RBS 2010 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Risk management: Credit risk continued

Global Restructuring Group continued

Depending on the case in question, GRG may employ a combination of

these options in order to achieve the best outcome. It may also consider

alternative approaches, either alone or together with the options listed

above.

The following are generally considered as options of last resort:

xEnforcement of security or otherwise taking control of assets: where

the Group holds underlying collateral or other security interest and is

entitled to enforce its rights, it may take ownership or control of the

assets. The Group’s preferred strategy is to consider other possible

options prior to exercising these rights.

xInsolvency: where there is no suitable restructuring option or the

business is no longer regarded as sustainable, insolvency will be

considered. Insolvency may be the only option that ensures that the

assets of the business are properly and efficiently distributed to

relevant creditors.

As discussed above, GRG will consider a range of possible restructuring

strategies. At the time of execution, the ultimate outcome of the strategy

adopted is unknown and highly dependent on the cooperation of the

borrower and the continued existence of a viable business. The

customer’s financial position, its anticipated future prospects and the

likely effect of the restructuring including any concessions are considered

by the GRG relationship manager to establish whether an impairment

provision is required, subject to divisional and Group governance.

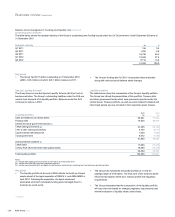

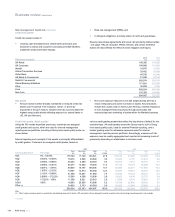

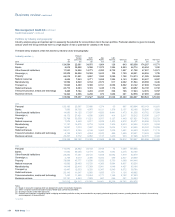

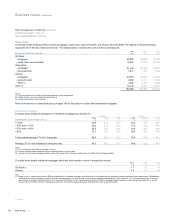

During 2010, GRG completed corporate loan restructurings totalling £6.2

billion (exposures of more than £5 million) of which £2.7 billion were

classified as impaired. Of these restructurings £2.4 billion related to

commercial real estate and £2.1 billion to manufacturing. The incidence

of the main types of arrangements is analysed below:

%of loans

(by value)

Term extensions 54

Debt forgiveness 25

Debt for equity 23

Interest rate concessions and payment moratoriums 36

The total above exceeds 100% as an individual case can involve more

than one type of arrangement.

Transfer of restructured loans to the performing book follows assessment

by relationship managers in GRG. All cases are individually assessed;

when no further losses are expected the loan is returned to performing

status. Restructured loans that carry an impairment provision remain

classified as impaired. Of the £3.5 billion of corporate loans that were

transferred to the performing book with a concession during 2010, loans

amounting to £1.8 billion had a negotiated margin increase as

compensation for concessions granted.

Retail collections and recoveries

There are collections and recoveries functions in each of the consumer

businesses. Their role is to provide support and assistance to customers

who are currently experiencing difficulties in meeting their financial

obligations. Where possible, the aim of the collections and recoveries

teams is to return the customer to a satisfactory position, by working with

them to restructure their finances. If this is not possible, the team has the

objective of reducing the loss to the Group.

Forbearance*

The Group’s retail forbearance activities involve granting various contract

revisions not normally available, such as reduced repayments, payment

moratoriums and the roll up of arrears, principally to retail customers with

secured lending that are experiencing temporary financial difficulties.

Loans are identified for forbearance primarily as a result of contact from

the customer or payment arrears and it is only granted following an

assessment of the customer’s ability to pay. For those loans that are

classified as impaired, the Group’s objective is to minimise the loss on

these accounts; for currently performing loans the aim is to enable the

customer to continue to service the loan.

Forbearance lending for which an impairment loss provision has been

recognised remains classified as non-performing. Where the customer

met the loan terms prior to modification and where there is an expectation

that the customer will meet the revised terms, these loans are classified

as performing loans.

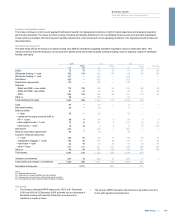

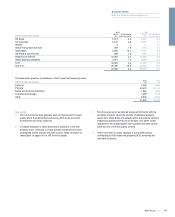

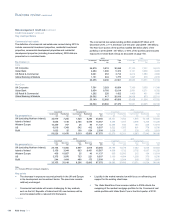

Retail loan forbearance arrangements during 2010 totalled £3.3 billion

(residential mortgages £3.1 billion), of which £1.0 billion were classified

as impaired. The incidence of the main types of retail forbearance is

analysed below.

%of loans

(by value)

Reduced repayments 59

Payment moratoriums 20

Roll up of arrears 19

Interest reductions 6

Term extensions 3

The total exceeds 100% as an individual case can involve more than one

type of arrangement.

Of the forbearance arrangements agreed in the performing book during

2010, less than 15% were impaired as at 31 December 2010.

*unaudited

RBS Group 2010148

Business review continued