RBS 2010 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

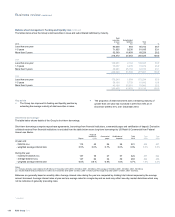

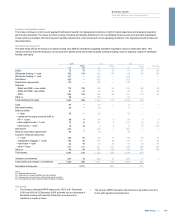

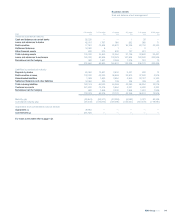

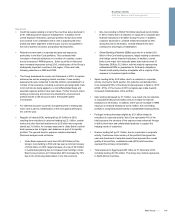

Risk management: Credit risk

All the disclosures in this section (pages 146 to 165) are audited unless

otherwise indicated by an asterisk (*).

Credit risk is the risk of financial loss owing to the failure of customers or

counterparties to meet payment obligations. The quantum and nature of

credit risk assumed across the Group's different businesses varies

considerably, while the overall credit risk outcome usually exhibits a high

degree of correlation to the macroeconomic environment.

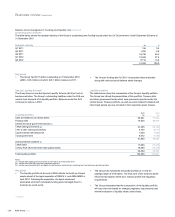

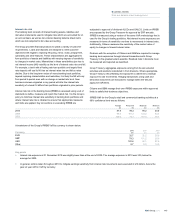

Credit risk organisation

The existence of a strong credit risk management organisation is vital to

support the ongoing profitability of the Group. The potential for loss

through economic cycles is mitigated through the embedding of a robust

credit risk culture within the business units and through a focus on the

importance of sustainable lending practices. The role of the credit risk

management organisation is to own the credit approval, concentration

and risk appetite frameworks and to act as the ultimate authority for the

approval of credit. This, together with strong independent oversight and

challenge, enables the business to maintain a sound lending environment

within risk appetite.

Responsibility for development of Group-wide policies, credit risk

frameworks, Group-wide portfolio management and assessment of

provision adequacy sits within the functional Group Credit Risk

organisation (GCR) under the management of the Group Chief Credit

Officer. Execution of these policies and frameworks is the responsibility of

the risk management organisations located within the Group’s business

divisions. These divisional credit risk functions work together with GCR to

ensure that the Board’s expressed risk appetite is met within a clearly

defined and managed control environment. Each credit risk function

within the division is managed by a Chief Credit Officer who reports jointly

to a divisional Chief Risk Officer and to the Group Chief Credit Officer.

Divisional activities within credit risk include credit approval, transaction

and portfolio analysis, early problem recognition and ongoing credit risk

stewardship.

GCR is additionally responsible for verifying compliance by the divisions

with all Group credit policies. It is assisted in this by a credit quality

assurance function owned by the Group Chief Credit Officer and housed

within the divisions.

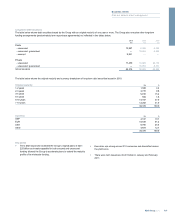

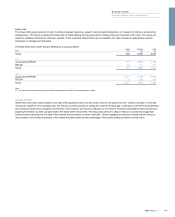

Credit risk appetite

Credit risk appetite is managed andcontrolled through a series of

frameworks designed to limit concentration by sector, counterparty,

country or asset class. These are supported by a suite of Group-wide and

divisional policies setting out the risk parameters within which business

units may operate. Information on the Group’s credit portfolios is reported

to the Board via the divisional and Group level risk committees detailed in

the Governance section on page 120.

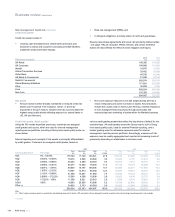

Product/asset class

xRetail: a formal risk appetite framework establishes Group-level

statements and thresholds that are cascaded through all retail

franchises in the Group and to granular business lines. These

include measures that relate to both aggregate portfolios and to

origination asset quality that are monitored frequently to ensure

consistency with Group standards and appetite. This appetite setting

and monitoring then informs the processes and parameters

employed in origination activities that require a large volume of small

scale credit decisions, typically involving an application for a new

product or a change in facilities on an existing product. The majority

of these decisions are based upon automated strategies utilising

credit and behaviour scoring techniques. Scores and strategies are

typically segmented by product, brand and other significant drivers

of credit risk. These data driven strategies utilise a wide range of

credit information relating to a customer including, where

appropriate, information across customers’ holdings. A small

number of credit decisions are subject to additional manual

underwriting by authorised approvers in specialist units. These

include higher value, more complex, small business and personal

unsecured transactions and some residential mortgage applications.

xWholesale: formal policies, specialised tools and expertise, tailored

monitoring and reporting and in certain cases specific limits and

thresholds are deployed to address certain lines of business across

the Group where the nature of credit risk incurred could represent a

concentration or a specific/heightened risk in some other form. Such

portfolios are subject to formal governance, including periodic review,

at either Group or divisional level, depending on materiality.

Sector

Across wholesale portfolios, exposures are assigned to, and reviewed in

the context of, a defined set of industry sectors. Through this sector

framework, appetite and portfolio strategies are agreed and set at

aggregate and more granular levels where exposures have the potential

to represent excessive concentration or where trends in both external

factors and internal portfolio performance give cause for concern. Formal

periodic reviews are undertaken at Group or divisional level depending on

materiality; these may include an assessment of the Group’s franchise in

aparticular sector, an analysis of the outlook (including downside

outcomes), identification of key vulnerabilities and stress/scenario tests.

Specific reporting on trends in sector risk and on status versus agreed

appetite and portfolio strategies is provided to senior management and to

the Board.

Single name

Within wholesale portfolios, much of the activity undertaken by the credit

risk function is organised around the assessment, approval and

management of the credit risk associated with a borrower or group of

related borrowers.

Aformal single name concentration framework addresses the risk of

outsized exposure to a borrower or borrower group. The framework

includes specific and elevated approval requirements; additional reporting

and monitoring; and the requirement to develop plans to address and

reduce excess exposures over an appropriate timeframe.

RBS Group 2010146

Business review continued