RBS 2010 Annual Report Download - page 196

Download and view the complete annual report

Please find page 196 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

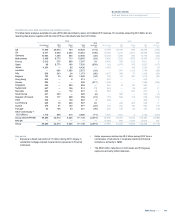

Risk management: Market risk continued

Risk measurement and control continued

The Global Market Risk Stress Testing Committee reviews and discusses

all matters relating to Market Risk Stress Testing. Stress test exposures

are discussed with senior management and relevant information is

reported to the Group Risk Committee, Executive Risk Forum and the

Board. Breaches in the Group’s market risk stress testing limits are

monitored and reported.

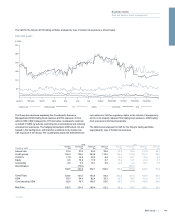

In addition to VaR and stress testing, the Group calculates a wide range

of sensitivity and position risk measures, for example interest rate ladders

or option revaluation matrices. These measures provide valuable

additional controls, often at individual desk or strategy level.

Model validation governance

Pricing models are developed and owned by the front office. Where

pricing models are used as the basis of books and records valuations,

they are all subject to independent review and sign-off. Models are

assessed by the Group Model Product Review Committee (GMPRC) as

having either immaterial or material model risk (valuation uncertainty

arising from choice of modelling assumptions), the assessment being

made on the basis of expert judgement. Those models assessed as

having material model risk are prioritised for independent quantitative

review. Independent quantitative review aims to quantify model risk (i.e.

the impact of missing risk factors in the front office model or the

possibility that we may be mismarking these products relative to other

market participants who may be using an alternative model) by

comparing model outputs against alternative independently developed

models. The results of the independent quantitative review are used by

Market Risk to inform risk limits and by Finance to inform reserves.

Governance over this process is provided by GMPRC, a forum which

brings together Front Office Quantitative Analysts, Market Risk, Finance

and Quantitative Research Centre (QuaRC), Group Risk’s independent

quantitative model review function.

Risk (market risk, incremental default risk, counterparty credit risk)

models are developed both within business units and by Group functions.

Risk models are also subject to independent review and sign-off.

Meetings are held with the FSA every quarter to discuss the traded

market risk, including changes in models, management, back testing

results, risks not included in the VaR framework and other model

performance statistics.

As part of the ongoing review and analysis of the suitability of the VaR

model, a methodology enhancement to the ABS VaR was approved and

incorporated into the regulatory model in 2010. The credit crisis in 2007 -

2009 caused large price changes for some structured bonds and the

spread based approach to calculating VaR for these instruments started

to give inaccurate risk levels, particularly for bonds trading at a significant

discount to par. The methodology enhancement harmonised the VaR

approach in the US and Europe by replacing the absolute spread-based

approach with a more reliable and granular relative price-based mapping

scheme. The enhancement better reflects the risk in the context of

position changes, downgrades and vintage as well as improving

differentiation between prime, Alt-A and sub-prime exposures.

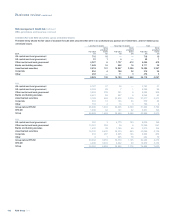

The VaR disclosure is broken down into trading and non-trading portfolios.

Trading VaR relates to the main trading activities of the Group and non-

trading reflects the risk associated with reclassified assets, money market

business and the management of internal funds flow within the Group’s

businesses.

Traded portfolios

The primary focus of the Group’s trading activities is to provide an

extensive range of debt and equity financing, risk management and

investment services to its customers, including major corporations and

financial institutions around the world. The Group undertakes these

activities organised along six principal business lines: money markets;

rates flow trading; currencies and commodities; equities; credit markets;

and portfolio management & origination.

Financial instruments held in the Group’s trading portfolios include, but

are not limited to: debt securities, loans, deposits, equities, securities sale

and repurchase agreements and derivative financial instruments (futures,

forwards, swaps and options).

The Group participates in exchange traded and over-the-counter (OTC)

derivatives markets. The Group buys and sells financial instruments that

are traded or cleared on an exchange, including interest rate swaps,

futures and options. Holders of exchange traded instruments provide

margin daily with cash or other security at the exchange, to which the

holders look for ultimate settlement.

The Group also buys and sells financial instruments that are traded OTC,

rather than on a recognised exchange. These instruments range from

commoditised transactions in derivative markets, to trades where the

specific terms are tailored to the requirements of the Group’s customers.

In many cases, industry standard documentation is used, most commonly

in the form of a master agreement, with individual transaction

confirmations.

Assets and liabilities in the trading book are measured at their fair value.

Fair value is the amount at which the instrument could be exchanged in a

current transaction between willing parties. The fair values are

determined following IAS 39 guidance which requires banks to use

quoted market prices or valuation techniques (models) that make the

maximum use of observable inputs. When marking to market using a

model, the valuation methodologies are reviewed and approved by the

market risk function. Group Risk provides an independent evaluation of

the model for transactions deemed by the Group Model Product Review

Committee (GMPRC) to be large, complex and/or innovative. Any profits

or losses on the revaluation of positions are recognised in the daily profit

and loss.

RBS Group 2010194

Business review continued