framework’s parameters, some progress was made against

exceptions arising from the framework. Overall there were 9% fewer

exceptions at the end of the period than at the beginning. Plans have

been developed and continue to be refined to deliver alignment with the

framework over the course of the Group’s strategic plan.

* unaudited