RBS 2010 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

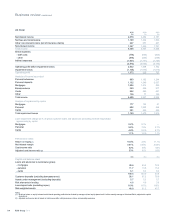

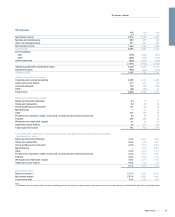

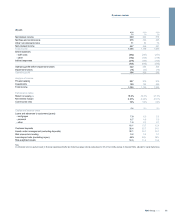

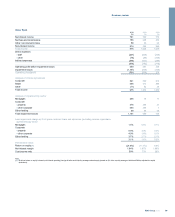

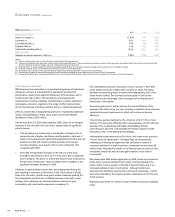

Ulster Bank continued

2010 2009 2008

£bn £bn £bn

Capital and balance sheet

Loans and advances to customers (gross)

- mortgages 21.2 16.2 18.1

- corporate

- property 5.4 10.1 10.9

- other corporate 9.0 11.0 12.9

- other lending 1.3 2.4 2.1

36.9 39.7 44.0

Customer deposits 23.1 21.9 24.3

Risk elements in lending

- mortgages 1.5 0.6 0.3

- corporate

- property 0.7 0.7 0.5

- other corporate 1.2 0.8 0.3

- other lending 0.2 0.2 0.1

3.6 2.3 1.2

Loan:deposit ratio (excluding repos) 152% 177% 179%

Risk-weighted assets 31.6 29.9 24.5

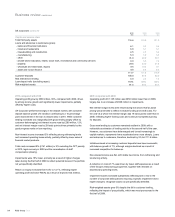

2010 compared with 2009

Overall performance deteriorated in 2010, largely as a result of an

increase in impairment losses of £512 million. Operating profit before

impairment increased to £400 million, up 50% in constant currency terms,

driven by the culmination of a bank-wide cost saving programme during

2010.

Net interest income increased by 1% on a constant currency basis as

actions to increase asset margins were largely eroded by tightening

deposit margins due to intensive market competition.

Non-interest income was 14% lower on a constant currency basis

reflecting a non-recurring gain in 2009.

Loans to customers fell by 5% in constant currency terms. On 1 July

2010 the division transferred a portfolio of development property assets

to the Non-Core division, partially offset by a simultaneous transfer of a

portfolio of retail mortgage assets to the core business.

Despite intense competition, customer deposit balances increased by 8%

in constant currency terms over the year with strong growth across all

deposit categories, driven by a focus on improving the bank’s funding

profile.

Expenses at constant exchange rates were 22% lower. The strong year-

on-year performance in expenses was primarily driven by an increased

focus on active management of the cost base, and the benefits derived

from the business restructuring and cost-saving programme which

commenced in 2009.

Impairment losses increased by £512 million to £1,161 million reflecting

the deteriorating economic environment in Ireland and rising default

levels across both personal and corporate portfolios. Lower asset values,

particularly in property-related lending together with pressure on

borrowers with a dependence on consumer spending have resulted in

higher corporate loan losses, while higher unemployment, lower incomes

and increased taxation have driven mortgage impairment increases.

Risk-weighted assets have increased due to deteriorating credit risk

metrics.

Customer numbers increased by 3% during 2010, with a strong

performance in current and savings accounts switchers.

2009 compared with 2008

Operating results were in line with expectations but deteriorated during

2009 as economic conditions across the island of Ireland worsened, with

an operating loss for the year of £368 million.

Net interest income declined by 7% in constant currency terms, largely as

aresult of tightening deposit margins in an increasingly competitive

market, partly offset by asset repricing initiatives. Net interest margin for

the year at 1.87% remained broadly stable despite the challenging

market conditions.

At constant exchange rates loans to customers decreased by 4% from

the prior year as new business demand weakened. Customer deposits

reduced by 5% in 2009 in constant currency terms, reflecting an

increasingly competitive Irish deposit market and reductions in wholesale

funding during Q1. During the second half of the year the market

stabilised and the division recorded strong growth in customer balances

resulting in an improved funding profile.

RBS Group 201090

Business review continued