RBS 2010 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

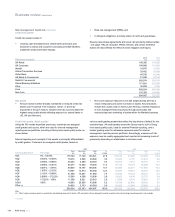

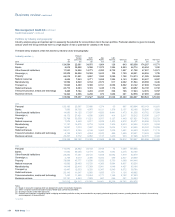

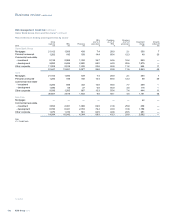

Retail credit assets: UK residential mortgages

Key points

xThe UK mortgage portfolio totalled £92.6 billion at 31 December

2010, an increase of 8% from 31 December 2009, due to continued

strong sales growth and lower redemption rates in historical terms.

Of the total portfolio, 98% is designated as Core business with the

primary brands being the Royal Bank of Scotland, NatWest, the One

Account and First Active (Non-Core is made up of Direct Line

Mortgages). The assets comprise prime mortgage lending and

include 6.8% (£6.2 billion) of exposure to residential buy-to-let at 31

December 2010. There is a small legacy self certification book

(0.3% of total assets); which was withdrawn from sale in 2004.

xGross new mortgage lending in 2010 was strong at £15.9 billion.

The average LTV for new business during 2010 was 64.2%

compared with 67.2% in 2009. The maximum LTV available to new

customers remains at 90%. Based on the Halifax House Price index

as at September 2010, the book averaged indexed LTV has reduced

to 58.2% at 31 December 2010 from 59.1% at 31 December 2009

influenced by favourable house price movements with the proportion

of balances in negative equity at 31 December 2010 standing at

6.9% down from 10.9% at 31 December 2009.

xThe arrears rate (more than 3 payments in arrears, excluding

repossessions and shortfalls post property sale) increased slightly to

1.7% at 31 December 2010 from 1.6% at 31 December 2009. After

aperiod of deterioration the arrears rate has stabilised and has

remained broadly stable since late 2009. The arrears rate on the

buy-to-let portfolio was 1.3 % at 31 December 2010 (2009 - 1.4%).

xThe mortgage impairment charge was £183 million for the year

ended 31 December 2010 compared to £129 million for 2009, with a

proportion of the 2010 charge (approximately £70 million) being the

result of adjustments reflecting reduced expectations of recovery on

prior period defaulted debt and refinement of provision methodology.

Underlying default trends improved throughout 2010 when

compared with 2009. Provisions as a percentage of loans and

receivables have increased to 0.37% at 31 December 2010

compared with 0.25% at 31 December 2009. Default and arrears

rates remain sensitive to economic developments and are currently

supported by the low interest rate environment and strong book

growth with recent business yet to mature.

xAnumber of initiatives aimed at supporting customers experiencing

temporary financial difficulties remain in place. Forbearance

activities include offering reduced or deferred payment terms on a

temporary basis for a period of up to 12 months during which arrears

continue to accrue on the account. Forbearance activities in the

performing book amounted to £0.6 billion during 2010. It is Group

policy not to initiate repossession proceedings for at least six

months after arrears are evident. The number of properties

repossessed in 2010 was 1,392 compared to 1,251 in 2009.

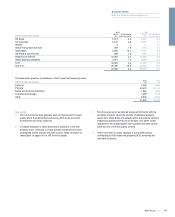

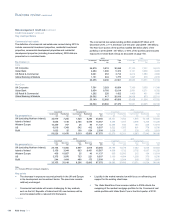

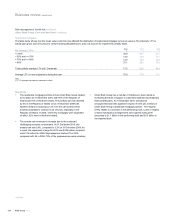

Citizens real estate

Key points

xCitizens total residential real estate portfolio totalled $38.2 billion at

31 December 2010 (2009 - $42.5 billion). The real estate portfolio

comprises $9.7 billion (Core: $8.6 billion; Non-Core: $1.1 billion) of

first lien residential mortgages and $28.5 billion (Core: $23.7 billion;

Non-Core: $4.8 billion) of home equity loans and lines (first and

second lien). Home Equity Core consists of 46% first lien position

while Non-Core consists of 97% second lien position. The Core

business comprises 84% of the portfolio and Non-Core comprising

16%, with the serviced by others (SBO) portfolio being the largest

component at 75% of the Non-Core portfolio.

xCitizens continue to focus primarily on the ‘footprint states’ of New

England, Mid-Atlantic and Mid-West targeting low risk products and

maintaining conservative risk policies. Loan acceptance criteria were

tightened during 2009 to address deteriorating economic and market

conditions. As at 31 December 2010, the portfolio consisted of $31.5

billion (82% of the total portfolio) in these footprint states.

xThe SBO portfolio is part of Non-Core and consists of purchased

pools of home equity loans and lines (96% second lien) with current

LTV (105%) and geographic profiles (73% outside of Citizens

footprint) leading to an annualised charge-off rate of 10.6% in 2010.

The SBO book has been closed to new purchases since the third

quarter of 2007 and is in run-off, with exposure down from $5.5

billion at 31 December 2009 to $4.5 billion at 31 December 2010.

The arrears rate of the SBO portfolio decreased from 3.1% at 31

December 2009 to 2.7% at 31 December 2010 due to more effective

account servicing and collections, following a service conversion in

2009.

xThe current weighted average LTV of the real estate portfolio

increased slightly from 74.5% at 31 December 2009 to 75.3% at 31

December 2010, driven by a down turn in home prices. The current

weighted average LTV of the real estate portfolio excluding SBO is

70.0%.

xThe arrears rate decreased slightly from 1.5% at 31 December 2009

to 1.4% at 31 December 2010. Delinquency rates have stabilised in

recent months for both residential mortgages and home equity loans

and lines. Citizens’ participates in the US Government Home

Affordable Modification Program (HAMP) alongside other bank

sponsored initiatives. Under HAMP, any borrower requesting a

modification must be first reviewed to see if they meet the criteria of

this programme. If the borrower does not qualify for HAMP, then

they are reviewed for internal modification programmes. The HAMP

programme is available only for first lien loans to owner-occupied.

All second lien home equity lines and loans are modified using

internal programmes.

xThe cumulative effect of these arrangements has helped the

Group’s customers. Modified loan balances were $566 million at 31

December 2010 (2009 - $235 million).

159RBS Group 2010

Business review

Risk and balance sheet management