RBS 2010 Annual Report Download - page 163

Download and view the complete annual report

Please find page 163 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

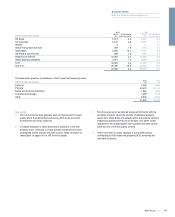

Ulster Bank Group (Core and Non-Core)*

Ulster Bank Group accounts for 8% of the Group’s total credit risk assets

or 7% of the Group’s Core credit risk assets. The Irish economy has

experienced severe economic headwinds resulting in a substantial rise in

unemployment and a steep property value correction over the last two

years. Ulster Bank Group has not been immune to the downturn which

has resulted in a significant migration of credit quality to lower grades and

asubstantial increase in loan impairments. Ulster Bank Group’s

commercial real estate and mortgage portfolios have been acutely

affected and these account for 81% of the 2010 impairment charges

(2009 - 75%).

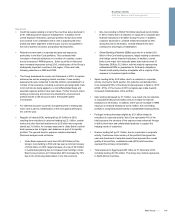

Core

Impairment charges increased by£512 million at 31 December 2009 to

£1,161 million at 31 December 2010, reflecting the deteriorating

economic environment in Ireland with rising default levels across both

personal and corporate portfolios. Lower asset values, particularly

property related, together with pressure on borrowers with a dependence

on consumer spending have resulted in higher corporate loan losses

while higher unemployment, lower incomes and increased taxation have

driven mortgage impairment increases. Ulster Bank Group is helping

customers in this difficult environment. Forbearance policies which are

deployed through the 'Flex' initiative are aimed at assisting customers in

financial difficulty. These policies have been reviewed in 2010 given the

structural problem that exist in Ireland with the scale and duration of

customers in financial difficulty. The industry definition in the Republic of

Ireland of an unsustainable mortgage (18 months accumulated interest)

has been used to underpin the policy which will improve identification of

customers where forbearance may not be appropriate. The forbearance

portfolios account for 5.8% (7,383 mortgages) of the Ulster Bank Group

mortgage portfolio (by value) at 31 December 2010 with 75% of these

customers (by value) in amortising or interest only agreements.

Non-Core

Impairment charges increased from£1,277 million at 31 December 2009

to £2,682 million at 31 December 2010, reflecting the deteriorating

economic environment in Ireland with rising default levels across the

portfolio. Lower asset values, in property related lending and most

specifically in development lending have resulted in higher corporate loan

losses.

In the third quarter of 2010, £6.1 billion of residential mortgages and

some corporate exposures were transferred from Non-Core to Core; at

the same time £5 billion of commercial real estate loans were transferred

from Core to Non-Core.

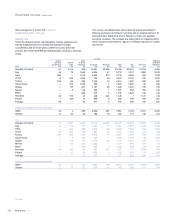

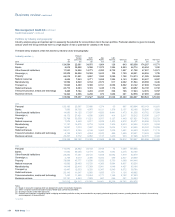

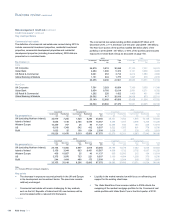

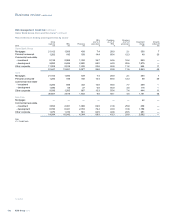

Credit risk assets by industry and geography

Credit risk assets include £51 billion and £3 billion of lending to customers and financial institutions respectively, with the remaining exposure company

RRM and contingent obligations.

Republic of Ireland UK Other Total

Core

Non-

Core Total Core

Non-

Core Total Core

Non-

Core Total Core

Non-

Core Total

Industry sector (1) £m £m £m £m £m £m £m £m £m £m £m £m

2010

Personal 20,064 120 20,184 2,730 22 2,752 5 — 5 22,799 142 22,941

Banks 107 — 107 3 — 3 14 — 14 124 — 124

Non-banks and financial

institutions 167 88 255 46 24 70 4 — 4 217 112 329

Sovereign (2) 2,174 — 2,174 672 — 672 — — — 2,846 — 2,846

Property 3,609 8,431 12,040 2,704 4,281 6,985 305 770 1,075 6,618 13,482 20,100

Retail and leisure 1,923 608 2,531 795 75 870 108 — 108 2,826 683 3,509

Other Corporate 4,033 338 4,371 1,089 88 1,177 198 — 198 5,320 426 5,746

32,077 9,585 41,662 8,039 4,490 12,529 634 770 1,404 40,750 14,845 55,595

2009

Personal 16,008 6,302 22,310 2,782 24 2,806 4 — 4 18,794 6,326 25,120

Banks 99 — 99 4 — 4 28 — 28 131 — 131

Non-banks and financial

institutions 190 19 209 170 16 186 3 — 3 363 35 398

Sovereign (2) 1,909 — 1,909 347 — 347 — — — 2,256 — 2,256

Property 6,686 5,852 12,538 4,540 2,635 7,175 759 413 1,172 11,985 8,900 20,885

Retail and leisure 2,638 288 2,926 579 22 601 126 — 126 3,343 310 3,653

Other Corporate 4,145 228 4,373 894 72 966 131 — 131 5,170 300 5,470

31,675 12,689 44,364 9,316 2,769 12,085 1,051 413 1,464 42,042 15,871 57,913

Notes:

(1) In the third quarter of 2010, £6.1 billion of residential mortgages and some corporate exposures were transferred from Non-Core; at the same time £5 billion of commercial real estate loans were

transferred from Core to Non-Core.

(2) Includes central bank exposures.

161RBS Group 2010

Business review

Risk and balance sheet management