RBS 2009 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2009 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

|

|

Business review continued

RBS Group Annual Report and Accounts 2009156

Funding and liquidity risk continued

Monitoring continued

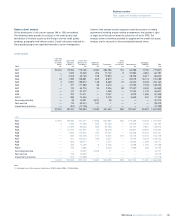

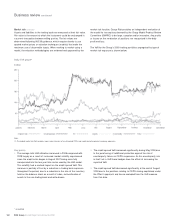

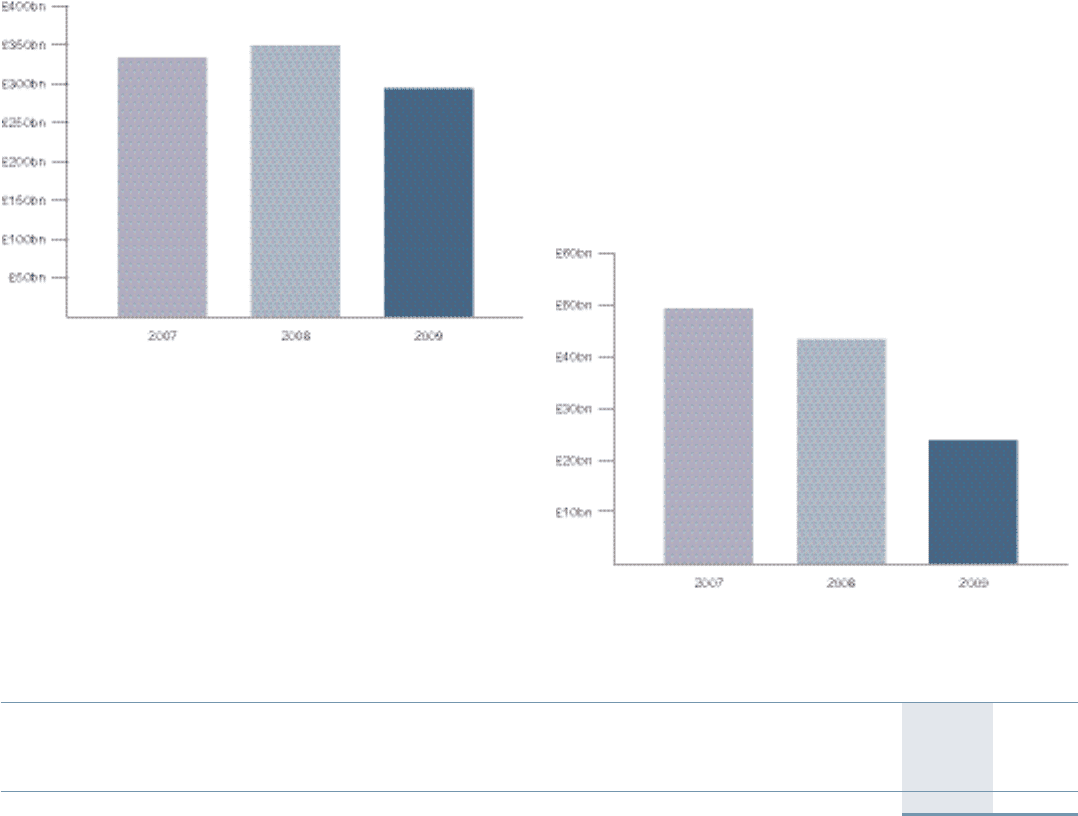

Undrawn commitments: The Group has been actively managing down

the amount of undrawn commitments that it is exposed to. Undrawn

commitments decreased from £349 billion at 31 December 2008 to

£289 billion at 31 December 2009.

Repo Agreements: At 31 December 2009 the Group had £68 billion of

customer secured funding and £38 billion of bank secured funding,

which includes borrowing using central bank funding schemes. With

markets continuing to stabilise through the course of 2009, the Group

has significantly reduced its reliance on secured funding from central

bank liquidity schemes.

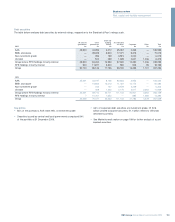

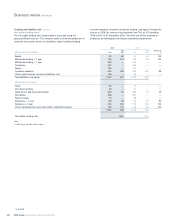

Liquidity reserves: The total stock of liquid assets has increased by

£81 billion during 2009 from £90 billion at 31 December 2008 to

£171 billion at 31 December 2009; this reflects the injection of

£25.5 billion of B shares at the end of December 2009 provided as

treasury bills and cash. The Group is targeting a liquidity pool of £150

billion by 2013. The table below shows the breakdown of these assets.

In addition to available liquid assets, the Group has a pool of

unencumbered assets that are available for securitisation to raise funds

if and when required.

The types of assets which can be used in securitisation include lending

assets, and the Group benefits from not having encumbered significant

amounts of lending assets historically.

Conduit commitments: The Group has taken additional measures to

improve the balance sheet structure. One area of focus has been

reducing the size of the multi-seller conduits business, which relies

upon funding assets through the issuance of short term asset-backed

commercial paper. Total facilities have declined by £17.9 billion to £25.0

billion at 31 December 2009. This has reduced the liquidity risk to the

Group through the commitments provided for this type of business.

2009 2008

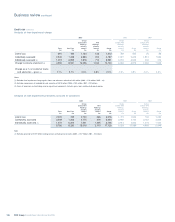

Liquidity reserves £m £m

Government securities 57,407 27,303

Cash and central bank balances 51,500 11,830

Unencumbered collateral (1) 42,055 30,054

Other liquid assets 19,699 20,647

Total liquidity reserve 170,661 89,834

Note:

(1) Includes secured assets which are eligible for discounting at central banks.

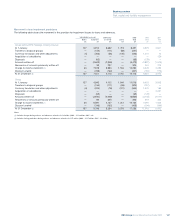

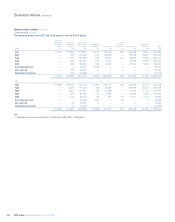

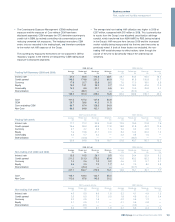

Funding profile

The contractual maturity of on balance sheet assets and liabilities,

shown in the tables overleaf, highlight the maturity transformation which

underpins the role of banks to lend longer-term but funded

predominantly by short-term liabilities such as customer deposits. This

is achieved through the diversified funding franchise of the Group

across an extensive retail, wealth and SME customer base, and across

a wide geographic network. In practice, the behavioural profile of many

assets and liabilities exhibit greater stability and longer maturity than the

contractual maturity. The Group models the behavioural maturity of

liabilities so that it can target a diversified and stable funding base.