RBS 2009 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review

Risk, capital and liquidity management

159RBS Group Annual Report and Accounts 2009

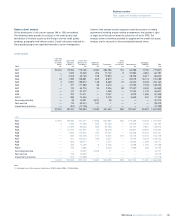

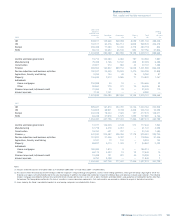

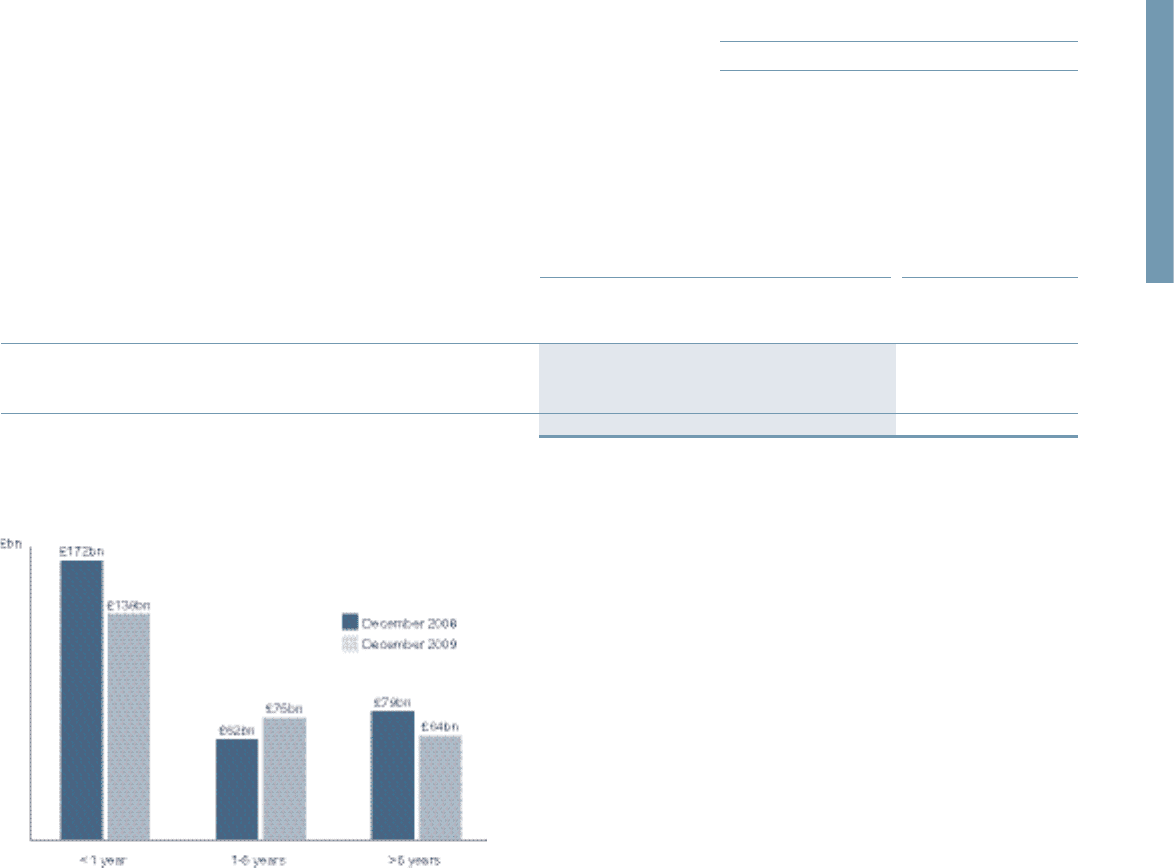

Wholesale funding maturity profile

Outlook for 2010*

Whilst there have been improvements in the state of the global economy

over the course of 2009, the outlook for 2010 remains uncertain. In line

with meeting the objectives of the strategic plan, the Group is actively

focusing on closing the customer funding gap, continuing to exit Non-

Core businesses and focusing on reducing undrawn and contingent

commitments. This will reduce the absolute need for wholesale funding

with the Group targeting £150 billion by 2013. In addition, the Group will

continue to make progress in terming out its remaining wholesale

funding. The Group will continue to reduce reliance on government

supported schemes and be governed by the state of the markets and

economies in which it operates. These strategies will ensure that the

Group will be more resilient to any further disruptions in the market and

will be better placed to take advantage of favourable trading conditions

as they return.

Regulatory environment*

The Group operates in multiple jurisdictions across the globe and is

subject to a number of regulatory regimes. The Group’s lead regulator is

the UK FSA, with other authorities such as the De Nederlandsche Bank

and the US Federal Reserve Bank playing key roles. The liquidity

framework applied by the FSA is the Sterling Stock regime. In line with

the FSA policy statement PS09/16, the Group will be subject to a new

liquidity risk regulatory framework in the future. The Group has been

working towards this new framework and will meet the requirements as

they come into force.

In the US the Group is required to meet the liquidity requirements set

out by all relevant regulatory authorities, including the Federal Reserve

Bank, Office of the Comptroller of the Currency, Federal Deposit

Insurance Corporation and Financial Industry Regulatory Authority. In

the Netherlands, ABN AMRO is subject the De Nederlandsche Bank

liquidity regulation regime.

2009 2008

Debt

securities Subordinated

in issue debt Total Total

£m £m £m % £m %

Less than one year 136,901 2,144 139,045 50.0 172,234 55.0

1-5 years 70,437 4,235 74,672 26.9 61,842 19.8

More than 5 years 38,991 25,159 64,150 23.1 79,060 25.2

246,329 31,538 277,867 100.0 313,136 100.0

The table below shows the maturity profile of the Group’s debt securities

in issue and subordinated debt. The composition of the profile reflects

the increased proportion of the Group’s debt securities in issue of

greater than 1 year maturity. Debt securities with a remaining maturity of

less than 1 year has reduced by £33 billion to £139 billion at 31

December 2009 (2008 – £172 billion). The proportion of debt securities

in issue with remaining maturity greater than 1 year has increased from

45% at 31 December 2008 to 50% at 31 December 2009.

* unaudited