RBS 2010 Annual Report Download

Download and view the complete annual report

Please find the complete 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

rbs.com

Annual Report and Accounts 2010

Table of contents

-

Page 1

Annual Report and Accounts 2010 rbs.com -

Page 2

... Our approach to risk management 32 34 36 38 40 41 Divisional review UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Global Banking & Markets RBS Insurance Business Services and Central Functions Non-Core Division Asset Protection Scheme (APS) 42 44... -

Page 3

...(1) Group operating profit/(loss) before tax, amortisation of purchased intangible assets, integration and restructuring costs, gain on redemption of own debt, strategic disposals, bonus tax, Asset Protection Scheme credit default swap - fair value changes, gains on pensions curtailment, write-down... -

Page 4

... our share of the mortgage and savings markets in the UK, with account numbers rising by 44,000 and 579,000, respectively. We are investing heavily in our core businesses, with a strong emphasis on serving customers better and improving our efficiency. Economic backdrop - getting better The global... -

Page 5

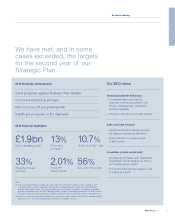

... programmes. Our annual Sustainability Report contains extensive information on our activities in this key area for us in the UK, USA, India and many other countries where we operate. Value for our shareholders It is vital that we make a proper financial return on the large amounts of new capital... -

Page 6

...-to-deposit ratio is 117%, down from 154% at peak and our Core businesses now take in over £1 of deposits for every £1 of loans Two years on from the global financial crisis, our recovery is ahead of schedule. In 2010 we made big strides in risk reduction and an early return to operating profits... -

Page 7

... itself. 2010 results were a large improvement on 2009 and our budgets for the year. At Group level RBS posted £1.9 billion of operating profits, excluding fair value of own debt (from a £6.1 billion loss in 2009). It was only after the post tax effect of APS (£1.1 billion) that we reported a net... -

Page 8

... in 2010, reflecting improvements in the economic environment. Impairments fell in all core businesses, except Ulster Bank, where asset default levels and loss rates remained high in both the retail and corporate portfolios, reflecting difficult economic conditions in Ireland. We currently expect... -

Page 9

... system. We want to put our balance sheet on a more secure footing by lending only as much as we have in deposits. We want to reduce our reliance on short-term money market funding to make our balance sheet less volatile. 10.7% >8% 4%(5) worst point 2009 2010 154%(6) 135% Loan:deposit ratio... -

Page 10

Our business and our strategy Our approach to business Progress on our strategic plan Our core businesses The economic environment 8 RBS Group 2010 -

Page 11

... risk management Our over-riding focus is on achieving three things: to serve customers well; to restore the Bank to undoubted standalone strength; and to rebuild sustainable value for all shareholders. In the second year of our five-year plan, we made progress on all three counts. RBS Group 2010... -

Page 12

...protects our reputation We work within all relevant laws and regulations We are a responsible and engaged member of the community We conduct our business in a sustainable manner We deliver essential customer services and critical business processes at all times People We value our people We recruit... -

Page 13

... and data We operate our processes, systems and controls to minimise loss from fraud or error Finances We manage our finances carefully We use the Group's capital and resources efficiently We account for and report our transactions properly Risk We understand and manage the risks we are taking... -

Page 14

...businesses and asset portfolios while maximising the value obtained for the Group. RBS management hallmarks to include an open, investorfriendly approach, discipline and proven execution effectiveness, strong risk management and central focus on the customer Publish targets for risk/return balance... -

Page 15

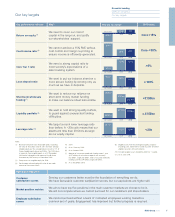

... strongest global peers Group loan:deposit ratio of c.100% Short-term wholesale funding 8% Retail and commercial businesses generated around 51% of the Core operating profit for 2010, moving towards the achievement of... -

Page 16

...Loan:deposit ratio (%) UK Corporate We are the leading provider of banking, finance and risk management services to the corporate and SME sector. We offer a full range of banking products and related financial services. Return on equity (%) Cost:income ratio (%) Loan:deposit ratio (%) 2009 2010... -

Page 17

... top five banks in New England. Return on equity (%) Cost:income ratio (%) Loan:deposit ratio (%) Global Banking & Markets We provide financing, risk management and advisory services to major corporations, financial institutions and public sector clients in 39 countries. RBS Insurance We sell and... -

Page 18

...cent in 2009. However, a fall in activity in the final quarter of 2010 served as a timely reminder that, while conditions are generally improving, the recovery is fragile. The recovery has helped many of our customers. Company trading profits grew for the first time since 2008. The unemployment rate... -

Page 19

...to the Plan. These are to: Operating model The risk and liquidity balance sheet management strategies are owned and set by the Group's Board of directors, and implemented by executive management led by the Group Chief Executive. A number of committees supports the execution of the business plan and... -

Page 20

... centrally-managed liquidity portfolio (£155 billion). We have continued to enhance our market risk management framework. We have reduced trading and banking book exposures (with asset sales and write-downs within Non-Core and banking book available-for-sale assets in Core). In our motor business... -

Page 21

.... Volatile funding position caused by the uncertainty of future investment returns and the projected value of schemes' liabilities. The economic environment improved but continued to impact the level of operational risk in areas such as the scale of structural change occurring across the Group... -

Page 22

Divisional review UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Global Banking & Markets RBS Insurance 20 RBS Group 2010 -

Page 23

...Core business is an asset to our customers, shareholders and risk profile - even before cross-business synergies are taken into account. The changes we are making to strengthen the Core business further can drive RBS to success as a leading bank in its markets for many years to come. RBS Group 2010... -

Page 24

... account against the progress we make, publishing an independentlyassured report on our performance every six months. 10% growth in customer deposits £1,372m operating profit Return on equity (%) Cost:income (%) Loan:deposit ratio (%) 2010 2013 target 18 >15 52 c.50 110 -

Page 25

...2011 to be another challenging year but we know that we will succeed as a business by helping our customers through good times and bad. Our commitment to becoming Britain's most Helpful and Sustainable Bank is a long-term one and we are confident we are creating a new kind of retail bank. RBS Group... -

Page 26

... costs. Helping businesses to start-up and grow We know that new businesses are vital to the recovering UK economy. In 2010, we opened on average more than 2,200 start-up accounts per week. Each one benefits from free transactional banking services in their first two years of operation. We launched... -

Page 27

... 5,000 loans to UK businesses each week. Our approval rate remains high: we continue to accept over 85% of the credit applications we receive. For the period from March 2010 to February 2011, RBS Group had agreed to make £50 billion of gross new lending facilities available to customers through its... -

Page 28

... Rory Tapner Chief Executive, Wealth Performance highlights Net interest income Non-interest income Total income Expenses Operating profit before impairment losses Impairment losses Operating profit Risk-weighted assets (£bn) Net interest margin Cost:income ratio Loan:deposit ratio 2010 £m 2009... -

Page 29

...Service awards, with a Jersey employee winning 'Frontline Professional of the Year'. In addition, two RBS International products, Autopilot and Navigator, won the Innovation Award in the 2010 Investment Life and Pensions Moneyfacts awards. Supporting good causes In 2010, the Coutts Charitable Trust... -

Page 30

...Group. Leveraging our global network GTS processes over 4.6 billion worldwide payments per year in 43 different currencies and we administer 4,600 global trade transactions each day. We use our international branch network to help customers do more business in more countries. We established a new UK... -

Page 31

... RMB accounts, currency exchange and trade finance services. For financial institutions, we unveiled the new Euro Trade Deduct product that maximises the benefits available from our cash and trade services. The launch of the RBS SWIFT Service Bureau throughout our Global Payments network enables... -

Page 32

...debt problems; and • local support, including no branch closures, a community fund and a 'Give a Day' volunteering programme. 8% increase in customer deposit balances in constant currencies 45 branches opened on Saturday for the first time Return on equity (%) Cost:income ratio (%) Loan:deposit... -

Page 33

... about what customers can expect concerning the costs, terms and conditions of credit and the factors that influence the price of a loan; and • understanding and support for businesses, including two-year free transactional banking for start-ups and an on-line business support programme. We are... -

Page 34

...make payments. We also Performance highlights Net interest income Non-interest income Total income Expenses Operating profit before impairment losses Impairment losses Operating profit/(loss) Risk-weighted assets (£bn) Return on equity Net interest margin Cost:income ratio Loan:deposit ratio 2010... -

Page 35

... sale to Advent International and Bain Capital, RBS will retain a 19.9% stake in the business, and can refer its customers to them for global merchant products and services. In May 2010, we also completed the exit of our joint arrangement with Kroger Personal Finance. Strengthening risk management... -

Page 36

...of own debt Fair value of own debt Operating profit Risk-weighted assets (£bn) Return on equity Net interest margin Cost:income ratio Loan:deposit ratio 2010 £m 2009 £m "Only by truly understanding our clients' needs can we apply our expertise to its best effect. That is why long-term customer... -

Page 37

...for derivatives (2010 Risk Interdealer Poll). Our debt capital markets business was voted Euromoney Best Debt House in the UK and the Netherlands. The Banker magazine gave us the Deal of the Year award for equities and sovereign bonds in Europe, financial institutions in the Middle East and loans in... -

Page 38

...in our underlying financial performance in the final quarter. 2009 £m Performance highlights Insurance net premium income Total income Expenses Net claims Impairment losses Investment income Operating (loss)/profit Return on equity Expense ratio Combined operating ratio 2010 £m 4,311 4,092 (703... -

Page 39

...on issues such as the risks of flood. Our dedication to customers, innovative products and hard working employees was recognised through a variety of awards in 2010. We received three 'Your Money' awards, with Direct Line winning for the Best Online Travel Insurance, Churchill for Best Pet Insurance... -

Page 40

...helped to launch similar products across other areas of the Group. Technology Services runs a programme to deliver innovative solutions, which includes building its own RBS 'App Store' to develop new business applications that boost productivity and enhance customer value. Managing operational risks... -

Page 41

... Finance Our Group Strategy and Corporate Finance team supports the Chief Executive, Chief Financial Officer and the Executive Committee in the development of the Group's strategy. Its objective is to ensure that the Group has the right portfolio of businesses, active in the right markets, supported... -

Page 42

...Asset Management business and for our Invoice Finance businesses in Germany and France. We completed the transfer of assets in six Asian countries to ANZ Group. 62% fall in operating losses 4 wholesale country exits in the year • Portfolio & Banking agreed deals to dispose of non-core portfolio... -

Page 43

... Plan (2012-13), subject to regulatory approval. Rory Cullinan Head of Non-Core Division Maximising shareholder value We achieved a significant reduction in the division's operating loss from £14.6 billion in 2009 to £5.5 billion, largely due to improvements in income from trading activities... -

Page 44

Sustainability 42 RBS Group 2010 -

Page 45

... sustainability In addition, we have a number of targeted community programmes that enable us to enhance our contribution to society. We aim to invest Group resources to maximise our impact, creating real and sustainable benefits in the communities in which we operate. RBS Group 2010 43 -

Page 46

... Chief Executive Officers of a number of our divisions. The GSC reviews the Group's overall sustainability strategy, values and policies. The Group Sustainability Forum is a network of senior managers from each division that makes sure we put into practice the priorities the GSC sets. The executive... -

Page 47

...12-19 year olds. The 2nd annual RBS Personal Finance Education Awards for Schools recognised the 2010 achievements of primary and secondary schools. Safety and security Protecting the security of our customers' money and data is a fundamental responsibility of the Group. We have continued to invest... -

Page 48

... in during work time. We run the activities through nine charities so that our employees can deliver the skills, services or fundraising that they need. This year 4,100 employees engaged in 225 activities. Our Global Banking and Markets division launched a new, bespoke volunteering programme across... -

Page 49

...in. The Group supported those efforts financially and by giving employees almost 170,000 hours off work to volunteer. Highlights of how we focus action across our businesses Fair banking Products and services The Group Customer Charter set out 14 clear commitments to our UK retail customers in 2010... -

Page 50

Report and accounts 48 RBS Group 2010 -

Page 51

... review 50 52 53 54 55 56 57 62 77 Presentation of information Forward-looking statements Description of business Competition Risk factors Key financials Summary consolidated income statement Analysis of results Divisional performance 106 Consolidated balance sheet 111 Cash flow 112 Capital... -

Page 52

... report as it more closely reflects the basis on which the Group is managed. 'UK' in this context includes domestic transactions and transactions conducted through the offices in the UK which service international banking transactions. The results, assets and liabilities of individual business units... -

Page 53

... costs; gain on redemption of own debt; strategic disposals; bonus tax; Asset Protection Scheme credit default swap - fair value changes; gains on pensions curtailment; write-down of goodwill and other intangible assets; and other Consortium Members' interest in shared assets. RBS Group 2010 51 -

Page 54

...; general operational risks; insurance claims; reputational risk; general geopolitical and economic conditions in the UK and in other countries in which the Group has significant business activities or investments, including the United States; the ability to achieve revenue benefits and cost savings... -

Page 55

... and equity financing, risk management and investment services to its customers. The division is organised along six principal business lines: money markets; rates flow trading; currencies and commodities; equities; credit and mortgage markets and portfolio management & origination. RBS Insurance... -

Page 56

... RBS Insurance, 80.01% of Global Merchant Services and substantially all of RBS Sempra Commodities JV business, as well as divesting the RBS branch-based business in England and Wales and the NatWest branches in Scotland, along with the Direct SME customers across the UK. Competition The Group... -

Page 57

... affect the Group's business, results of operations and financial condition and give rise to increased operational risk and may impair the Group's ability to raise new Tier 1 capital due to restrictions on its ability to make discretionary dividend or coupon payments on certain securities. The Group... -

Page 58

Business review continued Key financials Pro forma Statutory 2008 £m 2010 £m 2009 £m 2008 £m for the year ended 31 December Total income (1) Operating profit/(loss) before impairment losses and fair value of own debt (2) Loss before tax (3) Loss attributable to ordinary and B shareholders ... -

Page 59

... on redemption of own debt Strategic disposals Bonus tax Gains on pensions curtailment Asset Protection Scheme credit default swap - fair value changes Write-down of goodwill and other intangible assets Adjusted earnings/(loss) per ordinary and B share from continuing operations 14,200 8,194 (2,211... -

Page 60

Business review continued 2010 compared with 2009 - pro forma Operating profit/(loss) Group operating profit, excluding fair value of own debt, amortisation of purchased intangible assets, integration and restructuring costs, gain on redemption of own debt, strategic disposals, bonus tax, gains on... -

Page 61

... problem loans was 46% (2009 - 45%). Tax The tax charge for 2010 was £634 million compared with a tax credit of £429 million in 2009. Earnings Basic earnings per ordinary share, including discontinued operations, was a loss of 0.5p per share compared with a loss of 6.4p for 2009. RBS Group 2010... -

Page 62

Business review continued 2009 compared with 2008 - pro forma Operating loss Group operating loss, excluding fair value of own debt, amortisation of purchased intangible assets, write-down of goodwill and other intangible assets, integration and restructuring costs, gain on redemption of own debt,... -

Page 63

... loans was 45% (2008 - 51%). Tax The Group recorded a tax credit of £429 million in 2009, compared with a tax credit of £2,167 million in 2008. Earnings Basic earnings per ordinary and B share, including discontinued operations, improved from a loss of 146.7p to a loss of 6.4p. RBS Group 2010... -

Page 64

... (2009 - £350 million increase; 2008 - £860 million increase) to record interest on financial assets and liabilities designated as at fair value through profit or loss. Related interest-earning assets and interest-bearing liabilities have also been adjusted. (3) Gross yield is the interest rate... -

Page 65

Business review Average balance sheet and related interest Pro forma 2010 Average balance £m Interest £m Rate % Average balance £m Pro forma 2009 Interest £m Rate % Assets Loans and advances to banks Loans and advances to customers Debt securities Interest-earning assets Total interest-earning... -

Page 66

... - Overseas Customer accounts: other time deposits - UK - Overseas Debt securities in issue - UK - Overseas Subordinated liabilities - UK - Overseas Internal funding of trading business - UK - Overseas - UK Interest-bearing liabilities - Overseas Total interest-bearing liabilities - banking business... -

Page 67

...savings deposits - UK - Overseas Customer accounts: other time deposits - UK - Overseas Debt securities in issue - UK - Overseas Subordinated liabilities - UK - Overseas Internal funding of trading business - UK - Overseas - UK Interest-bearing liabilities - Overseas - banking business (2,3,6) Total... -

Page 68

...(2,3) Total assets Percentage of assets applicable to overseas operations Liabilities Deposits by banks Customer accounts: demand deposits Customer accounts: savings deposits Customer accounts: other time deposits Debt securities in issue Subordinated liabilities Internal funding of trading business... -

Page 69

...: savings deposits UK Overseas Customer accounts: other time deposits UK Overseas Debt securities in issue UK Overseas Subordinated liabilities UK Overseas Internal funding of trading business UK Overseas Total interest payable of the banking business UK Overseas Movement in net interest income UK... -

Page 70

...: savings deposits UK Overseas Customer accounts: other time deposits UK Overseas Debt securities in issue UK Overseas Subordinated liabilities UK Overseas Internal funding of trading business UK Overseas Total interest payable of the banking business UK Overseas Movement in net interest income UK... -

Page 71

Business review Non-interest income 2010 £m Pro forma (1) 2009 £m 2008 £m 2010 £m Statutory 2009 £m 2008 £m Fees and commissions receivable Fees and commissions payable Income/(loss) from trading activities - excluding Asset Protection Scheme credit default swap - fair value changes - Asset ... -

Page 72

... of 2009 the Group recorded a gain of £3,790 million on a liability management exercise to redeem a number of Tier 1 and upper Tier 2 securities. Other operating income decreased by £1,280 million. This reflected changes in the fair value of own debt of £926 million together with lower profits on... -

Page 73

...the £2.5 billion target for 2011 and are forecast to exceed £3 billion by 2013. Staff costs, excluding pension schemes curtailment gains, fell by £322 million to £9,671 million, driven by savings in Global Banking & Markets, UK Retail and Non-Core partially offset by higher costs in Group Centre... -

Page 74

... RBS systems. Accruals in relation to integration costs are set out below. 2009 compared with 2008 Integration costs in 2009 were £859 million compared with £1,050 million in 2008. Integration costs decreased primarily due to lower RBS N.V. (formerly ABN AMRO) integration activity during the year... -

Page 75

... relation to divestment costs are set out below. At 31 December 2009 £m Charge to income statement £m Utilised during the year £m At 31 December 2010 £m Staff costs - redundancy Staff costs - other Premises and equipment Other - - - - - 28 23 6 25 82 (6) (15) (6) (23) (50) 22 8 - 2 32 RBS... -

Page 76

Business review continued Impairment losses 2010 £m Pro forma 2009 £m 2008 £m 2010 £m Statutory 2009 £m 2008 £m New impairment losses Less: recoveries of amounts previously written-off Charge to income statement Comprising: Loans and advances Securities Charge to income statement 9,667 (... -

Page 77

... CDPCs (2) Asset-backed products Other credit exotics Equities Leveraged finance Banking book hedges Other Net credit and other market losses Notes: (1) Included in 'Income from trading activities', significantly all in Non-Core. (2) Credit derivative product companies. 2010 £m 2009 £m 2008... -

Page 78

... Risk and balance sheet management Financial statements Financial statements Financial statements Sub-section Other risk exposures Note 12 Financial instruments - valuation Critical accounting policies Note 11 Financial instruments - classification Page 204 310 284 306 Tax 2010 £m Pro forma 2009... -

Page 79

... assets (RWAs). 2010 £m 2009 £m 2008 £m UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Retail & Commercial Global Banking & Markets RBS Insurance Central items Core Non-Core Operating profit/(loss) before fair value of own debt Fair value... -

Page 80

...2.08 2010 2009 £bn 2008 £bn Risk-weighted assets by division UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Retail & Commercial Global Banking & Markets Other Core Non-Core Group before benefit of Asset Protection Scheme Benefit of Asset Protection... -

Page 81

Business review Employee numbers at 31 December (full time equivalents in continuing operations rounded to the nearest hundred) 2010 2009 2008 UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Retail & Commercial Global Banking & Markets RBS Insurance ... -

Page 82

Business review continued UK Retail 2010 £m 2009 £m 2008 £m Net interest income Net fees and commissions Other non-interest income (net of insurance claims) Non-interest income Total income Direct expenses - staff costs - other Indirect expenses Operating profit before impairment losses ... -

Page 83

...in 2010 on growing secured lending while at the same time building customer deposits, thereby reducing the Group's reliance on wholesale funding. Loans and advances to customers grew 5%, with a change in mix from unsecured to secured as the Group actively sought to improve its risk profile. Mortgage... -

Page 84

...) on a total book of £83.2 billion. Mortgage arrears rates stabilised in the second half of 2009 and remain well below the industry average, as reported by the Council of Mortgage Lenders. Repossessions show only a small increase on 2008, as the Group continues to support customers facing financial... -

Page 85

Business review UK Corporate 2010 £m 2009 £m 2008 £m Net interest income Net fees and commissions Other non-interest income Non-interest income Total income Direct expenses - staff - other Indirect expenses Operating profit before impairment losses Impairment losses Operating profit Analysis of... -

Page 86

Business review continued UK Corporate continued 2010 £bn 2009 £bn 2008 £bn Capital and balance sheet Total third party assets Loans and advances to customers (gross) - banks and financial institutions - hotels and restaurants - housebuilding and construction - manufacturing - other - private ... -

Page 87

Business review Wealth 2010 £m 2009 £m 2008 £m Net interest income Net fees and commissions Other non-interest income Non-interest income Total income Direct expenses - staff costs - other Indirect expenses Operating profit before impairment losses Impairment losses Operating profit Analysis of... -

Page 88

... constant exchange rates during 2009, with investors turning to more liquid assets and away from longer term investments. Loans and advances increased by 10% over 2008, primarily in the UK. Lending margins improved, particularly for mortgages, and credit metrics for new business remain satisfactory... -

Page 89

Business review Global Transaction Services 2010 £m 2009 £m 2008 £m Net interest income Non-interest income Total income Direct expenses - staff costs - other Indirect expenses Operating profit before impairment losses Impairment losses Operating profit Analysis of income by product Domestic ... -

Page 90

Business review continued Global Transaction Services continued 2010 compared with 2009 Operating profit increased 12%, or 10% on a constant foreign exchange basis, driven by a robust income performance (which has more than compensated for the loss of Global Merchant Services (GMS) income), good ... -

Page 91

Business review Ulster Bank 2010 £m 2009 £m 2008 £m Net interest income Net fees and commissions Other non-interest income Non-interest income Total income Direct expenses - staff - other Indirect expenses Operating profit before impairment losses Impairment losses Operating (loss)/profit ... -

Page 92

Business review continued Ulster Bank continued 2010 £bn 2009 £bn 2008 £bn Capital and balance sheet Loans and advances to customers (gross) - mortgages - corporate - property - other corporate - other lending Customer deposits Risk elements in lending - mortgages - corporate - property - ... -

Page 93

... asset values. Sectors driven by consumer spending have been affected by the double digit decline in 2009 with rising default rates evident. Customer account numbers increased by 3% during 2009, with growth fuelled by strong current account activity and new-to-bank savings customers. RBS Group 2010... -

Page 94

...$m 2008 US$m 2010 £m 2009 £m 2008 £m Net interest income Net fees and commissions Other non-interest income Non-interest income Total income Direct expenses - staff - other Indirect expenses Operating profit before impairment losses Impairment losses Operating profit/(loss) Average exchange rate... -

Page 95

Business review 2010 US$bn 2009 US$bn 2008 US$bn 2010 £bn 2009 £bn 2008 £bn Capital and balance sheet Total third party assets Loans and advances to customers (gross) - residential mortgages - home equity - corporate and commercial - other consumer Customer deposits (excluding repos) Risk ... -

Page 96

Business review continued Global Banking & Markets 2010 £m 2009 £m 2008 £m Net interest income from banking activities Net fees and commissions receivable Income from trading activities Other operating income (net of related funding costs) Non-interest income Total income Direct expenses - ... -

Page 97

Business review 2010 £bn 2009 £bn 2008 £bn Capital and balance sheet Loans and advances to customers Loans and advances to banks Reverse repos Securities Cash and eligible bills Other Total third party assets (excluding derivatives mark-to-market) Net derivative assets (after netting) ... -

Page 98

... constant exchange rates, compared with 31 December 2008, driven by a 43% reduction in loans and advances as customers took advantage of favourable capital market conditions to raise alternative forms of finance to bank debt. This reduction was partially offset by an increase in liquid assets. Risk... -

Page 99

...2009 £m 2008 £m Earned premiums Reinsurers' share Net premium income Fees and commissions Instalment income Other income Total income Net claims Underwriting profit Staff expenses Other expenses Total direct expenses Indirect expenses Technical result Impairment losses Investment income Operating... -

Page 100

Business review continued RBS Insurance continued 2010 2009 2008 Performance ratios Return on equity (3) Loss ratio (4) Commission ratio (5) Expense ratio (6) Combined operating ratio (7) Balance sheet General insurance reserves - total (£m) (7.9%) 92% 10% 13% 115% 7,559 1.7% 84% 9% 14% 106% ... -

Page 101

Business review 2009 compared with 2008 Operating profit was severely affected by the rising costs of bodily injury claims, declining to £58 million. Significant price increases were implemented in the latter part of the year to mitigate the industry trend of rising claims costs. Income grew by ... -

Page 102

Business review continued Central items 2010 £m 2009 £m 2008 £m Central items not allocated before fair value of own debt Fair value of own debt Central items not allocated Note: (1) Costs/charges are denoted by brackets. 577 35 612 385 (93) 292 150 875 1,025 Funding and operating costs ... -

Page 103

Business review Non-Core 2010 £m 2009 £m 2008 £m Net interest income Net fees and commissions Loss from trading activities Insurance net premium income Other operating income - rental income - other (1) Non-interest income Total income Direct expenses - staff - operating lease depreciation - ... -

Page 104

Business review continued Non-Core continued 2010 £m 2009 £m 2008 £m (Loss)/income from trading activities Monoline exposures Credit derivative product companies Asset-backed products (1) Other credit exotics Equities Leveraged finance Banking book hedges Other (2) (5) (139) 235 77 (17) - (82... -

Page 105

...infrastructure Property and construction Transport Telecoms, media & technology Banks and financials Other Total Global Banking & Markets Other Wealth Global Transaction Services Central items Total Other Total impairment losses 2010 £m 2009 £m 2008 £m 5 8 - 13 6 47 - 53 1 42 62 105 26 437... -

Page 106

... Transport Telecoms, media and technology Banks and financials Other Total Global Banking & Markets Other Wealth Global Transaction Services RBS Insurance Central items Total Other Gross loans and advances to customers (excluding reverse repurchase agreements) 2010 £bn 2009 £bn 2008 £bn... -

Page 107

Business review 2010 compared with 2009 By the end of 2010 third party assets (excluding derivatives) had decreased to £138 billion, £5 billion lower than the end of year target, as a result of a successful disposal strategy, managed portfolio run-off and impairments. 2010 operating losses in Non... -

Page 108

..., accrued income and other assets Assets of disposal groups Total assets Liabilities Bank deposits Repurchase agreements and stock lending Deposits by banks Customers deposits Repurchase agreements and stock lending Customer accounts Debt securities in issue Settlement balances Short positions... -

Page 109

... December 2010 were down £69.8 billion, 5%, compared with 31 December 2009. This principally reflects the continuing planned disposal of Non-Core assets, together with a reduction in the level of debt securities and mark-to-market value of derivatives in Global Banking & Markets. Cash and balances... -

Page 110

...-Core assets, together with a reduction in the level of debt securities and the mark-to-market value of derivatives. Cash and balances at central banks were up £4.8 billion, 9%, to £57.0 billion principally due to an improvement in the Group's structural liquidity position during 2010. Loans and... -

Page 111

.... Debt securities in issue were down £23.1 billion, 9% to £246.3 billion, mainly as a result of movements in exchange rates together with reductions in Global Banking & Markets and Non-Core. Retirement benefit liabilities increased by £1.2 billion, 74%, to £2.7 billion, with net actuarial losses... -

Page 112

...interest, up £20.6 billion. Debt securities in issue were down £32.7 billion, 11% to £267.6 billion mainly as a result of movements in exchange rates, together with reductions in Global Banking & Markets, Non-Core and the RFS Holdings minority interest. Retirement benefit liabilities increased by... -

Page 113

Business review Cash flow 2010 £m 2009 £m 2008 £m Net cash flows from operating activities Net cash flows from investing activities Net cash flows from financing activities Effects of exchange rate changes on cash and cash equivalents Net increase/(decrease) in cash and cash equivalents 19,291... -

Page 114

... 46,500 36,900 695,800 n/a 695,800 Banking book: On-balance sheet Off-balance sheet Trading book 480,200 84,600 44,200 609,000 % % % % 318,600 59,400 22,300 400,300 % Risk asset ratios Core Tier 1 Tier 1 Total Note: (1) The data for 2010, 2009 and 2008 are on a Basel II basis; prior periods are... -

Page 115

... AMRO as well as the transfers of businesses to the other Consortium Members occurred on 1 January 2008. Group operating profit/(loss) on a pro forma basis excludes: x x x x x x gain on redemption of own debt; strategic disposals; bonus tax; Asset Protection Scheme credit default swap - fair value... -

Page 116

... income Total income Operating expenses Profit before other operating charges Insurance net claims Operating profit before impairment losses Impairment losses Operating loss before fair value of own debt Fair value of own debt Operating loss Amortisation of purchased intangible assets Integration... -

Page 117

...-interest income Total income Operating expenses Profit/(loss) before other operating charges Insurance net claims Operating loss before impairment losses Impairment losses Operating loss before fair value of own debt Fair value of own debt Operating loss Amortisation of purchased intangible assets... -

Page 118

..., accrued income and other assets Assets of disposal groups Total assets Liabilities Bank deposits Repurchase agreements and stock lending Deposits by banks Customer deposits Repurchase agreements and stock lending Customer accounts Debt securities in issue Settlement balances Short positions... -

Page 119

..., accrued income and other assets Assets of disposal groups Total assets Liabilities Bank deposits Repurchase agreements and stock lending Deposits by banks Customer deposits Repurchase agreements and stock lending Customer accounts Debt securities in issue Settlement balances Short positions... -

Page 120

..., accrued income and other assets Assets of disposal groups Total assets Liabilities Bank deposits Repurchase agreements and stock lending Deposits by banks Customer deposits Repurchase agreements and stock lending Customer accounts Debt securities in issue Settlement balances Short positions... -

Page 121

... strategy â- Group policy framework â- Capital/risk adjusted performance Risk architecture â- Risk, finance and treasury architecture â- Risk data quality â- Analytics and modelling â- Risk information and reporting Operating Model Deliver 5 year plan with strong risk and balance sheet... -

Page 122

Business review continued Introduction* continued Governance Risk and balance sheet management strategies are owned and set by the Group's Board of directors, and implemented by executive management led by the Group Chief Executive. There are a number of committees and executives that support the ... -

Page 123

... level by a risk governance structure embedded in the businesses. During 2010, Risk Management has been enhanced by the appointment of a Deputy Chief Risk Officer to whom the Divisional CROs and the functional risk heads now report. Committee Group Board Executive Committee (ExCo) Board Risk... -

Page 124

... of Balance Sheet Management, Group Treasury Global Head of Markets Head of Non-Core division Head of Restructuring and Risk Deputy Chief Risk Officer Group Chief Credit Officer Global Head of: Market and Insurance Risk; Operational Risk; Country Risk and Firm Wide Risk Director, Group Finance Chief... -

Page 125

... of term debt issuance. Asset quality has broadly stabilised, resulting in total loan impairments 33% lower than in 2009. However, weakness in the Irish economy and falling property values have resulted in the doubling of Ulster Bank Group impairments (Core and Non-Core) in 2010. Markets have... -

Page 126

... defined benefit pension schemes. Volatile funding position caused by the uncertainty of future investment returns and the projected value of schemes' liabilities. In 2010, the Group established the Group Corporate Sustainability Committee, and also developed a framework for managing environmental... -

Page 127

... actually happen in any of the modelled scenarios. Furthermore, the results are FSA calculations impacting revenues, impairments and balance sheet items and assume an unchanged balance sheet from the end of 2009. The test confirms RBS remains well capitalised with a strong Tier 1 capital ratio under... -

Page 128

... Risk Management, in respect of risk-weighted assets (RWAs), manage and control the Group's balance sheet risks and consequent impact on the Group's capital, funding, liquidity, interest rate and currency risks. The FSA uses risk asset ratio (RAR) as a measure of capital adequacy in the UK banking... -

Page 129

... first loss Total Tier 2 capital Tier 3 Supervisory deductions Unconsolidated investments - RBS Insurance - other investments Other deductions Deductions from total capital Total regulatory capital Note: (1) Includes reduction for own liabilities carried at fair value 2010 £m 2009 £m 2008 £m 70... -

Page 130

... holdings Less APS first loss Total Tier 2 capital Tier 3 Supervisory deductions Unconsolidated investments - RBS Insurance - other investments Other deductions Deductions from total capital Total regulatory capital Note: (1) Includes reduction for own liabilities carried at fair value 70,388 1,719... -

Page 131

... are set out below: Credit risk £bn Counterparty risk £bn Market risk £bn Operational risk £bn Total £bn APS £bn Total £bn 2010 UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Retail & Commercial Global Banking & Markets Other Core Non-Core Group... -

Page 132

Business review continued Balance sheet management: Capital* continued Asset Protection Scheme The Group acceded to the Asset Protection Scheme ('APS' or 'the Scheme') in December 2009. Following the accession to the APS, HM Treasury provides loss protection against potential losses arising in a ... -

Page 133

... the taxpayer. Implementation by the Group RBS is advanced in its planning to implement these new measures and is appropriately well-capitalised with tangible equity of £56 billion, Core Tier 1 capital of £49 billion and a Core Tier 1 ratio of 10.7% at 31 December 2010. RBS Group 2010 131 -

Page 134

... and shared intent to work together to help the UK economy recover and grow. The banks: x x x x expected loss net of provisions; deferred tax assets not relating to timing differences; unrealised losses on available-for-sale securities; and significant investments in non-consolidated financial... -

Page 135

Business review Risk and balance sheet management Structure of prudential regulation in the UK Following the consultation by HM Treasury on 'A new approach to financial regulation' in 2010, the government subsequently published further detailed proposals to give the Bank of England responsibility ... -

Page 136

...for each business and applied to the major operating subsidiary balance sheets. A variety of firm-specific and market related scenarios are used at the consolidated level and in individual countries. These scenarios include assumptions about significant changes in key funding sources, credit ratings... -

Page 137

Business review Risk and balance sheet management Funding sources The table below shows the composition of the Group's primary funding sources, excluding repurchase agreements. 2010 £m 2009 £m 2008 £m % % % Deposits by banks - cash collateral - other Debt securities in issue - commercial ... -

Page 138

Business review continued Balance sheet management: Funding and liquidity risk continued The tables below show the Group's debt securities in issue and subordinated liabilities by maturity. Debt securities in issue £m Subordinated liabilities £m 2010 Total £m % Less than one year 1-5 years ... -

Page 139

Business review Risk and balance sheet management Long-term debt issuances The table below shows debt securities issued by the Group with an original maturity of one year or more. The Group also executes other long-term funding arrangements (predominately term repurchase agreements) not reflected ... -

Page 140

...liquidity portfolio at the end of 2009 reflects the build up of liquid assets ahead of the legal separation of RBS N.V. and ABN AMRO in April 2010. Following the separation, the liquid assets and associated short-term wholesale funding were managed down to business as usual levels. x The Group has... -

Page 141

... the Basel III guidance issued in December 2010. This measure seeks to show the proportion of structural term assets which are funded by stable funding including customer deposits, long-term wholesale funding, and equity. 2010 £bn ASF(1) £bn 2009 £bn ASF(1) £bn 2008 £bn ASF(1) £bn Weighting... -

Page 142

Business review continued Balance sheet management: Funding and liquidity risk continued Funding and liquidity metrics continued The table below shows the Group's loan to deposit ratio and customer funding gap. Loan to deposit ratio (1) Group Core % % Customer funding gap (1) Group £bn 2010 2009... -

Page 143

Business review Risk and balance sheet management 2009 0-3 months £m 3-12 months £m 1-3 years £m 3-5 years £m 5-10 years £m 10-20 years £m Assets by contractual maturity Cash and balances at central banks Loans and advances to banks Debt securities Settlement balances Other financial ... -

Page 144

Business review continued Balance sheet management: Funding and liquidity risk continued Assets and liabilities by contractual cashflow maturity continued 2008 0-3 months £m 3-12 months £m 1-3 years £m 3-5 years £m 5-10 years £m 10-20 years £m Assets by contractual maturity Cash and ... -

Page 145

... and balance sheet management Interest rate risk The banking book consists of interest bearing assets, liabilities and derivative instruments used to mitigate risks which are accounted for on an accrual basis, as well as non-interest bearing balance sheet items which are not subjected to fair value... -

Page 146

... to rising rates related to capital raised in December 2009. x Actions taken during the year increased the current base level of net interest income, while reducing the Group's overall asset sensitivity. The Group seeks to limit the sensitivity to its Core Tier 1 ratio to 20 basis points in a 10... -

Page 147

Business review Risk and balance sheet management Equity risk The Group holds equity positions in order to achieve strategic objectives, support venture capital transactions or in respect of customer restructuring arrangements. The Group is exposed to market risk on these banking book equity ... -

Page 148

...of Group-wide and divisional policies setting out the risk parameters within which business units may operate. Information on the Group's credit portfolios is reported to the Board via the divisional and Group level risk committees detailed in the Governance section on page 120. Product/asset class... -

Page 149

..., operational and franchise risk related losses. The framework for the Group's appetite for country risk is set by the Executive Risk Forum (ERF) in the form of limits by country risk grade, with sub-limits on medium-term exposure. Authority is delegated to the Group Country Risk Committee to manage... -

Page 150

... £2.4 billion related to commercial real estate and £2.1 billion to manufacturing. The incidence of the main types of arrangements is analysed below: % of loans (by value) Term extensions Debt forgiveness Debt for equity Interest rate concessions and payment moratoriums The total above... -

Page 151

Business review Risk and balance sheet management Credit risk mitigation* The Group employs a number of structures and techniques to mitigate credit risk. Netting of debtor and creditor balances will be undertaken in accordance with relevant regulatory and internal policies; exposure on over-the-... -

Page 152

... for internal management reporting across portfolios, including a Group level asset quality scale, as shown below. Internal reporting and oversight of risk assets is principally differentiated by credit grades. Customers are assigned credit grades, based on 2010 Non-Core £m x Non-Core exposure... -

Page 153

Business review Risk and balance sheet management AQ10 credit risk assets UK Retail UK Corporate Wealth Global Transaction Services Ulster Bank US Retail & Commercial Retail & Commercial Global Banking & Markets Core Non-Core 2010 AQ10 % of divisional £m credit risk assets 2009 AQ10 % of ... -

Page 154

... and for those which, under the country watch list process, have been identified as exhibiting signs of actual or potential stress. The country risk tables below show credit risk assets exceeding £1 billion by borrowers domiciled in countries with an external rating of A+ and below from Standard... -

Page 155

... of collateralised trading activity. Portugal: lending decreased slightly by £0.1 billion related to reductions in corporate activity. Non-Core represents 41% of the total exposure; the structure of the exposure was enhanced through a shift to short-term and collateralised products to support the... -

Page 156

... loan portfolio. Particular attention is given to industry sectors where the Group believes there is a high degree of risk or potential for volatility in the future. The table below analyses credit risk assets by industry sector and geography. Industry sector 2010 (1) UK £m Western Europe (excl. UK... -

Page 157

...Core bank exposure resides primarily in Corporate Banking and Global Banking & Markets and the portfolio is well diversified geographically. In aggregate, the exposure within and asset quality of the Core portfolio remained stable over the year. Global economic conditions and related trends in trade... -

Page 158

...division (1) Core UK Corporate Ulster Bank US Retail & Commercial Global Banking & Markets The commercial real estate lending portfolio totalled £87 billion at 31 December 2010, a 11% decrease over the prior year (2009 - £98 billion). The Non-Core portion of the portfolio totalled £46 billion (52... -

Page 159

... senior management approval. Current market conditions have resulted in some borrowers experiencing difficulty in finalising long-term finance arrangements. These borrowers are managed within the problem debt management process in "watch" or the GRG. Tighter risk appetite criteria for new business... -

Page 160

... US. The analysis below includes both Core and Non-Core balances. Personal credit risk assets (1) UK Retail - mortgages - cards, loans and overdrafts Ulster Bank - mortgages - other personal Citizens - mortgages - auto and cards - other (2) Other (3) 2010 £m 2009 £m 2008 £m 92,592 18,072 21,162... -

Page 161

Business review Risk and balance sheet management Retail credit assets: UK residential mortgages Key points x The UK mortgage portfolio totalled £92.6 billion at 31 December 2010, an increase of 8% from 31 December 2009, due to continued strong sales growth and lower redemption rates in historical... -

Page 162

... in the year. (3) The 2009 data have been revised to exclude the Kroger Personal Finance portfolio, which was sold in 2010. Key points x The UK personal lending portfolio, of which 98% is in Core businesses, comprises credit cards, unsecured loans and overdrafts and totalled £18.1 billion at 31... -

Page 163

Business review Risk and balance sheet management Ulster Bank Group (Core and Non-Core)* Ulster Bank Group accounts for 8% of the Group's total credit risk assets or 7% of the Group's Core credit risk assets. The Irish economy has experienced severe economic headwinds resulting in a substantial ... -

Page 164

Business review continued Risk management: Credit risk continued Ulster Bank Group (Core and Non-Core)* continued Risk elements in lending and impairments by sector Gross loans (1) £m REIL £m Provisions £m REIL as a % of gross loans % Provisions as a % of REIL % Provisions as a % of gross loans... -

Page 165

Business review Risk and balance sheet management 2009 Gross loans (1) £m REIL £m Provisions £m REIL as a % of gross loans % Provisions as a % of REIL % Provisions as a % of gross loans % Impairment charge £m Amounts written-off £m Ulster Bank Group Mortgages Personal unsecured ... -

Page 166

... during the year Note: (1) LTV averages calculated by transaction volume. 2010 % 2009 % 2008 % 35.9 13.5 13.5 37.1 71.2 75.9 40.7 15.2 15.5 28.6 62.5 72.8 47.1 17.1 18.2 17.6 54.3 71.1 Key points x The residential mortgage portfolio across Ulster Bank Group totalled £21.2 billion at 31... -

Page 167

Business review Risk and balance sheet management Commercial real estate The Commercial real estate lending portfolio for Ulster Bank Group totalled £18 billion at 31 December 2010 and decreased by 2% during the year. The Non-Core portion of the portfolio totalled £12.6 billion (70% of the ... -

Page 168

... credit quality gradings. Credit risk assets analysed on the preceding pages are reported internally to senior management, however they exclude certain exposures, primarily debt securities, and take account of legal agreements, including master netting arrangements that provide a right of legal set... -

Page 169

Business review Risk and balance sheet management Loans and advances 2009 Core £m Non-Core £m Total £m Securities £m Derivatives £m Other (1) £m Total £m Netting and offset (2) £m Total Central and local government Finance - banks - other (3) Residential mortgages Personal lending ... -

Page 170

Business review continued Risk management: Credit risk continued Balance sheet analysis: Industry and geography analysis continued Loans and advances to banks and customers by geography The table below analyses loans and advances gross of provisions by geography (location of office). 2010 £m 2009... -

Page 171

Business review Risk and balance sheet management The tables below and on pages 169 to 173 analyse financial assets by geography (location of office) and industry. Loans and advances 2010 Core £m Non-Core £m Total £m Securities £m Derivatives £m Other (1) £m Total £m Netting and offset (2) ... -

Page 172

Business review continued Risk management: Credit risk continued Balance sheet analysis: Industry and geography analysis continued Loans and advances 2010 Core £m Non-Core £m Total £m Securities £m Derivatives £m Other (1) £m Total £m Netting and offset (2) £m RoW Central and local ... -

Page 173

Business review Risk and balance sheet management Loans and advances 2009 Core £m Non-Core £m Total £m Securities £m Derivatives £m Other (1) £m Total £m Netting and offset (2) £m Europe Central and local government Finance - banks - other (3) Residential mortgages Personal lending ... -

Page 174

Business review continued Risk management: Credit risk continued Balance sheet analysis: Industry and geography analysis continued Netting and offset (2) £m 2008 Loans and advances £m Securities £m Derivatives £m Other (1) £m Total £m UK Central and local government Finance - banks - ... -

Page 175

Business review Risk and balance sheet management 2008 Loans and advances £m Securities £m Derivatives £m Other (1) £m Total £m Netting and offset (2) £m Europe Central and local government Finance - banks - other (3) Residential mortgages Personal lending Property Construction ... -

Page 176

... the customer type. All credit grades across the Group map to both a Group level asset quality scale, used for external financial reporting, and a master grading scale for wholesale exposures used for internal management reporting across portfolios. Debt securities are analysed by external ratings... -

Page 177

Business review Risk and balance sheet management 2010 Cash and balances at central banks £m Loans and advances to banks (1) £m Loans and advances to customers £m Settlement balances £m Derivatives £m Other financial instruments £m Commitments £m Contingent liabilities £m Total £m... -

Page 178

Business review continued Risk management: Credit risk continued Balance sheet analysis: Asset quality continued Cash and balances at central banks £m Loans and advances to banks (1) £m Loans and advances to customers £m Other financial instruments £m 2008 Settlement balances £m ... -

Page 179

... review Risk and balance sheet management Central and local government 2009 UK £m US £m Other £m Banks and building societies £m ABS (1) £m Corporate £m Other £m Total £m % of total (2) AAA AA to AA+ A to AABBB- to ANon-investment grade Unrated Group before RFS MI RFS MI Group 2008... -

Page 180

... and local government 2010 UK £m US £m Other £m Banks and building societies £m ABS £m Corporate £m Other £m Total £m Held-for-trading (HFT) Designated as at fair value through profit or loss Available-for-sale Loans and receivables Total Short positions (HFT) Net 2009 5,097 1 8,377... -

Page 181

... netting agreements in respect of mark-to-market (mtm) values and collateral do not result in a net presentation in the Group's balance sheet under IFRS. 2010 6-12 months £m 0-3 months £m 3-6 months £m 1-5 years £m Over 5 years £m Total £m 2009 Total £m AQ1 AQ2 AQ3 AQ4 AQ5 AQ6 AQ7... -

Page 182

... greater than 0.5% of the Group's total assets. None of these countries have experienced repayment difficulties that have required restructuring of outstanding debt. Government £m 2010 Banks £m Other £m Total £m 2009 Total £m 2008 Total £m United States France Germany Japan Spain... -

Page 183

Business review Risk and balance sheet management REIL, provisions and reserves All the disclosures in this section (pages 181 to 192) are audited. The Group classifies impaired assets as either risk elements in lending (REIL) or potential problem loans (PPL). REIL represents impaired loans, and ... -

Page 184

... Irish property prices. x x Past due analysis The table below shows loans and advances to customers that were past due at the balance sheet date but not considered impaired: 2009 Group before RFS MI £m 2010 Core £m Non-Core £m Total £m Core £m Non-Core £m RFS MI £m Group £m 2008 Group... -

Page 185

Business review Risk and balance sheet management Loans, REIL and impairments by industry and geography The tables below analyse gross loans and advances to customers and banks (excluding reverse repos and disposal groups), REIL, provisions, impairment charge and amounts written-off relating to ... -

Page 186

...loans % Impairment charge £m Amounts written-off £m 2009 REIL £m Provisions £m Central and local government Finance - banks - other Residential mortgages Personal lending Property Construction Manufacturing Service industries and business activities... 471 6,478 461 6,939 184 RBS Group 2010 -

Page 187

Business review Risk and balance sheet management 2010 Gross loans £m REIL £m Provisions £m Core REIL as a % of gross loans % Provisions as a % of REIL % Provisions as a % of gross loans % Impairment charge £m Amounts written-off £m Central and local government Finance - banks - other... -

Page 188

...government Finance - banks - other Residential mortgages Personal lending Property Construction Manufacturing Service industries and business activities Agriculture, forestry and fishing Finance leases and instalment credit Interest accruals Latent of which: UK Europe US RoW Group before RFS MI 2009... -

Page 189

Business review Risk and balance sheet management Risk elements in lending and potential problem loans by division The tables below analyse the Group's loans and advances to banks and customers (excluding reverse repos and disposal groups) and related REIL, PPL, provisions, impairments, amounts ... -

Page 190

.... Available-for-sale financial assets are initially recognised at fair value plus directly related transaction costs and are subsequently measured at fair value with changes in fair value reported in owners' equity until disposal, at which stage the cumulative gain or loss is recognised in profit or... -

Page 191

Business review Risk and balance sheet management Movement in loan impairment provisions The movement in provisions balance by division is shown in the table below. UK Retail £m UK Corporate £m Wealth £m GTS (1) £m Ulster Bank £m US R&C (2) £m Total R&C (2) £m GBM (3) £m Total Core £m Non-... -

Page 192

... following table analyses impairment losses. 2010 £m 2009 £m 2008 £m Latent loss Collectively assessed Individually assessed Loans to customers Loans to banks Securities Charge to income statement Charge relating to customer loans as a % of gross customer loans (1) Note: (1) Gross of provisions... -

Page 193

Business review Risk and balance sheet management Available-for-sale debt securities and related reserves The table below analyses available-for-sale (AFS) debt securities by issuer and related AFS reserves, for countries exceeding £0.5 billion at any reporting date below, together with the total ... -

Page 194

... available-for-sale debt securities that were in an unrealised loss position at 31 December, and the related gross unrealised losses. Less than 12 months Gross unrealised Fair value losses £m £m More than 12 months Gross unrealised Fair value losses £m £m Total Gross unrealised losses £m 2010... -

Page 195

... desk level market risk limits. A daily report summarises the Group's market risk exposures against agreed limits. This daily report is sent to the Head of Restructuring & Risk, Global Head of Market & Insurance Risk, business Chief Risk Officers and appropriate business Risk Managers. The head of... -

Page 196

... assets, money market business and the management of internal funds flow within the Group's businesses. Traded portfolios The primary focus of the Group's trading activities is to provide an extensive range of debt and equity financing, risk management and investment services to its customers... -

Page 197

... the VaR for the Group's trading portfolios segregated by type of market risk exposure. Trading VaR Interest rate Credit spread Currency Equity Commodity Diversification Average £m 2010 Period end £m Maximum £m Minimum £m Average £m 2009 Period end £m Maximum £m Minimum £m 51.6 166... -

Page 198

Business review continued Risk management: Market risk continued Traded portfolios continued Key points x The Group's period end VaR reduced as the exceptional volatility of the market data from the period of the financial crisis dropped out of the 500 days of time series data used in the VaR ... -

Page 199

... Core Non-Core 30.5 1.3 Key points x The non-traded credit spread, Core and total VaR have decreased significantly due to the implementation of the relative price-based mapping scheme in the VaR methodology discussed above and the sales of available-for-sale securities in the US mortgage business... -

Page 200

Business review continued Risk management: Market risk continued Structured Credit Portfolios Drawn notional 2010 CDOs £m CLOs £m MBS (1) £m Other ABS £m Total £m CDOs £m CLOs £m Fair value MBS (1) £m Other ABS £m Total £m 1-2 years 2-3 years 3-4 years 4-5 years 5-10 years >10 years - ... -

Page 201

... the Group's business as it is inherent in the processes it operates in to provide services to customers and generate profit for shareholders. An objective of operational risk management is not to remove operational risk altogether, but to manage the risk to an acceptable level, taking into account... -

Page 202

...report regularly on the internal control framework for which they are responsible, confirming its adequacy and effectiveness. This includes certifying compliance with the requirements of Group policies. x x x Each business unit must manage its operational risk exposure within an acceptable level... -

Page 203

Business review Risk and balance sheet management Operational risk metrics Reporting forms an integral part of operational risk management. The Group's risk management processes are designed to ensure that issues are identified, escalated and managed on a timely basis. Exposures for each division ... -

Page 204

... process, and planning for the introduction of new or changed rules and regulations. During the last 12 months the Group has experienced unprecedented levels of prospective rules and regulations particularly in the area of prudential regulation (capital, liquidity, governance and risk management... -

Page 205

...' liabilities. Pension scheme liabilities vary with changes to long-term interest rates, inflation, pensionable salaries and the longevity of scheme members as well as changes in legislation. The Group is exposed to the risk that the market value of the schemes' assets, together with future returns... -

Page 206

...-Core businesses. Definitions of acronyms used in this section can be found in the Glossary on pages 434 to 439. Asset-backed securities The Group structures, originates, distributes and trades debt in the form of loan, bond and derivative instruments in all major currencies and debt capital markets... -

Page 207

Business review Risk and balance sheet management Asset-backed securities by product, geography and measurement classification FVTPL (1) US £m UK £m Other Europe £m RoW (2) £m Total £m HFT (3) £m DFV (4) £m AFS (5) £m LAR (6) £m 2010 Gross exposure RMBS: G10 government RMBS: covered bond... -

Page 208

Business review continued Risk management: Other risk exposures continued Asset-backed securities by product, geography and measurement classification continued FVTPL (1) US £m UK £m Other Europe £m RoW (2) £m Total £m HFT (3) £m DFV (4) £m AFS (5) £m LAR (6) £m 2009 Gross exposure RMBS... -

Page 209

... RMBS: G10 government RMBS: covered bond RMBS: prime RMBS: non-conforming RMBS: sub-prime CMBS CDOs CLOs Other ABS Notes: (1) Fair value through profit or loss. (2) Rest of the world. (3) Held-for-trading. (4) Designated as at fair value. (5) Available-for-sale. (6) Loans and receivables. 33... -

Page 210

... Key points x Carrying values of asset-backed securities decreased by £16.8 billion during 2010 with net reductions across all portfolios. x x Within G10 government RMBS, net sell-downs by the US Mortgage Trading business in GBM in the first quarter of 2010, as part of the Group's repositioning... -

Page 211

... 2,174 Key point x Non-investment grade securities increased by £1.4 billion of which £1.0 billion was in CDOs reflecting purchases by GBM's Mortgage Trading business as well as credit down grades and rating withdrawals of certain ABS structures in Non-Core during the year. RBS Group 2010 209 -

Page 212

...and the credit enhancement of the securitisation structure. Several tranches of notes are issued, each secured against the same portfolio of mortgages, but providing differing levels of seniority to match the risk appetite of investors. The most junior (or equity) notes will suffer early capital and... -

Page 213

... Net (debit)/credit relating to reclassified debt securities Net credit/(debit) to income statement (1) Note: (1) Comprises the following elements for the year ended 2010 and 2009: - a loss of £5 million (2009 - £2,387 million) in income from trading activities; - impairment reversals/(losses) of... -

Page 214

Business review continued Risk management: Other risk exposures continued Monoline insurers continued A number of debt instruments with monoline protection were reclassified from HFT to AFS in 2008. Changes in the fair value since the reclassification are recognised in the income statement to the ... -

Page 215

... wrapped securities and other assets with credit enhancement from monoline insurers. These securities are traded with the benefit of this credit enhancement. Any deterioration in the credit rating of the monoline is reflected in the fair value of these assets. 2010 £m 2009 £m 2008 £m Gross... -

Page 216

Business review continued Risk management: Other risk exposures continued Credit derivative product companies continued The table below details CDPC exposures by rating. Notional: protected assets £m Fair value: reference protected assets £m Gross exposure £m Credit valuation adjustment £m Net... -

Page 217

...of its participation in the Asset Protection Scheme, due to the unique features of this derivative. The net income statement effect arising from the change in level of CVA for all other counterparties and related trades is shown in the table below. 2010 £m 2009 £m Credit valuation adjustment at... -

Page 218

... finance exposures during the year. Drawn £m 2010 Undrawn £m Total £m Drawn £m 2009 Undrawn £m Total £m Balance at 1 January Transfers (out)/in (from credit trading business) Sales and restructurings Repayments and facility reductions Funded deals Lapsed/collapsed deals Changes in fair value... -

Page 219

... set out below. 2010 £m 2009 £m 2008 £m UK Corporate - debt financing (1) - senior debt transactions (2) Total UK Corporate Ulster Bank 3,664 2,604 6,268 597 6,865 4,041 3,034 7,075 621 7,696 4,496 2,330 6,826 694 7,520 Notes: (1) Loans for UK mid-market buyouts, supplementing equity capital... -

Page 220

... own-asset conduit in 2009 with a committed liquidity of £26.0 billion (2009 - £25.1 billion) to access the Bank of England's open market operations for contingent funding purposes. x x x The average maturity of ABCP issued by the Group's conduits has risen throughout 2010, to 69.4 days (2009... -

Page 221

Business review Risk and balance sheet management Collateral analysis, profile, credit ratings and weighted average lives relating to the Group's consolidated conduits are detailed below. Funded assets 2010 Loans £m Securities £m Total £m Undrawn £m Liquidity for third parties £m Total ... -

Page 222

Business review continued Risk management: Other risk exposures continued Conduits continued CP funded assets Geographic distribution Other Europe US £m £m Credit ratings (S&P equivalent) RoW £m Total £m Weighted average life - years AAA £m AA £m A £m BBB £m Below BBB £m 2010 UK £m ... -

Page 223

Business review Risk and balance sheet management Asset Protection Scheme* All the disclosures in this section (pages 221 to 224) are unaudited and are marked with an asterisk (*). References to 'Group' in this section relate to 'Group before RFS MI'. Key aspects of the Scheme On 22 December 2009, ... -

Page 224

... finance portfolios (2010 - £6.7 billion). Credit impairments and write downs The table below analyses the cumulative credit impairment losses and adjustments to par value (including AFS reserves) relating to the covered assets. 2010 £m 2009 £m 2008 £m Loans and advances Debt securities... -

Page 225