RBS 2010 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

RBS Insurance continued

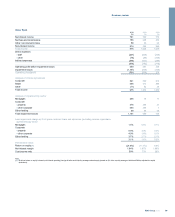

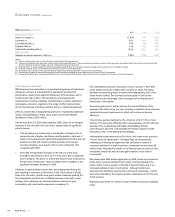

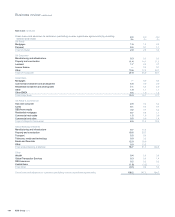

2010 2009 2008

Performance ratios

Return on equity (3) (7.9%) 1.7% 18.3%

Loss ratio (4) 92% 84% 70%

Commission ratio (5) 10% 9% 10%

Expense ratio (6) 13% 14% 14%

Combined operating ratio (7) 115% 106% 94%

Balance sheet

General insurance reserves - total (£m) 7,559 7,030 6,673

Notes:

(1) Other is predominantly made up of the discontinued personal lines broker business.

(2) Total in-force policies include travel and creditor policies sold through RBS Group. These comprise travel policies included in bank accounts e.g. Royalties Gold Account, and creditor policies sold

with bank products including mortgage, loan and card repayment payment protection.

(3) Divisional return on equity is based on divisional operating (loss)/profit after tax, divided by divisional average notional equity (based on regulatory capital).

(4) Loss ratio is based on net claims divided by net premium income for the UK businesses.

(5) Commission ratio is based on fees and commissions divided by gross written premium income for the UK businesses.

(6) Expense ratio is based on expenses (excluding fees and commissions) divided by gross written premium income for the UK businesses.

(7) Combined operating ratio is expenses (including fees and commissions) divided by gross written premium income, added to the loss ratio, for the UK businesses.

2010 compared with 2009

RBS Insurance has embarked on a significant programme of investment

designed to achieve a substantial lift in operational and financial

performance, ahead of the planned divestment of the business, with a

current target date of 2012. This programme encompasses the

enhancement of pricing capability, transformation of claims operations

and expense reduction, together with a range of other improvements

across the business, including a greater focus on capital management.

2010 as a whole was a disappointing profit year, impacted by significant

reserve strengthening for bodily injury claims and severe weather,

resulting in a loss of £295 million.

Income was down 2% (£63 million) against 2009, driven by a managed

reduction in the risk of the UK motor book, largely offset by significant

price increases:

xThis de-risking was achieved by a combination of rating action to

reduce the mix of higher-risk drivers, and the partial or total exit of

higher risk business lines (significantly scaling back the fleet and taxi

business and the exit of personal lines business sold through

insurance brokers). As a result in-force motor policies fell 14%

compared with 2009.

xEven with the significant reduction in the risk mix of the book,

average motor premiums were up 7% in the year, due to significant

price increases. The prices of like-for-like policies have increased by

35-40% over the last year. These increases were in addition to the

significant increases achieved in 2009.

Initiatives to grow ancillary income were also implemented during the

year resulting in revenues of £46 million in 2010 (£25 million in 2009).

Away from UK motor, overall home gross written premiums grew by 2%.

This included the exit from less profitable business in line with overall

strategy. Our underlying own brands business continues to grow

successfully, with gross written premiums increasing 4%.

The International business continued to invest in growth in 2010 with

gross written premiums of £425 million up 20% on 2009. The Italian

business successfully grew to a market share approaching 30% of the

direct insurer market. The German business grew 7% and is well

positioned to take advantage of the emerging shift to direct/internet

distribution in that market.

Several programmes to further improve the overall efficiency of the

business took effect during the year, including a reduction of six sites and

operational process improvements, which will continue to improve

efficiency.

Total in-force policies declined by 3%, driven by a fall of 14% in motor

policies. This was partly offset by higher travel policies, up 64% with new

business from a partnership with Nationwide Building Society

commencing in Q4 2010. The personal lines broker segment overall

declined by 43%, in line with business strategy.

Underwriting income declined by £63 million, with lower motor premium

income, driven by rating action. Increased fees and commissions

reflected profit sharing arrangements with UK Retail in relation to

insurance distribution to bank customers. Investment income was £28

million lower, reflecting the impact of low interest rates on returns on the

investment portfolio as well as lower gains realised on the sale of

investments.

Net claims were £326 million higher than in 2009, driven by increases to

bodily injury reserves relating to prior years, including allowance for

higher claims costs in respect of Periodic Payment Orders due to an

increased settlement rate of such claims. Although bodily injury

frequency has stabilised, severity has continued to deteriorate. Claims

were also impacted by the adverse weather experienced in the first and

fourth quarters.

Expenses were down 7%, driven by lower industry levies and marketing

costs.

RBS Group 201098

Business review continued