RBS 2010 Annual Report Download - page 219

Download and view the complete annual report

Please find page 219 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

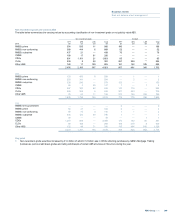

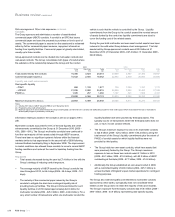

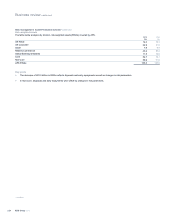

In addition to the above, UK Corporate and Ulster Bank have leveraged finance exposures as set out below.

2010 2009 2008

£m £m £m

UK Corporate

- debt financing (1) 3,664 4,041 4,496

- senior debt transactions (2) 2,604 3,034 2,330

Total UK Corporate 6,268 7,075 6,826

Ulster Bank 597 621 694

6,865 7,696 7,520

Notes:

(1) Loans for UK mid-market buyouts, supplementing equity capital provided by third party private equity investors.

(2) Loans to UK mid-corporates supporting acquisitions, recapitalisations or general corporate purposes where higher leverage criteria were met.

Special purpose entities

The Group arranges securitisations to facilitate client transactions and

undertakes securitisations to sell financial assets or to fund specific

portfolios of assets. The Group also acts as an underwriter and depositor

in securitisation transactions involving both client and proprietary

transactions. In a securitisation, assets, or interests in a pool of assets,

are transferred generally to a special purpose entity (SPE) which then

issues liabilities to third party investors. SPEs are vehicles established for

aspecific, limited purpose, usually do not carry out a business or trade

and typically have no employees. They take a variety of legal forms -

trusts, partnerships and companies - and fulfil many different functions.

As well as being a key element of securitisations, SPEs are also used in

fund management activities to segregate custodial duties from the fund

management advice provided by the Group.

It is primarily the extent of risks and rewards assumed that determines

whether these entities are consolidated in the Group's financial

statements. The following section aims to address the significant

exposures which arise from the Group's activities through specific types

of SPEs.

The Group sponsors and arranges own-asset securitisations, whereby

the sale of assets or interests in a pool of assets into an SPE is financed

by the issuance of securities to investors. The pool of assets held by the

SPE may be originated by the Group, or (in the case of whole loan

programmes) purchased from third parties, and may be of varying credit

quality. Investors in the debt securities issued by the SPE are rewarded

through credit-linked returns, according to the credit rating of their

securities. The majority of securitisations are supported through liquidity

facilities, other credit enhancements and derivative hedges extended by

financial institutions, some of which offer protection against initial defaults

in the pool of assets. Thereafter, losses are absorbed by investors in the

lowest ranking notes in the priority of payments. Investors in the most

senior ranking debt securities are typically shielded from loss, since any

subsequent losses may trigger repayment of their initial principal.

The Group also employs synthetic structures, where assets are not sold

to the SPE, but credit derivatives are used to transfer the credit risk of the

assets to an SPE. Securities may then be issued by the SPE to investors,

on the back of the credit protection sold to the Group by the SPE.

Residential and commercial mortgages and credit card receivables form

the types of assets generally included in cash securitisations, while

corporate loans and commercial mortgages typically serve as reference

obligations in synthetic securitisations.

The Group sponsors own-asset securitisations primarily as a way of

diversifying funding sources. The Group purchases the securities issued

in own asset securitisations. During 2008, the Group was able to pledge

AAA rated asset-backed securities as collateral for repurchase

agreements with major central banks under schemes such as the Bank of

England's Special Liquidity Scheme, launched in April 2008, which

allowed banks to temporarily swap high-quality mortgage-backed and

other securities for liquid UK treasury bills. This practice contributed to

the Group's sources of funding in the face of the contraction in the UK

market for inter-bank lending, particularly during 2008 and 2009, and

investor base for securitisations.

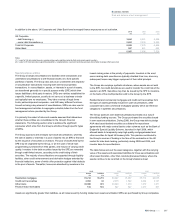

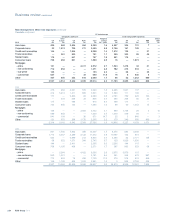

The table below sets out the asset categories, together with the carrying

value of the assets and associated liabilities for those securitisations and

other asset transfers, other than conduits (discussed below), where the

assets continue to be recorded on the Group's balance sheet

2010 2009 2008

Assets Liabilities Assets Liabilities Assets Liabilities

£m £m £m £m £m £m

Residential mortgages 76,212 18,215

69,927 15,937 55,714 20,075

Credit card receivables 3,993 34

2,975 1,592 3,004 3,197

Other loans 30,988 974

36,448 1,010 1,679 1,071

Finance lease receivables 510 510

597 597 1,077 857

Assets are significantly greater than liabilities, as all notes issued by funding related own asset securitisation SPEs are purchased by Group companies.

217RBS Group 2010

Business review

Risk and balance sheet management