RBS 2010 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Regulatory developments

Basel III and CRD IV

The Basel Committee released the final text on the new Basel III Capital

and Liquidity Frameworks in December 2010, the contents of which were

broadly as expected. Whilst most of the new rules are ‘final’ there are

lengthy observation periods for the more novel elements (the liquidity

coverage ratio, the net stable funding ratio and the leverage ratio)

designed to identify any unintended consequences prior to full

implementation and it is possible that some of the detail may be amended.

The capital requirements for credit valuation adjustments (CVAs) with

respect to counterparty risk are subject to a final impact assessment

which is being carried out in the first quarter of 2011. The Committee’s

guidance on the countercyclical capital buffers allows for significant

judgement which will need to be clarified by national regulators. The

potential impacts for RBSG are set out below.

xnational implementation of increased capital requirements will begin

on 1 January 2013;

xthere will be a phased five year implementation of new deductions

and regulatory adjustments to Core Tier 1 capital commencing 1

January 2014;

xthe de-recognition of non-qualifying non common Tier 1 and Tier 2

capital instruments will be phased in over 10 years from 1 January

2013; and

xrequirements for changes to minimum capital ratios, including

conservation and countercyclical buffers, as well as additional

requirements for Systemically Important Financial Institutions, will be

phased in from 2013 to 2019.

The focus will now be on the EU’s implementation of the Basel framework.

The Commission’s legislative proposal - the Capital Requirements

Directive (CRD) IV - is expected to appear in summer 2011.

Contingent capital and loss absorbency

The Basel Committee issued its final rules on the requirements to ensure

all classes of capital instruments fully absorb losses at the point of non-

viability, before tax payers are exposed to loss. These are designed to

combat the experience during the crisis where holders of Tier 2 capital

instruments did not suffer any losses when banks were bailed out by the

public sector. Debate continues, meanwhile, over possible requirements

for bailing-in senior debt holders, as a further means of protecting the

taxpayer.

Implementation by the Group

RBS is advanced in its planning to implement these newmeasures and is

appropriately well-capitalised with tangible equity of £56 billion, Core Tier

1capital of £49 billion and a Core Tier 1 ratio of 10.7% at 31 December

2010.

Set out below are indicative impacts and timings of the major Basel 2.5

and Basel III proposals on the Group’s Core Tier 1 ratio. The estimates

are still subject to change; a high degree of uncertainty still remains

around implementation details as the guidelines are not fully finalised and

must still be converted into rules by the FSA.

Asubstantial part of the mitigating impacts mentioned in the following

paragraphs relate to run-off in the normal course of business and de-

leveraging of legacy positions and securitisations, including Non-Core.

The Group is also devoting considerable resource to enhancing its

models to improve management of market and counterparty exposures.

Akey mitigating action related to counterparty risk involves enhancement

to internal models, which is a significant undertaking. There could be

various hedging strategies and business decisions taken as part of

mitigation which may have an adverse, but manageable, impact on

revenues.

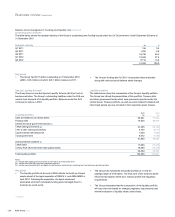

CRD3 (Basel 2.5): Published rules for market risk and re-securitisations.

Proposed implementation date 31 December 2011

The estimated impact on pro-forma at the end of 2011 on RWAs post

mitigation is an increase of £25 billion to £30 billion, split equally between

GBM and Non-Core.

Basel III Counterparty risk: Proposed implementation date 1 January

2013

The impact on RWAs on implementation in 2013 is currently estimated at

£45 to £50 billion post mitigation and deleveraging, although there may

still be movement in the final framework around this risk.

Basel III Securitisations: Proposed implementation date 1 January 2013

Under the proposals, current deductions under Basel II (50% Core Tier 1,

50% Tier 2) for securitisation positions are switched to RWAs weighted at

1,250%. Post the run-off of securitisation positions and mitigating actions,

the impact on implementation in 2013, on RWAs is estimated to be an

increase of £30 billion to £35 billion with a corresponding reduction in

deductions from Core Tier 1 and Tier 2 capital of £1.2 billion to £1.5

billion each. The impact net RWA equivalent of this change assuming a

10% Core Tier 1 ratio would be an increase in net RWA equivalents of

£18 billion to £20 billion.

Summary impacts

The extent of the individual areas of impact, as set out above, may

continue to change over time. As previously indicated, however, the

overall impact on RWAs of CRD III and CRD IV after mitigation and

deleveraging is estimated to be £100 billion to £115 billion, before

allowing for the offsetting reduction in deductions.

The impact referenced above would lower the Core Tier 1 ratio by

approximately 1.3%, assuming RWAs of £600 billion and a Core Tier 1

ratio of 10%.

131RBS Group 2010

Business review

Risk and balance sheet management