RBS 2010 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

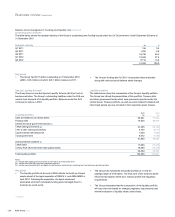

Structure of prudential regulation in the UK

Following the consultation by HM Treasury on ‘A new approach to

financial regulation’ in 2010, the government subsequently published

further detailed proposals to give the Bank of England responsibility for

prudential regulation, and to create a new Consumer Protection and

Markets Authority to protect the interests of bank customers.

Increase in the level of customer protection under Financial Services

Compensation Scheme

The European Commission has introduced a uniform compensation level

of €100,000 across Member States from 1 January 2011. The sterling

equivalent was confirmed by HM Treasury as £85,000.

Independent Commission on Banking

The Independent Commission on Banking has published responses from

banks, academics and other interested parties to its initial consultation.

In its summary of the evidence received the Commission noted that there

was considerable interest, both positive and negative, in the question of

splitting retail and investment banks. The Commission plans to publish its

interim report in April.

FSA Code on remuneration

In July 2009 the European Commission adopted a proposal to further

amend the Capital Requirements Directive (CRD) which included

proposals on remuneration policies. This was subsequently voted for and

approved (CRD III).

CRD III required the Commission of European Banking Supervisors

(CEBS) to issue guidelines on sound remuneration policies which comply

with its principles and these were issued on 10 December 2010 (the

“Guidelines”).

The FSA amended its Remuneration Code to take into account the

Guidelines and published its policy statement on remuneration on 17

December 2010.

The Group is required to be compliant with the FSA Remuneration Code

with effect from 1 January 2011:

xas a “Tier 1” organisation, the Code applies to all employees on a

global basis;

xthere are specific remuneration and governance requirements in

relation to “Code Staff”; and

xfollowing an ongoing review of our remuneration arrangements and

discussions with the FSA, 2011 RBS remuneration arrangements

are fully compliant with the FSA Remuneration Code.

Bank levy

In his 22 June 2010 budget statement, the Chancellor announced that the

UK Government will introduce an annual bank levy. The Finance Bill

2011 contains details of how the levy will be calculated and collected.

The levy will be collected through the existing quarterly corporation tax

collection mechanism starting with payment dates on or after the date the

Finance Bill 2011 receives Royal Assent. Further information is included

on page 368.

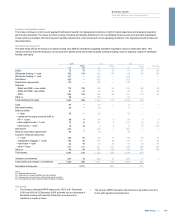

Stress and scenario testing

Stress testing forms part of the Group’s risk and capital framework and is

an integral component of Basel II. As a key risk management tool, stress

testing highlights to senior management potential adverse unexpected

outcomes related to a mixture of risks and provides an indication of how

much capital might be required to absorb losses, should adverse

scenarios occur. Stress testing is used at both a divisional and Group

level to assess risk concentrations, estimate the impact of stressed

earnings, impairments and write-downs on capital. It determines the

overall capital adequacy under a variety of adverse scenarios. The

principal business benefits of the stress testing framework include:

understanding the impact of recessionary scenarios; assessing material

risk concentrations; and forecasting the impact of market stress and

scenarios on the Group’s balance sheet liquidity.

Aseries of stress events are monitored on a regular basis to assess the

potential impact of an extreme yet plausible event on the Group. There

are four core elements of scenario stress testing:

xmacroeconomic stress testing considers the impact on both

earnings and capital for a range of scenarios. They entail multi-year

systemic shocks to assess the Group’s ability to meet its capital

requirements and liabilities as they fall due in a downturn in the

business cycle and/or macroeconomic environment;

xenterprise-wide stress testing considers scenarios that are not

macroeconomic in nature but are sufficiently broad to impact across

multiple risks or divisions and are likely to affect earnings, capital

and funding;

xcross-divisional stress testing includes scenarios which have

impacts across divisions relating to sensitivity to a common risk

factor(s). This would include, for example, sector based stress

testing across corporate portfolios and sensitivity analysis to stress

in market factors. These stress tests are discussed with senior

divisional management and are reported to senior committees

across the Group; and

xdivisional and risk specific stress testing is undertaken to support

risk identification and management. Examples include the daily

product based stress testing using a hybrid of hypothetical and

historical scenarios within market risk.

Portfolio analysis, using historic performance and forward looking

indicators of change, uses stress testing to facilitate the measurement of

potential exposure to events and seeks to quantify the impact of an

adverse change in factors which drive the performance and profitability of

aportfolio.

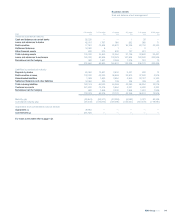

133RBS Group 2010

Business review

Risk and balance sheet management