RBS 2010 Annual Report Download - page 370

Download and view the complete annual report

Please find page 370 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

368 -

369

369 -

370

370 -

371

371 -

372

372 -

373

373 -

374

374 -

375

375 -

376

376 -

377

377 -

378

378 -

379

379 -

380

380 -

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

34 Memorandum items continued

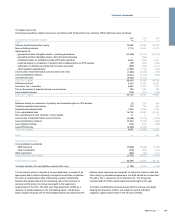

Bank levy

In his 22 June 2010 budget statement, the Chancellor announced that the

UK Government will introduce an annual bank levy. The Finance Bill

2011 contains details of how the levy will be calculated and collected.

The levy will be collected through the existing quarterly Corporation Tax

collection mechanism starting with payment dates on or after the date the

Finance Bill 2011 receives Royal Assent.

The levy will be based upon the total chargeable equity and liabilities as

reported in the balance sheet at the end of a chargeable period. In

determining the chargeable equity and liabilities the following amounts

are excluded: Tier 1 capital; certain “protected deposits” (for example

those protected under the Financial Services Compensation Scheme);

liabilities that arise from certain insurance business within banking groups;

liabilities in respect of currency notes in circulation; Financial Services

Compensation Scheme liabilities; liabilities representing segregated client

money; and deferred tax liabilities, current tax liabilities, liabilities in

respect of the levy, revaluation of property liabilities, liabilities

representing the revaluation of business premises and defined benefit

retirement liabilities. It will also be permitted in specified circumstances to

reduce certain liabilities by: netting against them certain assets; offsetting

assets on the relevant balance sheets that would qualify as high quality

liquid assets (in accordance with the FSA definition); and repo liabilities

secured against sovereign and supranational debt.

The levy will be set at a rate of 0.075 per cent from 2011. Three different

rates apply during 2011, these average to 0.075 per cent. Certain

liabilities will be subject to only a half rate, namely: any deposits not

otherwise excluded (except for those from financial institutions and

financial traders); and liabilities with a maturity greater than one year at

the balance sheet date. The levy will not be charged on the first £20

billion of chargeable liabilities.

If the levy had been applied to the balance sheet at 31 December 2010,

the cost of the levy to RBS Group would be in the region of £350 million

to £400 million in 2011.

Litigation

As a participant in the financial services industry,RBS Group operates in

alegal and regulatory environment that exposes it to potentially

significant litigation risks. As a result, the company and other members of

RBS Group are involved in various disputes and legal proceedings in the

United Kingdom, the United States and other jurisdictions, including

litigation. Such cases are subject to many uncertainties, and their

outcome is often difficult to predict, particularly in the earlier stages of a

case.

Other than as set out in this section “Litigation”, so far as RBS Group is

aware, no member of RBS Group is or has been engaged in or has

pending or threatened any governmental, legal or arbitration proceedings

which may have or have had in the recent past (covering the 12 months

immediately preceding the date of this document) a significant effect on

RBS Group’s financial position or profitability.

Unarranged overdraft charges

In the US, Citizens Financial Group, in common with other US banks, has

been named as a defendant in a class action asserting that Citizens

charges excessive overdraft fees. The plaintiffs claim that overdraft fees

resulting from point of sale and automated teller machine (ATM)

transactions violate the duty of good faith implied in Citizens’ customer

account agreement and constitute an unfair trade practice. RBS Group

considers that it has substantial and credible legal and factual defences

to these claims and will defend them vigorously. RBS Group is unable

reliably to estimate the liability, if any, that might arise or its effect on RBS

Group’s consolidated net assets, operating results or cash flows in any

particular period.

Shareholder litigation

RBS Group and a number of its subsidiaries and certain individual

officers and directors have been named as defendants in a class action

filed in the United States District Court for the Southern District of New

York. The consolidated amended complaint alleges certain false and

misleading statements and omissions in public filings and other

communications during the period 1 March 2007 to 19 January 2009, and

variously asserts claims under Sections 11, 12 and 15 of the US

Securities Act of 1933, Sections 10 and 20 of the US Securities

Exchange Act of 1934 (“Exchange Act”) and Rule 10b-5 thereunder.

The putative class is composed of (1) all persons who purchased or

otherwise acquired RBS Group ordinary securities and US American

depositary receipts (ADRs) between 1 March 2007 and 19 January 2009;

and/or (2) all persons who purchased or otherwise acquired RBS Group

Series Q, R, S, T and/or U non-cumulative dollar preference shares

issued pursuant or traceable to the 8 April 2005 US Securities and

Exchange Commission (SEC) registration statement and were damaged

thereby. Plaintiffs seek unquantified damages on behalf of the putative

class.

On 11 January 2011, the District Court dismissed all claims except those

based on the purchase of RBS Group Series Q, R, S, T, and/or U non-

cumulative dollar preference shares. The Court has not yet considered

potential grounds for dismissal of the remaining claims, and directed RBS

Group to re-file its motion to dismiss those claims within 45 days of its

ruling. On 28 January 2011, a new complaint was filed asserting claims

under Sections 10 and 20 of the Exchange Act on behalf of a putative

class of purchasers of ADRs.

RBS Group has also received notification of similar prospective claims in

the United Kingdom and elsewhere but no court proceedings have been

commenced in relation to these claims.

RBS Group considers that it has substantial and credible legal and

factual defences to the remaining and prospective claims and will defend

them vigorously. RBS Group is unable to reliably estimate the liability, if

any, that might arise or its effect on RBS Group’s consolidated net assets,

operating results or cash flows in any particular period.

RBS Group 2010368

Notes on the accounts continued