RBS 2009 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009144

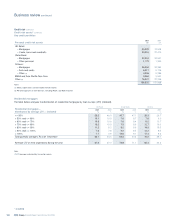

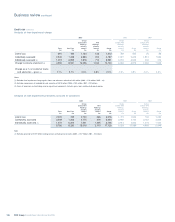

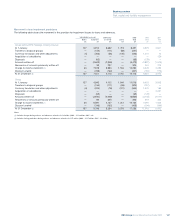

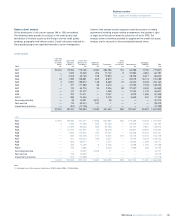

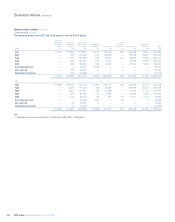

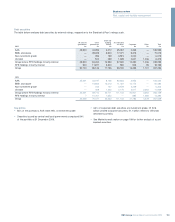

Credit risk continued

Impairment loss provision methodology

Provisions for impairment losses are assessed under three categories:

•Individually assessed provisions: provisions required for individually

significant impaired assets which are assessed on a case by case

basis, taking into account the financial condition of the counterparty

and any guarantee and other collateral held after being stressed for

downside risk. This incorporates an estimate of the discounted value

of any recoveries and realisation of security or collateral. The asset

continues to be assessed on an individual basis until it is repaid in

full, transferred to the performing portfolio or written-off;

•Collectively assessed provisions: provisions on impaired credits

below an agreed threshold which are assessed on a portfolio basis,

to reflect the homogeneous nature of the assets, such as credit

cards or personal loans. The provision is determined from a

quantitative review of the relevant portfolio, taking account of the

level of arrears, security and average loss experience over the

recovery period; and

•Latent loss provisions: provisions held against impairments in the

performing portfolio that have been incurred as a result of events

occuring before the balance sheet date but which have not been

identified at the balance sheet date. The Group has developed

methodologies to estimate latent loss provisions that reflect:

– Historical loss experience adjusted where appropriate, in the light

of current economic and credit conditions; and

– The period (‘emergence period’) between an impairment event

occurring and a loan being identified and reported as impaired.

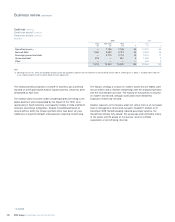

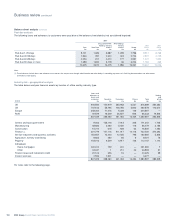

Recoverable cash flows are estimated using two parameters: loss

given default (LGD) – this is the estimated loss amount, expressed as

a percentage, that will be incurred if the borrower defaults; and the

probability that the borrower will default (PD).

Emergence periods are estimated at a portfolio level and reflect the

portfolio product characteristics such as a coupon period and

repayment terms, and the duration of the administrative process

required to report and identify an impaired loan as such. Emergence

periods vary across different portfolios from two to 225 days. They

are based on actual experience within the particular portfolio and are

reviewed regularly.

The Group’s retail business segment their performing loan books into

homogenous portfolios such as mortgages, credit cards or

unsecured loans, to reflect their different credit characteristics. Latent

provisions are computed by applying portfolio-level LGDs, PDs and

emergence periods. The wholesale calculation is based on similar

principles but there is no segmentation into portfolios: PDs and LGDs

are calculated on an individual basis.

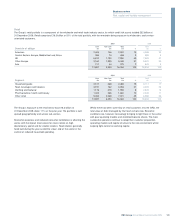

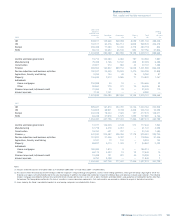

Provision analysis

The Group’s consumer portfolios, which consist of high volume, small

value credits, have highly efficient largely automated processes for

identifying problem credits and very short timescales, typically three

months, before resolution or adoption of various recovery methods.

Corporate portfolios consist of higher value, lower volume credits, which

tend to be structured to meet individual customer requirements.

Provisions are assessed on a case by case basis by experienced

specialists with input from professional valuers and accountants. The

Group operates a transparent provisions governance framework, setting

thresholds to trigger enhanced oversight and challenge.