RBS 2010 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Expected losses are applied to estimated potential future exposures

which are modelled to reflect the volatility of the market factors which

drive the exposures and the correlation between those factors. Potential

future exposures arising from vanilla products (including interest rate and

foreign exchange derivatives) are modelled jointly using the Group's core

counterparty risk systems. The majority of the Group's CVA held in

relation to other counterparties arises on these vanilla products. The

exposures arising from all other product types are modelled and

assessed individually. The potential future exposure to each counterparty

is the aggregate of the exposures arising on the underlying product types.

The correlation between exposure and counterparty risk is also

incorporated within the CVA calculation where this risk is considered

significant. The risk primarily arises on trades with emerging market

counterparties where the gross mark-to-market value of the trade, and

therefore the counterparty exposure, increases as the strength of the

local currency declines.

Collateral held under a credit support agreement is factored into the CVA

calculation. In such cases where the Group holds collateral against

counterparty exposures, CVA is held to the extent that residual risk

remains.

CVA is held against exposures to all counterparties with the exception of

the CDS protection that the Group has purchased from HM Treasury, as

part of its participation in the Asset Protection Scheme, due to the unique

features of this derivative.

The net income statement effect arising from the change in level of CVA

for all other counterparties and related trades is shown in the table below.

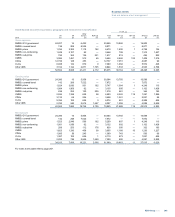

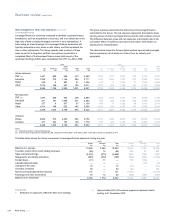

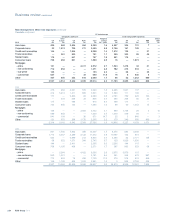

2010 2009

£m £m

Credit valuation adjustment at 1 January (1,588) (1,738)

Credit valuation adjustment at 31 December (1,714) (1,588)

(Increase)/decrease in credit valuation adjustment (126) 150

Net debit relating to realisations, hedges, foreign exchange and other movements (19) (841)

Income from trading activities - net losses (145) (691)

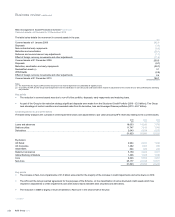

Key points

xThe increase in CVA held against exposures to other counterparties

was driven by rating downgrades of certain counterparties and the

net impact of changes in credit spreads and counterparty exposures

due to market moves. This increase was partially offset by a

decrease due to the disposal of parts of the RBS Sempra

Commodities JV business during the year.

xLosses on hedges and realised defaults are the primary driver of the

loss arising on foreign exchange, hedges, realisations and other

movements.

215RBS Group 2010

Business review

Risk and balance sheet management