RBS 2009 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

89RBS Group Annual Report and Accounts 2009

Business review

2009 compared with 2008

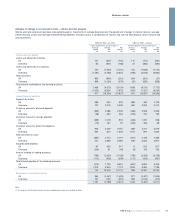

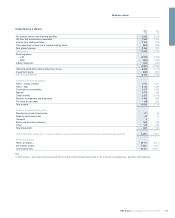

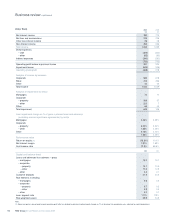

Operating profit of £229 million was £494 million lower than in 2008.

Profit before impairments was up £166 million or 10%, but impairments

rose by £660 million as the economic environment deteriorated, albeit

with signs of conditions stabilising in the second half of the year.

The division has focused in 2009 on growing secured lending to meet

its Government targets while at the same time building customer

deposits, thereby reducing the Group’s reliance on wholesale funding.

Loans and advances to customers grew 10%, with a change in mix from

unsecured to secured as the Group sought actively to reduce its risk

profile, with 15% growth in mortgage lending and an 8% reduction in

unsecured lending.

•Mortgage growth was due to good retention of existing customers

and new business sourced predominantly from the existing customer

base. Gross mortgage lending market share increased to 12% from

7% in 2008, with the Group on track to exceed its Government

targets on net lending by £3 billion.

•Customer deposits grew 11% on 2008 reflecting the strength of the

UK Retail customer franchise, which outperformed the market in an

increasingly competitive environment. Savings balances grew by £6

billion or 11% and account acquisition saw a 20% increase, with 2.2

million accounts opened. Personal current account balances

increased by 12% on 2008 with a 3% growth in accounts to 12.8

million.

Net interest income increased significantly by 8% to £3,452 million,

driven by strong balance sheet growth. Net interest margin was flat at

3.59%, with decreasing liability margins in the face of stiff competition

for deposits offsetting wider asset margins. The growth in mortgages

and the reduction in higher margin unsecured balances also had a

negative impact on the blended net interest margin.

Non-interest income declined 15% to £1,495 million, principally

reflecting the withdrawal of the single premium payment protection

insurance product and the restructuring of current account overdraft

fees in the final quarter of 2009, with the annualised impact of the

overdraft fee restructuring further affecting income in 2010. The weak

economic environment presented little opportunity in 2009 to grow

credit card, private banking and bancassurance fees.

Expenses decreased by 5%, with the cost:income ratio improving from

62% to 60%.

•Direct staff costs declined by 9%, as the division benefited from

strong cost control, a focus on process re-engineering and a 10%

reduction in headcount.

•RBS continues to progress towards a more convenient, lower cost

operating model, with over 4 million active users of online banking

and a record share of new sales achieved through direct channels.

More than 5.5 million accounts have switched to paperless

statements and 254 branches now utilise automated cash deposit

machines.

Impairment losses increased 65% to £1,679 million reflecting the

deterioration in the economic environment, and its impact on customer

finances.

•The mortgage impairment charge was £124 million (2008 – £31

million) on a total book of £83.2 billion. Mortgage arrears rates

stabilised in the second half of 2009 and remain well below the

industry average, as reported by the Council of Mortgage Lenders.

Repossessions show only a small increase on 2008, as the Group

continues to support customers facing financial difficulties.

•The unsecured lending impairment charge was £1,555 million (2008

– £988 million) on a book of £19.8 billion. Industry benchmarks for

cards arrears showed a slightly improving trend in the final quarter

of 2009, which is consistent with the Group’s experience. RBS

continues to perform better than the market on arrears.

Risk weighted assets increased by 12% to £51.3 billion due to higher

lending and the upward pressure from procyclicality, more than

offsetting the adoption of a through-the-cycle loss given default

approach for mortgages.