RBS 2010 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

RBS Group 201016

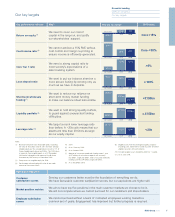

The economic environment

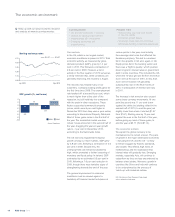

MKeep up with our latest economic research

and analysis at www.rbs.com/economics Current position

• UK and US economies in recovery

• Outlook for gradual improvement

• Indebtedness still a headwind

• Emerging economics still

outperforming

Possible risks

• Interest rates stay near zero bound,

or rise too rapidly

• Economic growth falters

• Sovereign credit risks not controlled

• Wholesale funding conditions deteriorate

GDP growth (%, real terms)

-4.9

-2.6

1.3

2.8

-10

-8

-6

-4

-2

0

2

4

UK

2009

Source: Datastream

2010

UK

US

US

Sterling exchange rates

1.00

1.15

1.30

1.45

1.60

1.75

Jan 2010 Dec 2010

$ to £1 €to £1

Our markets

In the UK, which is our largest market,

economic conditions improved in 2010. Total

economic activity, as measured by gross

domestic product (GDP), grew by 1.3 per

cent in 2010. This followed a contraction of

4.9 per cent in 2009. However, a fall in

activity in the final quarter of 2010 served as

a timely reminder that, while conditions are

generally improving, the recovery is fragile.

The recovery has helped many of our

customers. Company trading profits grew for

the first time since 2008. The unemployment

rate levelled off at around 8 per cent, which

is much higher than at the start of the

recession, but still relatively low compared

with the peak in other recessions. These

factors supported commercial property

prices, which were 6 per cent higher in

December 2010 than they were a year earlier,

according to International Property Databank.

Most of those gains came in the first half of

the year. The residential market was less

robust: house prices fell in the second half of

the year, dragging the year-on-year growth

rate to -1 per cent in December 2010,

according to the Nationwide index.

The US economy registered the fastest

growth among our main markets. GDP grew

by 2.8 per cent, following a contraction of 2.6

per cent in 2009. Despite this, the

unemployment rate remained stubbornly

high, which prompted a further loosening of

monetary and fiscal policy. In Ireland, GDP

contracted by an estimated 0.5 per cent in

2010, following a 7.6 per cent reduction in

2009, though there were tentative signs of

strengthening towards the end of the year.

The general improvement in economic

conditions must be viewed against a

backdrop of financial market turbulence at

various points in the year, most notably

the sovereign debt crisis that affected the

Eurozone periphery. This led to a marked

fall in risk appetite in Q2 and, again, in Q4.

Equity prices fell in the banking sector and

there was a ‘flight to quality’, which pushed

down long-term interest rates on government

debt in some countries. This included the UK,

where the 10-year gilt rate fell from more than

4 per cent at the start of 2010, to less than

3 per cent in October. UK gilt yields

subsequently rose in the final months of

2010, in anticipation of interest rate rises

in 2011.

The increase in risk aversion also caused

some sharp currency movements. At one

point the pound was 11 per cent down

against the dollar, but sterling rallied in the

second half of 2010, to end the year just

slightly lower than where it started ($1.57

from $1.61). Sterling rose by 10 per cent

against the euro in the first half of the year,

before giving up most of these gains, to

end the year at €1.17 (from €1.13).

The economic outlook

We expect the global recovery to be

maintained, but to remain uneven. The pace

of growth in the major developed economies

– including the UK and the US – is likely

to remain sluggish by historic standards,

and volatile. This reflects high levels of

indebtedness and the expectation that

interest rates will gradually rise. Emerging

markets, especially Asia, will continue to

outperform as they are less encumbered by

balance sheet strains. Moreover, growth in

countries like China and India will continue

to be underpinned by the process of

‘catch-up’ with industrial nations.

N.B. All data are from Thomson Datastream

unless otherwise indicated.