RBS 2010 Annual Report Download - page 339

Download and view the complete annual report

Please find page 339 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

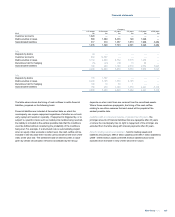

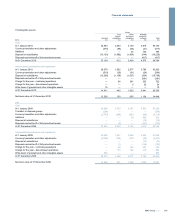

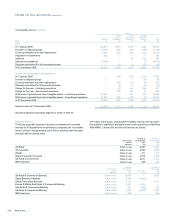

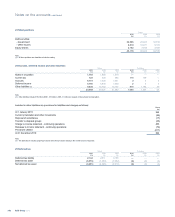

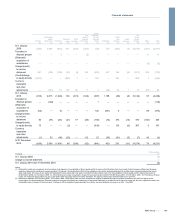

Impairment testing involves the comparison of the carrying value of a

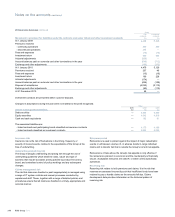

CGU or group of CGUs with its recoverable amount. The recoverable

amount is the higher of the unit's fair value and its value in use. Value in

use is the present value of expected future cash flows from the CGU or

group of CGUs. Fair value is the amount obtainable for the sale of the

CGU in an arm's length transaction between knowledgeable, willing

parties.

Impairment testing inherently involves a number of judgmental areas: the

preparation of cash flow forecasts for periods that are beyond the normal

requirements of management reporting; the assessment of the discount

rate appropriate to the business; estimation of the fair value of CGUs;

and the valuation of the separable assets of each business whose

goodwill is being reviewed. Sensitivity to the variables more significant to

each assessment are presented below.

The recoverable amounts for all CGUs at 30 September 2010 were

based on the value in use test, using management's latest five-year

forecasts. The long-term growth rates have been based on respective

country GDP rates adjusted for inflation. The risk discount rates are

based on observable market long-term government bond yields and

average industry betas adjusted for an appropriate risk premium based

on independent analysis.

The recoverable amount of UK Retail, based on a 3% (2009 - 4%)

terminal growth rate and 15.7% (2009 - 14.6%) pre tax discount rate,

exceeded the carrying amount by £6.9 billion (2009 - £0.7 billion). A 1%

change in the discount rate or the terminal growth rate would change the

recoverable amount by approximately £1.5 billion (2009 - £0.9 billion) and

£0.9 billion (2009 - £0.5 billion) respectively. In addition, a 5% change in

the forecast pre tax earnings would change the recoverable amount by

approximately £0.9 billion (2009 - £0.4 billion).

The recoverable amount of UK Corporate, based on 3% (2009 - 4%)

terminal growth rate and a 15.6% (2009 - 15.1%) pre tax discount rate,

exceeded its carrying value by £5.3 billion (2009 - £6.1 billion). A 1%

change in the discount rate or the terminal growth rate would change the

recoverable amount by approximately £1.6 billion (2009 - £1.4 billion) and

£0.9 billion (2009 - £0.9 billion) respectively. In addition, a 5% change in

the forecast pre tax earnings would change the recoverable amount by

approximately £1.0 billion (2009 - £0.8 billion).

The recoverable amount of Wealth, based on a 3% (2009 - 4%) terminal

growth rate and a 12.0% (2009 - 15.3%) pre tax discount rate, exceeded

its carrying value by more than 100% and was insensitive to a reasonably

possible change in key assumptions.

The recoverable amount of Global Transaction Services, based on a 3%

(2009 - 3%) terminal growth rate and a 12.8% (2009 - 16.7%) pre tax

discount rate, exceeded its carrying value by more than 100% (2009 -

100%) and was insensitive to a reasonably possible change in key

assumptions.

The recoverable amount of US Retail & Commercial, based on a 5%

(2009 - 5%) terminal growth rate and a 14.9% (2009 - 14.8%) pre tax

discount rate, exceeded its carrying value by £1.6 billion (2009 - £2.1

billion). A 1% change in the discount rate or the terminal growth rate

would change the recoverable amount by approximately £1.6 billion

(2009 - £1.0 billion) and £0.8 billion (2009 - £0.8 billion) respectively. In

addition, a 5% change in the forecast pre tax earnings would change the

recoverable amount by approximately £0.7 billion (2009 - £0.7 billion).

The recoverable amount of RBS Insurance, based on a 3% (2009 - 3%)

terminal growth rate and a 13.1% (2009 - 13.9%) pre tax discount rate,

exceeded the carrying amount by over £2.4 billion (2009 - £3.0 billion)

and was insensitive to a reasonably possible change in key assumptions.

In 2008, the recoverable amounts for all CGUs were based on value in

use tests. Goodwill write downs were recorded in Global Banking &

Markets, US Retail & Commercial, Europe & Middle East Retail &

Commercial Banking and Asia Retail & Commercial Banking divisions. In

addition, an impairment charge of £14.5 billion was recorded in respect of

goodwill attributable to the State of Netherlands minority interest arising

on the acquisition of ABN AMRO.

337RBS Group 2010

Financial statements