RBS 2010 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

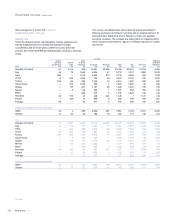

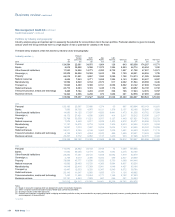

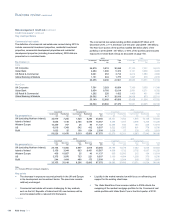

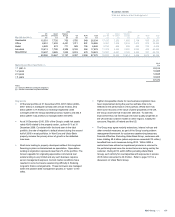

Key points

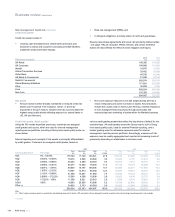

xCredit risk assets relating to most of the countries above declined in

2010, reflecting active exposure management. In addition to the

overall exposure reductions, granular portfolio reviews have been

and continue to be undertaken with a view to adjusting the tenor

profile and better alignment of the Group’s country risk appetite to

the risk of adverse economic and political developments.

xReductions were seen in corporate and personal exposures,

particularly in the Non-Core portfolios. This contrasted with

increases in financial institutions in a number of countries, mostly

due to increases in RRM exposure. Some countries in Asia have

seen increased exposures during 2010, including two of the Group’s

strategically important countries in this region, China and India,

following reductions in 2008 and 2009.

xThe Group broadened its country risk framework in 2010, to capture

advanced as well as emerging market countries. Cross-country

assessments were conducted to identify portfolio vulnerabilities to a

number of risk scenarios, including a eurozone sovereign debt crisis.

Limit controls are being applied on a risk differentiated basis and

selected exposure actions have been taken. Further scenario stress

testing is continuing, and covers the potential for economic and

political shocks in the eurozone and in the broader global

environment.

xFor selected eurozone countries, the general trend in lending was

lower, due in part to a depreciation of the euro against sterling by

3% over the year.

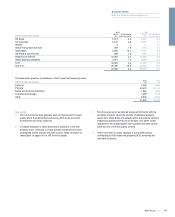

xRepublic of Ireland (ROI): lending fell by £4.3 billion in 2010,

resulting from reductions in personal lending by £2.1 billion, central

banks and other financial institutions by £0.5 billion and corporate

clients by £1.6 billion. An increase was seen in Ulster Bank’s central

bank exposure due to higher cash balances as part of its liquidity

portfolio. The general trend in exposure remains downward.

Divisional analysis is set out below:

xUlster Bank represents more than 95% (£32 billion) of the

Group’s Core lending to ROI and has seen a minimal increase

of £0.64 billion in 2010, largely because of a rise of £0.3 billion

in central bank placing due to increased cash holdings. Ulster

Bank Core provisions at 31 December 2010 increased by 70%

due to the continuing deterioration in the Irish economy.

xNon-Core lending to ROI (£10.8 billion) declined by £4.2 billion

in 2010, mainly due to a reduction in exposure to corporate and

financial institutions of £3 billion during the year. In addition,

customer advances in Lombard Ireland decreased by 30%

during the year to £0.9 billion. Overall default levels have

continued to show signs of stabilisation.

xGlobal Banking & Markets (GBM) accounts for a further £0.6

billion of the Core lending exposure, largely relating to domestic

and foreign owned financial institutions. In addition, overall

limits to the major Irish domestic banks have halved since 31

December 2008 to £1.2 billion, with the majority representing

collateralised RRM or guarantees for third-party obligations.

Overall credit quality remains acceptable with a majority of the

exposure to investment grade entities.

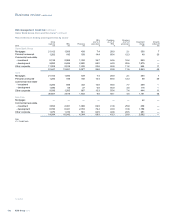

xSpain: lending fell by £0.9 billion, due to a reduction in corporate

activity. During the fourth quarter, this reduction accelerated. Non-

Core represents 59% of the Group’s total exposure to Spain in 2010

(2009 - 65%). In the course of 2010, progress was made towards

increased collateralisation of the portfolio.

xItaly: lending decreased by £1.7 billion, as a result of a net reduction

in corporate lending of £2.0 billion and an increase to financial

institutions of £0.3 billion. In addition, there was an increase in RRM

exposure to financial institutions by £0.7 billion; the non-lending

portfolio is comprised predominantly of collateralised trading activity.

xPortugal: lending decreased slightly by £0.1 billion related to

reductions in corporate activity. Non-Core represents 41% of the

total exposure; the structure of the exposure was enhanced through

ashift to short-term and collateralised products to support the

hedging needs of customers.

xGreece: lending fell by £0.1 billion, due to a reduction in corporate

activity. Continuous close scrutiny of the portfolio throughout the

year and divestment of selected assets have improved the overall

quality of the portfolio, available-for-sale (AFS) debt securities

represent the primary concentration.

xTotal exposure to Egypt was £253 million at 31 December 2010,

including lending of £124 million. The Group has minimal exposures

to North African countries.

153RBS Group 2010

Business review

Risk and balance sheet management