RBS 2010 Annual Report Download - page 202

Download and view the complete annual report

Please find page 202 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Risk management: Operational risk* continued

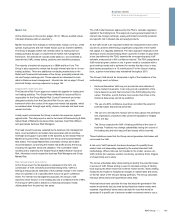

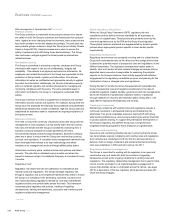

Through the three lines of defence model the Group obtains assurance

that the standards in the GPF are being adhered to. GPF defines

requirements for testing and gathering evidence which demonstrates that

each division and function is appropriately controlled.

GPF is owned and managed by the Group’s operational risk function and

relies upon the operational risk framework for effective implementation

and ongoing maintenance.

Three lines of defence model

To ensure appropriate responsibility is allocated for the management, reporting and escalation of operational risk, the Group operates a three lines of

defence model which outlines principles for the roles, responsibilities and accountabilities for operational risk management.

1st line of defence

The business

2nd line of defence

Operational risk

3rd line of defence

Group Internal Audit

Accountable for the ownership and day-to-day

management and control of operational risk.

Responsible for implementing processes in

compliance with Group policies.

Responsible for testing key controls and

monitoring compliance with Group policies.

Responsible for the implementation and

maintenance of the operational risk framework,

tools and methodologies.

Responsible for oversight and challenge on the

adequacy of the risk and control processes

operating in the business.

Responsible for providing independent

assurance on the design, adequacy and

effectiveness of the Group’s system of internal

controls.

The Group’s Operational Risk Policy Standards (ORPS) are incorporated

in the GPF. They provide the direction for delivering effective operational

risk management and are designed to enable the consistent identification,

assessment, management, monitoring and reporting of operational risk

across the Group.

The three lines of defence model and the ORPS apply throughout the

Group and are implemented taking into account the nature and scale of

the underlying business. The following key operational risk management

techniques are included in the ORPS;

xRisk and control assessments: business units identify and assess

operational risks to ensure that they are effectively managed,

prioritised, documented and aligned to risk appetite;

xScenario analysis: scenarios for operational risk are used to assess

the possible impact of extreme but plausible operational risk loss

events. Scenario assessments provide a forward looking basis for

managing exposures that are beyond the Group’s risk appetite;

xLoss data management: each business unit’s internal loss data

management process captures all operational risk loss events above

certain minimum thresholds. The data is used to enhance the

adequacy and effectiveness of controls, identify opportunities to

prevent or reduce the impact of recurrence, identify emerging

themes, enable formal loss event reporting and inform risk and

control assessments and scenario analysis. Escalation of individual

events to senior management is determined by the seriousness of

the event. Operational loss events are categorised under the

following headings:

- clients, products and business practices;

- technology and infrastructure failures;

- employment practices and workplace safety;

- internal fraud;

- external fraud;

- execution, delivery and process management;

- malicious damage; and

- disaster and public safety.

xNew product approval process: this process ensures that all new

products or significant variations to existing products are subject to a

comprehensive risk assessment. Products are evaluated and

approved by specialist areas and are subject to executive approval

prior to launch; and

xSelf certification process: this requires management to monitor and

report regularly on the internal control framework for which they are

responsible, confirming its adequacy and effectiveness. This

includes certifying compliance with the requirements of Group

policies.

Each business unit must manage its operational risk exposure within an

acceptable level, testing the adequacy and effectiveness of controls and

other risk mitigants (for example, insurance) regularly and documenting

the results. Where unacceptable control weaknesses are identified,

action plans must be produced and tracked to completion. The Group

purchases insurance to provide the business with financial protection

against specific losses and to comply with statutory or contractual

requirements. Insurance is used as a risk mitigation tool in controlling the

Group’s exposures providing protection against financial loss once a risk

has crystallised.

*unaudited

RBS Group 2010200

Business review continued