RBS 2010 Annual Report Download - page 199

Download and view the complete annual report

Please find page 199 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Non-traded portfolios

VaR is not always the most appropriate measure of risk for assets in the

non-trading book, particularly for those in Non-Core which will diminish

over time as the asset inventory is sold down.

In order to better represent the risk of the non-traded portfolios, the table

below analyses the VaR for the non-trading portfolios but excludes

Structured Credit Portfolios (SCP) in Non-Core. These assets are shown

separately on a drawn notional and fair value basis by maturity profile

and asset class and are managed on both an asset and RWA basis.

Also excluded from the non-traded VaR are the loans and receivables

products that are managed within the credit risk management framework.

The 2009 and 2010 VaR data below is shown on this basis; however the

VaR data for the 2008 period could not be recalculated excluding the

SCP and LAR portfolios mentioned above due to data and system

constraints.

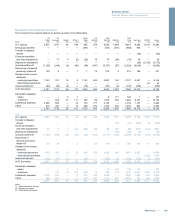

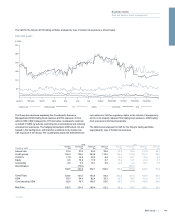

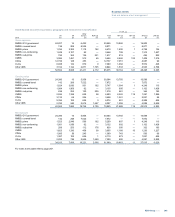

The table below analyses the risk for the Group’s non-trading portfolios.

2010 2009

Non-trading VaR Average

£m

Period end

£m

Maximum

£m

Minimum

£m

Average

£m

Period end

£m

Maximum

£m

Minimum

£m

Interest rate 8.7 10.4 20.5 4.4 13.0 13.9 26.3 7.7

Credit spread 32.0 16.1 101.2 15.4 81.7 100.3 131.5 39.7

Currency 2.1 3.0 7.6 0.3

1.4 0.6 7.0 0.2

Equity 1.2 3.1 4.6 0.2

3.3 2.2 5.8 1.6

Diversification (15.9) (20.4)

30.9 16.7 98.0 13.7 80.4 96.6 126.9 46.8

Core 30.5 15.6 98.1 12.8

78.4 95.9 126.9 46.8

Non-Core 1.3 2.8 4.1 0.2

3.5 1.9 16.9 —

Key points

xThe non-traded credit spread, Core and total VaR have decreased

significantly due to the implementation of the relative price-based

mapping scheme in the VaR methodology discussed above and the

sales of available-for-sale securities in the US mortgage business.

xThe business model for the US mortgage business has focussed its

activity on client facilitation flow trading during 2010. This has

encompassed the disposal of a large portfolio of illiquid available-for-

sale securities that were sold throughout the year, resulting in the

non-traded VaR reducing. In parallel, the risk management of the

business has been significantly enhanced to ensure that the

business remains focussed on client facilitation flow trading of liquid

assets. Tools have been implemented to monitor the liquidity of

trading volumes, asset aged inventory controls have been tightened

and granular asset concentration risk limits imposed, to complement

the existing VaR and stress testing market risk frameworks.

197RBS Group 2010

Business review

Risk and balance sheet management