RBS 2010 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Reputation risk*

Reputation risk is defined as the potential loss in reputation that could

lead to negative publicity, loss of revenue, costly litigation, a decline in

the customer base or the exit of key Group employees.

Reputation risk can arise from actions taken by the Group or a failure to

take action, such as failing to assess the environmental, social or ethical

impacts of clients or projects that the Group has provided products or

services to.

The Group seeks to safeguard its reputation by considering the impact on

the value of its franchise from how it conducts business, its choice of

customers and the way stakeholders view the Group. Managing the

Group’s reputation is the joint responsibility of all employees, and

reputational considerations should, as part of standard practice, be

integrated into the Group’s day-to-day decision making structures.

Currently the Group manages reputational risk through a number of

functions, such as divisions, Group Communications, Group

Sustainability and an Environmental, Social and Ethical (ESE) risk

management function. The latter function is responsible for assessing

ESE risks associated with business engagements and business divisions.

The Board has ultimate responsibility for managing any impact on the

reputation of the Group arising from its operations. The Group

Sustainability Committee (established at the beginning of 2010) sets the

overall strategy and approach for the management of Group sustainability,

however all parts of the Group take responsibility for reputation

management.

The risk is viewed as material given the central nature of the Group’s

market reputation in the strategic risk objectives.

Pension risk*

The Group is exposed to risk from its defined benefit pension schemes to

the extent that the assets of the schemes do not fully match the timing

and amount of the schemes’ liabilities. Pension scheme liabilities vary

with changes to long-term interest rates, inflation, pensionable salaries

and the longevity of scheme members as well as changes in legislation.

The Group is exposed to the risk that the market value of the schemes’

assets, together with future returns and any additional future contributions

could be considered insufficient to meet the liabilities as they fall due. In

such circumstances, the Group could be obliged, or may choose, to make

additional contributions to the schemes.

The RBS Group Pension Fund (“Main scheme”) is the largest of the

schemes and the main source of pension risk. The Main scheme

operates under a trust deed under which the corporate trustee, RBS

Pension Trustees Limited, is a wholly owned subsidiary of The Royal

Bank of Scotland plc and the trustee board comprises six directors

selected by the Group and four directors nominated by members.

The trustee is solely responsible for the investment of the schemes

assets which are held separately from the assets of the Group. The

Group and the trustee must agree on the investment principles and the

funding plan.

In October 2006, the Main scheme was closed to new employees. In

November 2009, the Group confirmed that it was making changes to the

Main scheme and a number of other defined benefit schemes including

the introduction of a limit of 2% per annum (or Consumer Price Indices

(CPI) inflation, if lower) to the amount of any salary increase that will

count for pensionable purposes.

Risk appetite and investment policy are agreed by the trustee with

quantitative and qualitative input from the scheme actuaries and

investment advisers. The trustee also consults with the Group to obtain

its view on the appropriate level of risk within the pension fund.

The Group maintains an independent review of risk within its pension

funds. The Group Risk Committee now monitors pension obligation risk

on an ongoing basis with a monthly report illustrating the funding

positions and key sensitivities of the Group’s pension schemes.

Additionally, as part of the Internal Capital Adequacy Assessment

Process (ICAAP) process, the change in asset and liability values is

modelled over a twelve-month time horizon under a stressed scenario.

The funding valuation of the Main scheme at 31 March 2010 is currently

in progress. Further details are given in Note 4 on the accounts.

The Main scheme, which represents 84% of plan assets at 31 December

2010, is invested in a diversified portfolio of quoted and private equity,

government and corporate fixed interest and index-linked bonds, and

other assets including property and hedge funds. The trustee has taken

measures to partially mitigate inflation and interest rate risks both by

investment in suitable physical assets and by entering into inflation and

interest rate swaps. The Main scheme has an additional exposure to

rewarded risk by investing in equity futures.

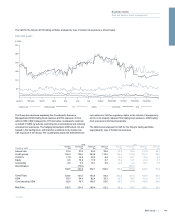

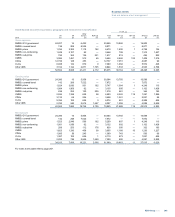

The table below shows the impact on the Main schemes assets and

liabilities (measured according to IAS 19 ‘Employee Benefits’) of changes

in interest rates and equity values at the year end, taking account of the

current asset allocation and hedging arrangements.

Change

in value

of assets

£m

Change

in value of

liabilities

£m

Decrease/

(increase) in net

pension

obligations

£m

As at 31 December 2010

Fall in nominal swap yields of 0.25% at all durations with no change in credit spreads 422 193 229

Fall in real swap yields of 0.25% at all durations with no change in credit spreads 355 799 (444)

Fall in credit spreads of 0.25% at all durations with no change in nominal or real swap yields 98 1,005 (907)

Fall in equity values of 10% (1,083) — (1,083)

203RBS Group 2010

Business review

Risk and balance sheet management