RBS 2010 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Interest rate risk

The banking book consists of interest bearing assets, liabilities and

derivative instruments used to mitigate risks which are accounted for on

an accrual basis, as well as non-interest bearing balance sheet items

which are not subjected to fair value accounting.

The Group provides financial products to satisfy a variety of customer

requirements. Loans and deposits are designed to meet customer

objectives with regard to repricing frequency, tenor, index, prepayment,

optionality and other features. These characteristics are aggregated to

form portfolios of assets and liabilities with varying degrees of sensitivity

to changes in market rates. Mismatches in these sensitivities give rise to

net interest income (NII) volatility as the level of interest rates rise and fall.

For example, a bank with a floating rate loan portfolio and largely fixed

rate deposits will see its NII rise as interest rates rise and fall as rates

decline. Due to the long-term nature of many banking book portfolios,

layered repricing characteristics and maturities, it is likely the NII will vary

from period to period even with no change in market rate level. New

business volumes originated in any period will alter the interest rate

sensitivity of a bank if it differs from portfolios originated in prior periods.

Interest rate risk in the banking book (IRRBB) is assessed using a set of

standards to define, measure and report the market risk. It is the Group’s

policy to minimise interest rate sensitivity in banking book portfolios and

where interest rate risk is retained to ensure that appropriate measures

and limits are applied. Key conventions in evaluating IRRBB are

subjected to approval of divisional ALCOs and GALCO. Limits on IRRBB

are proposed by the Group Treasurer for approval by ERF annually.

IRRBB is measured using a version of the same VaR methodology that is

used for the Group’s trading portfolios. Net interest income exposures are

measured in terms of sensitivity over time to movements in interest rates.

Additionally, Citizens measures the sensitivity of the market value of

equity to changes in forward interest rates.

Divisions with the exception of Citizens and GBM are required to manage

banking book exposures through internal transactions with Group

Treasury to the greatest extent possible. Residual risks in divisions must

be measured and reported as described.

Group Treasury aggregates exposures arising from its own external

activities and positions transferred in from divisions. Where appropriate,

Group Treasury nets offsetting risk exposures to determine a residual

exposure to rate movements. Hedging transactions using cash and

derivative instruments are executed to manage within the GALCO

approved VaR limits.

Citizens and GBM manage their own IRRBB exposures within approved

limits to satisfy their business objectives.

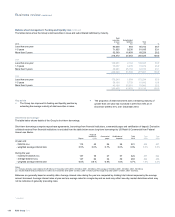

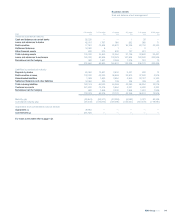

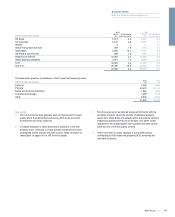

IRRBB VaR for the Group's retail and commercial banking activities at a

99% confidence level was as follows:

Average Period end Maximum Minimum

£m £m £m £m

2010 57.5 96.2 96.2 30.0

2009 85.5 101.3 123.2 53.3

2008 130.0 76.7 197.4 76.7

Abreakdown of the Group's IRRBB VaR by currency is shown below.

Currency 2010

£m

2009

£m

2008

£m

EUR 32.7 32.2 30.9

GBP 79.3 111.2 26.0

USD 120.6 42.1 57.9

Other 9.7 9.0 14.0

Key points

xInterest rate exposure at 31 December 2010 was slightly lower than at the end of 2009. The average exposure in 2010 was 33% below the

average for 2009.

xIn general, actions taken throughout 2010 to mitigate earnings sensitivity from interest rate movements were executed in US dollars, hence the

year on year shift in VaR by currency.

143RBS Group 2010

Business review

Risk and balance sheet management