RBS 2010 Annual Report Download - page 162

Download and view the complete annual report

Please find page 162 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Risk management: Credit risk continued

Credit risk assets* continued

Key credit portfolios continued

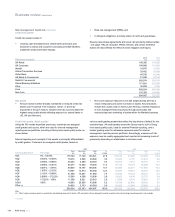

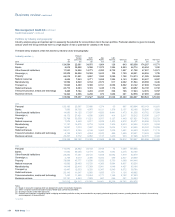

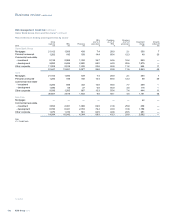

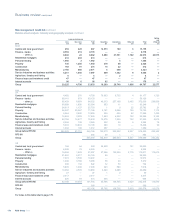

Retail credit assets: Personal lending

The Group's personal lending portfolio includes credit cards, unsecured loans, auto finance and overdrafts. The majority of personal lending exposures

exist in the UK and the US. New defaults as a proportion of average loans and receivables are shown in the following table.

2010 2009 2008

Personal lending

Average

loans and

receivables

£m

Impairment

charge

as a % o

f

loans and

receivables

%

Average

loans and

receivables

£m

Impairment

charge

as a % o

f

loans and

receivables

%

Average

loans and

receivables

£m

Impairment

charge

as a % o

f

loans and

receivables

%

UK Retail cards (1) 6,025 5.0 6,101 8.7 6,617 6.4

UK Retail loans (1) 9,863 4.8 12,062 5.9 13,545 3.3

$m % $m % $m %

Citizens cards (2,3) 1,555 9.9 1,772 9.7 2,275 4.9

Citizens auto loans (2) 8,133 0.6 9,759 1.2 11,386 1.1

Notes:

(1) The ratio for UK Retail assets refers to the impairment charges for the year.

(2) The ratio for Citizens refers to charge-offs in the year, net of recoveries realised in the year.

(3) The 2009 data have been revised to exclude the Kroger Personal Finance portfolio, which was sold in 2010.

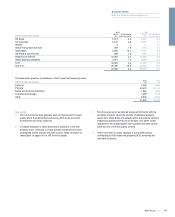

Key points

xThe UK personal lending portfolio, of which 98% is in Core

businesses, comprises credit cards, unsecured loans and overdrafts

and totalled £18.1 billion at 31 December 2010 (2009 - £20.3 billion),

adecrease of 11% due to continued subdued loan recruitment

activity and a continuing general market trend of customers repaying

unsecured loan balances with cards and current account balances

remaining stable. The Non-Core portfolio consists of the direct

finance loan portfolios (Direct Line, Lombard, Mint and Churchill),

and totalled £0.45 billion at 31 December 2010 (2009 - £0.7 billion).

xRisk appetite continues to be actively managed across all products.

Support continues for customers experiencing financial difficulties

through “breathing space initiatives” on all unsecured products,

whereby a thirty day period is given to allow customers to establish

a debt repayment plan. During this time the Group suspends

collection activity. A further extension of thirty days can be granted if

progress is made and discussions are continuing. Investment in

collection and recovery processes continues, addressing both

continued support for the Group’s customers and the management

of impairments.

xBenefiting from a combination of risk appetite tightening and a more

favourable economic environment, impairment losses on unsecured

lending have reduced significantly during 2010 from £1,603 million

at 31 December 2009 to £991 million at 31 December 2010 with the

downward trajectory moderating significantly in the latter part of the

year. Impairments will remain sensitive to the external environment.

xIndustry benchmarks for cards arrears remain stable, with the Group

continuing to perform favourably.

xOutstanding balances for the Citizens credit card portfolio totalled

$1.53 billion at 31 December 2010. This figure excludes the Kroger

Personal Finance portfolio, which was sold on 27 May 2010. Core

assets comprised 86.3% of the portfolio.

xThe Citizens cards business has traditionally adopted conservative

risk strategies compared to the US market as a whole. Given the

economic climate, Citizens has over the past 24 months introduced

tighter lending criteria and lower credit limits. These actions have led

to improving new business quality and a business performing on par

with industry benchmarks (provided by VISA). The latest available

metrics show the rate for 60+ days delinquency as a percentage of

total outstanding balances at 3.17% in December 2010 (compared

to an industry figure of 3.22%) and net contractual charge-offs as a

percentage of total outstanding balances at 4.76% in December

2010 (compared to an industry figure of 5.67%). We expect further

improvement based on early delinquency trends.

xCitizens is a leading regional provider of retail auto financing to US

consumers through a network of 3,433 auto dealers located in 23

US states. Citizens maintain a conservative, prime indirect auto

lending credit programme with loss rates that have historically been

below national averages. Current outstanding retail auto loan

balances totalled $7.9 billion (includes Core and Non-Core) at 31

December 2010 of which 96% of the portfolio is in the Core business.

The $324 million of Non-Core auto assets are anticipated to run-off

by 2013. The tightening of credit parameters in 2008-09, along with

enhanced collection activities and seasonal factors, has resulted in

improved credit performance. The net charge-off rate on the total

auto portfolio fell to 0.34% at 31 December 2010, down from 1.3% at

31 December 2009. The 30+ DPD delinquency rate fell from 2.6%

as of 31 December 2009 to 1.6% at 31 December 2010 even as

balances fell by $917 million. The 1.7% 30+ DPD delinquency rate

on the total auto loan portfolio at 30 September 2010 Citizens was

favourable to the 2.6% nationwide bank indirect auto delinquency

rate as reported by Experian.

*unaudited

RBS Group 2010160

Business review continued