RBS 2010 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

The development of the RBS and NatWest Customer Charters aims to

deliver those elements that customers have said are most important to

them, and has been well received by both customers and staff. The

division is reaping continuing benefits from investment in process

improvements and automation, resulting in gains in both service quality

and cost efficiency.

Serving our customers better is a key priority for RBS. While our

customer satisfaction compares well with our competitors we know we

can do more. In June 2010 we launched a Customer Charter setting out

14 commitments to delivering helpful banking.

The Customer Charter reflects the views and expectations of more than

30,000 customers. We are working hard to deliver on the commitments

we have made. This won't happen overnight but the Customer Charter is

our pledge that we will be regularly held to account against the progress

we make. As part of this we will publish an independently-assured report

on our performance every six months.

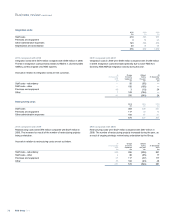

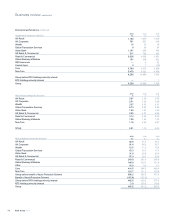

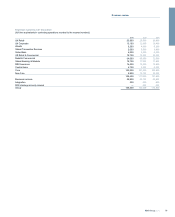

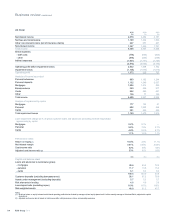

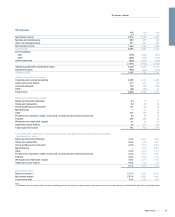

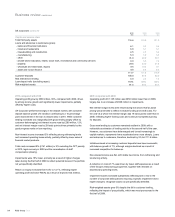

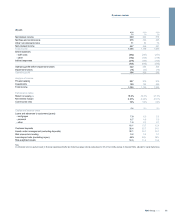

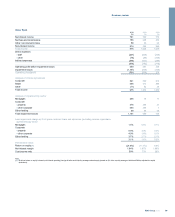

2010 compared with 2009

Operating profit recovered strongly from the low levels recorded in 2008

and 2009 to £1,372 million. Profit before impairments was up £624 million

or 33% and impairments fell by £519 million as the economic

environment continued to recover.

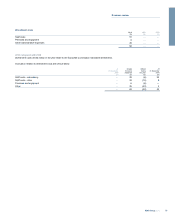

The division has continued to focus in 2010 on growing secured lending

while at the same time building customer deposits, thereby reducing the

Group’s reliance on wholesale funding. Loans and advances to

customers grew 5%, with a change in mix from unsecured to secured as

the Group actively sought to improve its risk profile. Mortgage balances

grew by 9% while unsecured lending contracted by 10%.

xMortgage growth was due to good retention of existing customers

and new business, the majority of which comes from the existing

customer base. Gross mortgage lending market share remained

broadly in line with 2009 at 12%, with the Group on track to meet its

Government target on net mortgage lending.

xCustomer deposits grew 10% on 2009, reflecting the strength of the

UK Retail customer franchise, which outperformed the market in an

increasingly competitive environment. Savings balances grew by £8

billion or 13% with 1.8 million accounts opened, outperforming the

market total deposit growth of 3%. Personal current account

balances increased by 3% on 2009.

Net interest income increased significantly by 18% to £4,078 million,

driven by strong balance sheet growth and repricing. Net interest margin

improved by 32 basis points to 3.91%, with widening asset margins

partially offset by contracting liability margins in the face of a competitive

deposit market.

Non-interest income declined 11% to £1,327 million, principally reflecting

the restructuring of current account overdraft fees in the final quarter of

2009.

Expenses decreased by 5%, with the cost:income ratio (net of insurance

claims) improving from 61% to 53%.

xDirect staff costs declined by 8%, largely driven by a clear

management focus on process re-engineering enabling a 7%

reduction in headcount.

xRBS continues to progress towards a more convenient, lower cost

operating model, with over 4.8 million active users of online banking

and a record share of new sales achieved through direct channels.

More than 7.8 million accounts have switched to paperless

statements and 276 branches now utilise automated cash deposit

machines.

Impairment losses decreased 31% to £1,160 million primarily reflecting

the recovery in the economic environment.

xThe mortgage impairment charge was £177 million (2009 - £124

million) on a total book of £91 billion. Mortgage arrears rates

marginally increased in 2010 but remain below the industry average,

as reported by the Council of Mortgage Lenders. Repossessions

showed only a small increase on 2009, as the Group continues to

support customers facing financial difficulties.

xThe unsecured lending impairment charge was £983 million (2009 -

£1,555 million) on a total book of £18 billion.

Risk-weighted assets decreased by 5% to £48.8 billion, with lower

unsecured lending, improving portfolio credit metrics and small

procyclicality benefits more than offsetting growth in mortgages.

81RBS Group 2010

Business review