RBS 2010 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

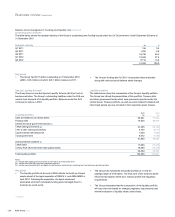

Balance sheet management: Funding and liquidity risk

All disclosures in this section (pages 134 to 145) are audited unless

indicated otherwise with an asterisk (*).

Introduction

The Group’s balance sheet composition is a function of the broad array of

product offerings and diverse markets served by its Core divisions. The

structural integrity of the balance sheet is augmented as needed through

active management of both asset and liability portfolios. The objective of

these activities is to optimise liquidity transformation in normal business

environments while ensuring adequate coverage of all cash requirements

under extreme stress conditions.

Diversification of the Group’s funding base is central to the liquidity

management strategy. The Group’s businesses have developed large

customer franchises, the largest being in the UK, US and Ireland but

extend into Europe, Asia and Latin America. Customer deposits provide

large pools of stable funding to support the majority of the Group’s

lending. It is a strategic objective to improve the Group’s loan to deposit

ratio to 100%, or better, by 2013.

The Group also accesses professional markets funding by way of public

and private debt issuances on an unsecured and secured basis. These

debt issuance programmes are spread across multiple currencies, and

maturities to appeal to a broad range of investor types, and preferences

around the world. This market based funding supplements the Group’s

structural liquidity needs and in some cases achieves certain capital

objectives.

Stress testing

Simulated liquidity stress testing is periodically performed for each

business and applied to the major operating subsidiary balance sheets. A

variety of firm-specific and market related scenarios are used at the

consolidated level and in individual countries. These scenarios include

assumptions about significant changes in key funding sources, credit

ratings, contingent uses of funding, and political and economic conditions

in certain countries. Stress tests are regularly updated based on

changing market conditions.

Contingency planning

The Group has a Contingency Funding Plan (CFP) which is maintained

and updated as the balance sheet evolves. The CFP is linked to stress

test results and forms the foundation for liquidity risk limits. Limits in the

business-as-usual environment are bounded by capacity to satisfy the

Group’s liquidity needs in the stress environments. The CFP provides a

detailed description of the availability, size and timing of all sources of

contingent liquidity available to the Group in a stress event. These are

ranked in order of economic impact and effectiveness to meet the

anticipated stress requirement. The CFP includes documented

procedures and sign-offs for actions that may require businesses to

provide access to customer assets for collateralized borrowing,

securitisation or sale. Roles and responsibilities for the effective

implementation of the CFP are also documented.

Liquidity reserves

The Group maintains liquidity reserves sufficient to satisfy cash

requirements in the event of a severe disruption in its access to either

wholesale or retail funding sources. The reserves consist of high quality

unencumbered government securities and cash held on deposit at central

banks. Government securities vary by type and jurisdiction based on

local regulatory considerations. The currency mix of the reserves reflects

the underlying balance sheet composition.

Regulatory oversight

The Group operates in multiple jurisdictions and is subject to a number of

regulatory regimes.

The Group's lead regulator is the Financial Services Authority (FSA). The

FSA implemented a new liquidity regime on 1 June 2010. The new rules

provide a standardised approach applied to all UK banks. At RBS, the

rules focus on the RBS UK Defined Liquidity Group (a subset comprising

the Group’s five main UK banks, The Royal Bank of Scotland plc,

National Westminster Bank Plc, Ulster Bank Limited, Coutts & Company

and Adam & Company) and cover adequacy of liquidity resources,

controls, stress testing and the Individual Liquidity Adequacy Assessment

(ILAA) process. The ILAA informs the Board and FSA of the assessment

and quantification of the Group’s liquidity risks and their mitigation, and

how much current and future liquidity is required. The ILAA was approved

by the Board in November 2010. The FSA is expected to issue ‘Individual

Liquidity Guidance’ to the Group in 2011.

In the US, the Group’s operations are required to meet liquidity

requirements set out by the US Federal Reserve Bank, Office of the

Comptroller of the Currency, Federal Deposit Insurance Corporation and

Financial Industry Regulatory Authority. In the Netherlands, the Group is

subject to the De Nederlandsche Bank liquidity oversight regime.

Regulatory developments*

There have been a number of significant developments in the regulation

of liquidity risk.

In December 2010, the BCBS issued the ‘International framework for

liquidity risk measurement, standards and monitoring’ which confirmed

the introduction of two liquidity ratios, the liquidity coverage ratio (LCR)

and the net stable funding ratio (NSFR). The introduction of both of these

will be subject to an observation period, which includes review clauses to

address and identify any unintended consequences.

After an observation period beginning in 2011, the LCR, including any

revisions, will be introduced on 1 January 2015. The NSFR, including any

revisions, will move to a minimum standard by 1 January 2018.

*unaudited

RBS Group 2010134

Business review continued