RBS 2010 Annual Report Download - page 285

Download and view the complete annual report

Please find page 285 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

25. Share-based payments

The Group awards shares and options over shares in The Royal Bank of

Scotland Group plc to its employees. The expense for these transactions

is measured based on the fair value on the date the awards are granted.

The fair value of an option is estimated using valuation techniques which

take into account its exercise price, its term, the risk-free interest rate and

the expected volatility of the market price of The Royal Bank of Scotland

Group plc's shares. Vesting conditions are not taken into account when

measuring fair value, but are reflected by adjusting the proportion of

awards that actually vest. The fair value is expensed on a straight-line

basis over the vesting period. Following an amendment to IFRS 2 for

accounting periods starting after 1 January 2009, the cancellation of an

award with non-vesting conditions triggers immediate recognition of an

expense in respect of any unrecognised element of the fair value of the

award.

26. Cash and cash equivalents

Cash and cash equivalents comprises cash and demand deposits with

banks together with short-term highly liquid investments that are readily

convertible to known amounts of cash and subject to insignificant risk of

change in value.

27. Shares in Group entities

The company's investments in its subsidiaries are stated at cost less any

impairment.

Critical accounting policies and key sources of estimation

uncertainty

The reported results of the Group are sensitive to the accounting policies,

assumptions and estimates that underlie the preparation of its financial

statements. UK company law and IFRS require the directors, in preparing

the Group's financial statements, to select suitable accounting policies,

apply them consistently and make judgements and estimates that are

reasonable and prudent. In the absence of an applicable standard or

interpretation, IAS 8 ‘Accounting Policies, Changes in Accounting

Estimates and Errors’, requires management to develop and apply an

accounting policy that results in relevant and reliable information in the

light of the requirements and guidance in IFRS dealing with similar and

related issues and the IASB's ‘Framework for the Preparation and

Presentation of Financial Statements’. The judgements and assumptions

involved in the Group's accounting policies that are considered by the

Board to be the most important to the portrayal of its financial condition

are discussed below. The use of estimates, assumptions or models that

differ from those adopted by the Group would affect its reported results.

Loan impairment provisions

The Group's loan impairment provisions are established to recognise

incurred impairment losses in its portfolio of loans classified as loans and

receivables and carried at amortised cost. A loan is impaired when there

is objective evidence that events since the loan was granted have

affected expected cash flows from the loan. Such objective evidence,

indicative that a borrower’s financial condition has deteriorated, can

include for loans that are individually assessed: the non-payment of

interest or principal; debt restructuring; probable bankruptcy or liquidation;

significant reduction in the value of any security; breach of limits or

covenants; and deteriorating trading performance and, for collectively

assessed portfolios: the borrowers’ payment status and observable data

about relevant macroeconomic measures.

The impairment loss is the difference between the carrying value of the

loan and the present value of estimated future cash flows at the loan's

original effective interest rate.

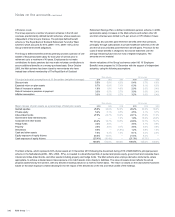

At 31 December 2010, gross loans and advances to customers totalled

£573,315 million (2009 - £745,519 million; 2008 - £885,611 million) and

customer loan impairment provisions amounted to £18,055 million (2009 -

£17,126 million; 2008 - £10,889 million).

There are two components to the Group's loan impairment provisions:

individual and collective.

Individual component - all impaired loans that exceed specific thresholds

are individually assessed for impairment. Individually assessed loans

principally comprise the Group's portfolio of commercial loans to medium

and large businesses. Impairment losses are recognised as the

difference between the carrying value of the loan and the discounted

value of management's best estimate of future cash repayments and

proceeds from any security held. These estimates take into account the

customer's debt capacity and financial flexibility; the level and quality of

its earnings; the amount and sources of cash flows; the industry in which

the counterparty operates; and the realisable value of any security held.

Estimating the quantum and timing of future recoveries involves

significant judgement. The size of receipts will depend on the future

performance of the borrower and the value of security, both of which will

be affected by future economic conditions; additionally, collateral may not

be readily marketable. The actual amount of future cash flows and the

date they are received may differ from these estimates and consequently

actual losses incurred may differ from those recognised in these financial

statements.

Collective component - this is made up of two elements: loan impairment

provisions for impaired loans that are below individual assessment

thresholds (collectively assessed provisions) and for loan losses that

have been incurred but have not been separately identified at the balance

sheet date (latent loss provisions). Collectively assessed provisions are

established on a portfolio basis using a present value methodology taking

into account the level of arrears, security, past loss experience, credit

scores and defaults based on portfolio trends. The most significant

factors in establishing these provisions are the expected loss rates and

the related average life. These portfolios include credit card receivables

and other personal advances including mortgages. The future credit

quality of these portfolios is subject to uncertainties that could cause

actual credit losses to differ materially from reported loan impairment

provisions. These uncertainties include the economic environment,

notably interest rates and their effect on customer spending, the

unemployment level, payment behaviour and bankruptcy trends. Latent

loss provisions are held against estimated impairment losses in the

performing portfolio that have yet to be identified as at the balance sheet

date. To assess the latent loss within its portfolios, the Group has

developed methodologies to estimate the time that an asset can remain

impaired within a performing portfolio before it is identified and reported

as such.

283RBS Group 2010

Financial statements