RBS 2010 Annual Report Download - page 323

Download and view the complete annual report

Please find page 323 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

The model primarily uses the following inputs in relation to each individual

asset: notional, maturity, probability of default and expected recovery rate

given default. Other key inputs include: the correlation between the

underlying assets; the range of possible recovery rates on the underlying

assets (“alpha”); the size of the first loss; and the level of expected losses

on covered assets that have been sold, that can be treated as losses for

the purpose of the APS (“loss credits”).

During 2010, refinements were made to the treatment of derivative trades

in the valuation model. This followed a change in the nature of protection

provided in relation to certain structured credit trades involving mainly

asset backed securities and associated bought protection credit

derivatives: the risk of losses arising on the derivative trades due to

counterparty risk was replaced by the risk of incurring losses on the

underlying asset backed securities that are not recovered through the

derivative trades. The valuation refinements were made to accurately

reflect the impact of this change and ensure a consistent treatment

across all derivative trades.

The APS protects a wide range of asset types, and hence, the correlation

between the underlying assets cannot be observed from market data. In

the absence of this, the Group determines a reasonable level for this

input. The expected recovery rate given default is based on internally

assessed levels. The probability of default is calculated with reference to

data observable in the market. Where possible, data is obtained for each

asset within the APS, but for most of the assets, such observable data

does not exist. In these cases, this important input is determined from

information available for similar entities by geography and rating. The

approach for doing this was refined during the year in order to accurately

reflect both changes in market conditions and the profile of the portfolio of

covered assets.

As the inputs into the valuation model are not all observable the APS

derivative is a level 3 asset. The fair value of the credit protection at 31

December 2010 was £0.55 billion (2009 - £1.40 billion).

The Group has used the following reasonably possible alternative

assumptions in relation to those inputs that could have a significant effect

on the valuation of the APS:

Correlation: +/- 10%

The correlation uncertainty relates to both the nature of the underlying

portfolio and the seniority of protection. The +/-10% correlation range

looks reasonable in light of market observable correlations of similar

levels of protection seniority, for portfolios of investment grade and high

yield assets.

Range of possible recovery rates on underlying assets (alpha): +/- 10%

The level of alpha used in the valuation of the APS is in line with that

used to value tranches traded by the exotic credit desk and assumes that

the underlying assets have a wide range of potential recovery rates. As

the APS protects a wider range of asset classes than is generally

referenced by exotic credit trades, there is uncertainty in relation to this

approach. A comparison of actual recoveries to expected recoveries

supports the approach adopted and, in light of this, only changes of +/-

10% in the assumed width of this range are considered reasonable.

Credit spreads: +/- 10%

The credit spread uncertainty relates to determining the probability of

default for assets where there is no such observable data in the market.

An analysis of the impact on credit spreads of small changes in the

ratings assumptions in key geographic regions indicated that overall

credit spread movements in the +/- 10% range look reasonable.

Discount curve: +/- 1%

Due to the long-dated contractual maturity of the APS, and the

requirement to pay fixed levels of premiums each year, the valuation is

sensitive to long-term interest rates. Valuation uncertainty arises due to

the illiquidity of such interest rates. An interest rate range of +/- 1% is

considered reasonable.

Loss credits: +/- 10%

The level of expected losses on covered assets that have been sold that

can be treated as losses for the purpose of the APS are assessed by the

Asset Protection Agency. For disposals made by the Group where this

assessment has not been completed, the Group makes an estimate of

the likely assessment for the purpose of valuing of the APS. A range of

+/- 10% in the level of assessment is considered reasonable.

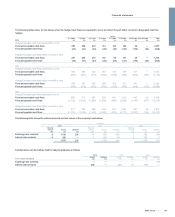

Using the above reasonably possible alternative assumptions, the fair

value of the APS derivative could be higher by approximately £860 million

or lower by approximately £940 million as detailed in the table below.

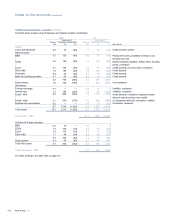

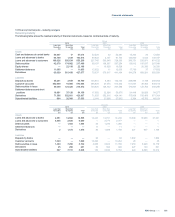

Sensitivity Favourable

£m

Unfavourable

£m

Correlation +/- 10% 300 300

Recover alpha +/- 10% 250 300

Spreads +/-10% 125 100

Discount curve +/- 1% 175 230

Loss credit +/- 10% 10 10

Total 860 940

Individual sensitivities above have been aggregated and do not reflect the

correlated effect of some of the assumptions as related sensitivities.

321RBS Group 2010

Financial statements