RBS 2010 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Key points

xExposure to monolines decreased over the period due to a

combination of restructuring certain exposures and higher prices of

underlying reference instruments, partially offset by the

strengthening of the US dollar against sterling.

xThe CVA decreased on a total basis, reflecting the reduction in

exposure, but was stable on a relative basis with the impact of

tighter credit spreads offset by an increase in the expected lives of

certain trades.

xThe reduction in the Group’s RWA requirements over the quarter

was driven by the reduction in exposure to monolines and the

impact of restructuring certain risk structures.

xDuring the year there was a significant increase in the RWA

requirements of RBS N.V. following its migration to the Basel II

regime. Regulatory intervention at certain monoline counterparties

triggered International Swaps and Derivative Association (ISDA)

credit events in the period. At the point of trigger the exposure to

these counterparties was excluded from the RWA calculations and

capital deductions of £171 million were taken instead. The impact of

this together with restructuring certain exposures and an

improvement in the rating of underlying reference bonds held by the

Group to investment grade status were the main drivers of the

reduction in RWA requirements during the second half of the year. *

The Group also has indirect exposures to monoline insurers through

wrapped securities and other assets with credit enhancement from

monoline insurers. These securities are traded with the benefit of this

credit enhancement. Any deterioration in the credit rating of the monoline

is reflected in the fair value of these assets.

Credit derivative product companies

Acredit derivative product company (CDPC) is a company that sells

protection on credit derivatives. CDPCs are similar to monoline insurers,

however, they are not regulated as insurers.

The Group has purchased credit protection from CDPCs through

tranched and single name credit derivatives. The Group's exposure to

CDPCs is predominantly due to tranched credit derivatives (“tranches”). A

tranche references a portfolio of loans and bonds and provides protection

against total portfolio default losses exceeding a certain percentage of

the portfolio notional (the attachment point) up to another percentage (the

detachment point).

The Group has predominantly traded senior tranches with CDPCs, the

average attachment and detachment points are 13% and 49%

respectively (2009 - 15% and 51% respectively; 2008 - 16% and 50%

respectively), and the majority of the loans and bonds in the reference

portfolios are investment grade.

The gross mark-to-market of the CDPC protection is determined using

industry standard models. The methodology employed to calculate the

CDPC CVA is different to that outlined above for monolines, as there are

no market observable credit spreads and recovery levels for these

entities. The level of expected loss on CDPC exposures is estimated with

reference to recent market events impacting CDPCs, including

communication activity, and by analysing the underlying trades and the

cost of hedging expected default losses in excess of the capital in each

vehicle.

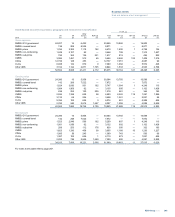

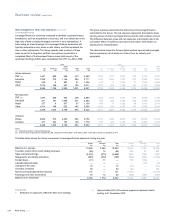

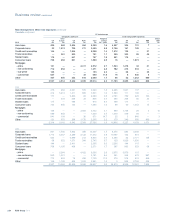

Asummary of the Group's exposure to CDPCs all of which are in Non-

Core is detailed below.

2010

£m

2009

£m

2008

£m

Gross exposure to CDPCs 1,244 1,275 4,776

Credit valuation adjustment (490) (499) (1,311)

Net exposure to CDPCs 754 776 3,465

Credit valuation adjustment as a % of gross exposure 39% 39% 27%

Counterparty and credit risk RWAs*£7.2bn £7.5bn £5.0bn

Capital deductions*£280m £347m —

*unaudited

213RBS Group 2010

Business review

Risk and balance sheet management