RBS 2010 Annual Report Download - page 213

Download and view the complete annual report

Please find page 213 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

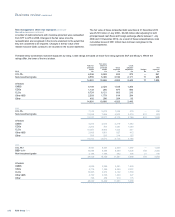

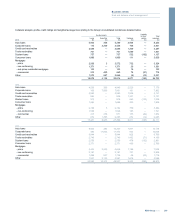

Credit valuation adjustments (CVA)

CVA represents an estimate of the adjustment to arrive at fair value that a market participant would make to incorporate the credit risk inherent in

counterparty derivative exposures.

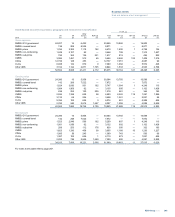

The table below details the Group’s CVA by type of counterparty.

2010

£m

2009

£m

2008

£m

Monoline insurers 2,443 3,796 5,988

CDPCs 490 499 1,311

Other counterparties 1,714 1,588 1,738

4,647 5,883 9,037

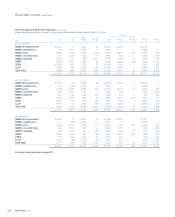

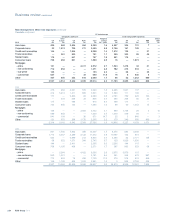

Monoline insurers

The Group has purchased protection from monoline insurers

(“monolines”), mainly against specific ABS. Monolines specialise in

providing credit protection against the principal and interest cash flows

due to the holders of debt instruments in the event of default by the debt

instrument counterparty. This protection is typically held in the form of

derivatives such as credit default swaps (CDSs) referencing underlying

exposures held directly or synthetically by the Group.

The gross mark-to-market of the monoline protection depends on the

value of the instruments against which protection has been bought. A

positive fair value, or a valuation gain, in the protection is recognised if

the fair value of the instrument it references decreases. For the majority

of trades the gross mark-to-market of the monoline protection is

determined directly from the fair value price of the underlying reference

instrument, however for the remainder of the trades, the gross mark-to-

market is determined using industry standard models.

The methodology employed to calculate the monoline CVA uses market

implied probability of defaults and internally assessed recovery levels to

determine the level of expected loss on monoline exposures of different

maturities. The probability of default is calculated with reference to

market observable credit spreads and recovery levels. CVA is calculated

at a trade level by applying the expected loss, corresponding to each

trade’s expected maturity, to the gross mark-to-market of the monoline

protection. The expected maturity of each trade reflects the scheduled

notional amortisation of the underlying reference instruments and

whether payments due from the monoline are received at the point of

default or over the life of the underlying reference instruments.

The table below summarises the Group's exposure to monolines, all of

which are in Non-Core.

2010

£m

2009

£m

2008

£m

Gross exposure to monolines 4,023 6,170 11,581

Hedges with financial institutions (71) (531) (789)

Credit valuation adjustment (2,443) (3,796) (5,988)

Net exposure to monolines 1,509 1,843 4,804

Credit valuation adjustment as a % of gross exposure 61% 62% 52%

Counterparty and credit risk RWAs*£17.8bn £13.7bn £7.3bn

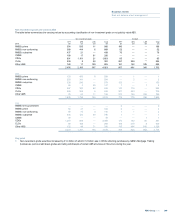

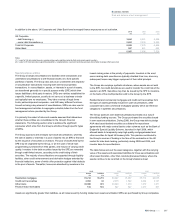

The net income statement effect relating to monoline exposures is detailed below.

2010 2009 2008

£m £m £m

Credit valuation adjustment at 1 January (3,796) (5,988) (862)

Credit valuation adjustment at 31 December (2,443) (3,796) (5,988)

Decrease/(increase) in credit valuation adjustment 1,353 2,192 (5,126)

Net debit relating to realisations, hedges, foreign exchange and other movements (844) (3,290) (347)

Net (debit)/credit relating to reclassified debt securities (305) (1,468) 1,916

Net credit/(debit) to income statement (1) 204 (2,566) (3,557)

Note:

(1) Comprises the following elements for the year ended 2010 and 2009:

- a loss of £5 million (2009 - £2,387 million) in income from trading activities;

-impairment reversals/(losses) of £71 million (2009 - (£239) million); and

-other income of £138 million (2009 - £60 million) relating to reclassified debt securities.

*unaudited

211RBS Group 2010

Business review

Risk and balance sheet management