RBS 2010 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

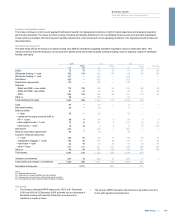

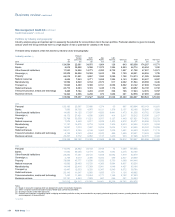

Credit risk mitigation*

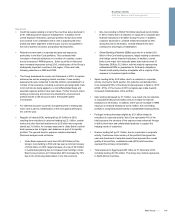

The Group employs a number of structures and techniques to mitigate

credit risk. Netting of debtor and creditor balances will be undertaken in

accordance with relevant regulatory and internal policies; exposure on

over-the-counter derivative and secured financing transactions is further

mitigated by the exchange of financial collateral and documented on

market standard terms. Further mitigation may be undertaken in a range

of transactions, from retail mortgage lending to large wholesale financing,

by structuring a security interest in a physical or financial asset; credit

derivatives, including credit default swaps, credit linked debt instruments,

and securitisation structures; and guarantees and similar instruments (for

example, credit insurance) from related and third parties are used in the

management of credit portfolios, typically to mitigate credit concentrations

in relation to an individual obligor, a borrower group or a collection of

related borrowers.

The use and approach to credit risk mitigation varies by product type,

customer and business strategy. Minimum standards applied across the

Group cover: general requirements, including acceptable credit risk

mitigation types and any conditions or restrictions applicable to those

mitigants; the means by which legal certainty is to be established,

including required documentation and all necessary steps required to

establish legal rights; acceptable methodologies for the initial and any

subsequent valuations of collateral and the frequency with which they are

to be revalued (for example, daily in the trading book); actions to be taken

in the event the current value of mitigation falls below required levels;

management of the risk of correlation between changes in the credit risk

of the customer and the value of credit risk mitigation; management of

concentration risks, for example, setting thresholds and controls on the

acceptability of credit risk mitigants and on lines of business that are

characterised by a specific collateral type or structure; and collateral

management to ensure that credit risk mitigation remains legally effective

and enforceable.

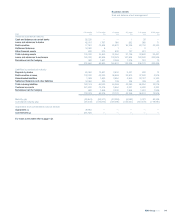

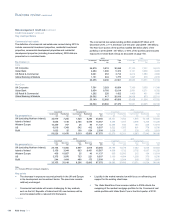

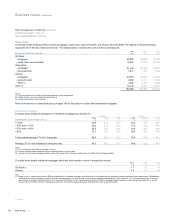

Credit risk measurement

Credit risk models are used throughout the Group to support the

quantitative risk assessment element of the credit approval process,

ongoing credit risk management, monitoring and reporting and portfolio

analytics. Credit risk models used by the Group may be divided into three

categories, as follows.

Probability of default/customer credit grade (PD)

These models assess the probability that a customer will fail to make full

and timely repayment of their obligations. The probability of a customer

failing to do so is measured over a one year period through the economic

cycle, although certain retail scorecards use longer periods for business

management purposes.

Wholesale businesses: as part of the credit assessment process, each

counterparty is assigned an internal credit grade derived from a default

probability. There are a number of different credit grading models in use

across the Group, each of which considers risk characteristics particular

to that type of customer. The credit grading models score a combination

of quantitative inputs (for example, recent financial performance) and

qualitative inputs, (for example, management performance or sector

outlook).

Retail businesses: each customer account is separately scored using

models based on the most material drivers of default. In general,

scorecards are statistically derived using customer data. Customers are

assigned a score, which in turn is mapped to a probability of default. The

probabilities of default are used to group customers into risk pools. Pools

are then assigned a weighted average probability of default using

regulatory default definitions.

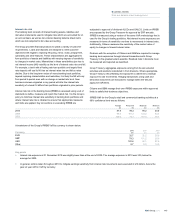

Exposure at default

Facility usage models estimate the expected level of utilisation of a credit

facility at the time of a borrower’s default. For revolving and variable draw

down type products which are not fully drawn, the exposure at default

(EAD) will typically be higher than the current utilisation. The

methodologies used in EAD modelling provide an estimate of potential

exposure and recognise that customers may make more use of their

existing credit facilities as they approach default.

Counterparty credit risk exposure measurement models are used for

derivative and other traded instruments where the amount of credit risk

exposure may be dependent upon one or more underlying market

variables such as interest or foreign exchange rates. These models drive

internal credit risk activities such as limit and excess management.

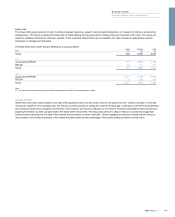

Loss given default

These models estimate the economic loss that may be experienced (the

amount that cannot be recovered) by the Group on a credit facility in the

event of default. The Group’s loss given default (LGD) models take into

account both borrower and facility characteristics for unsecured or

partially unsecured facilities, as well as the quality of any risk mitigation

that may be in place for secured facilities, plus the cost of collections and

atime discount factor for the delay in cash recovery.

149RBS Group 2010

Business review

Risk and balance sheet management