RBS 2010 Annual Report Download - page 350

Download and view the complete annual report

Please find page 350 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

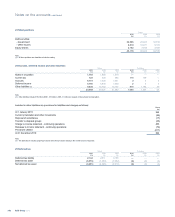

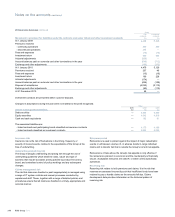

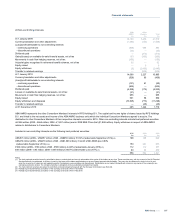

26 Insurance business continued

Loss ratios

The following table shows loss ratios for each major class of business, gross and net of reinsurance.

2010 2009 2008

Earned

premiums

Claims

incurred

Loss

ratio

Earned

premiums

Loss

ratio

Earned

premiums

Loss

ratio

£m £m % £m % £m %

Residential property Gross 1,168 643 55 1,129 53 1,103 48

Net 1,107 643 58 1,065 56 1,034 51

Personal motor Gross 2,829 3,530 125 2,984 103 3,173 84

Net

2,760 3,458 125 2,901 103 3,075 83

Commercial property Gross 187 106 57 182 41 194 41

Net

169 106 63 166 45 174 46

Commercial motor Gross 120 128 107 136 100 143 91

Net

119 124 104 135 98 141 91

Other Gross

837 374 45 848 51 994 42

Net

834 369 44 845 51 828 51

Total Gross

5,141 4,781 93 5,279 82 5,607 68

Net 4,989 4,700 94 5,112 83 5,252 71

Frequency and severity of specific risks and sources of uncertainty

Most general insurance contracts are written on an annual basis, which

means that the Group’s liability extends for a 12 month period, after

which the Group is entitled to decline or renew or can impose renewal

terms by amending the premium, terms and conditions, or both.

The frequency and severity of claims and the sources of uncertainty for

the key classes that the Group is exposed to are as follows:

Motor insurance contracts (personal and commercial)

Claims experience is quite variable, due to a wide range of factors, but

the principal ones are age, sex and driving experience of the driver, type

and nature of vehicle, use of vehicle and area.

There are many sources of uncertainty that will affect the Group’s

experience under motor insurance, including operational risk, reserving

risk, premium rates not matching claims inflation rates, weather, the

social, economic and legislative environment and reinsurance failure risk.

Property insurance contracts (residential and commercial)

The major causes of claims for property insurance are theft, flood,

escape of water, fire, storm, subsidence and various types of accidental

damage.

The major source of uncertainty in the Group’s property contracts is the

volatility of weather. Over a longer period, the strength of the economy is

also a factor.

Other commercial insurance contracts

Other commercial claims come mainly from business interruption and

loss arising from the negligence of the insured (liability insurance).

Business interruption losses come from the loss of income, revenue

and/or profit as a result of property damage claims. Liability insurance

includes employers’ liability and public/products’ liability. Liability

insurance is written on an occurrence basis, and is subject to claims that

are identified over a substantial period of time, but where the loss event

occurred during the life of the policy.

Fluctuations in the social and economic climate are a source of

uncertainty in the Group’s business interruption and general liability

accounts. Other sources of uncertainty are changes in the law, or its

interpretation, and reserving risk. Other uncertainties are significant

events (for example terrorist attacks) and any emerging new heads of

damage or types of claim that are not envisaged when the policy is

written.

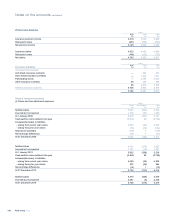

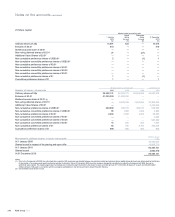

The following table shows the expected maturity of undiscounted

insurance liabilities up to 20 years, excluding those linked directly to the

financial assets backing these contracts (2010 - nil; 2009 - £4,175 million;

2008 - £4,189 million).

Group

0-3 months 3-12 months 1-3 years 3-5 years 5-10 years 10-20 years

£m £m £m £m £m £m

2010 724 1,503 1,821 898 734 442

2009 561 1,685 1,898 949 665 73

2008 623 1,645 1,899 903 487 53

RBS Group 2010348

Notes on the accounts continued