RBS 2010 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

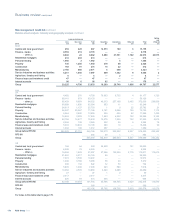

Risk management: Credit risk continued

Ulster Bank Group (Core and Non-Core)* continued

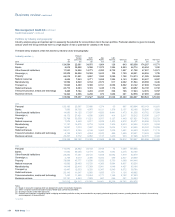

Residential mortgages

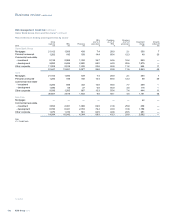

The table belowshows how the steep value correction has affected the distribution of residential mortgages by loan-to-value (LTV) (indexed). LTV is

based upon gross loan amounts and, whilst including defaulted loans, does not account for impairments already taken.

By average LTV (1) 2010

%

2009

%

2008

%

<= 50% 35.9 40.7 47.1

>50% and <= 70% 13.5 15.2 17.1

>70% and <= 90% 13.5 15.5 18.2

>90% 37.1 28.6 17.6

Total portfolio average LTV at 31 December 71.2 62.5 54.3

Average LTV on new originations during the year 75.9 72.8 71.1

Note:

(1) LTV averages calculated by transaction volume.

Key points

xThe residential mortgage portfolio across Ulster Bank Group totalled

£21.2 billion at 31 December 2010; with 90% in the Republic of

Ireland and 10% in Northern Ireland. The portfolio size has declined

by 4% in the Republic of Ireland since 31 December 2009 with

Northern Ireland increasing by 12% over the same period. New

business originations continue to be very low, especially in the

Republic of Ireland. In 2010, 3,557 new mortgages were originated

of which, 92% were in Northern Ireland.

xThe arrears rate continues to increase due to the continued

challenging economic environment. At 31 December 2010, the

arrears rate was 6.0%, compared to 3.3% at 31 December 2009. As

aresult, the impairment charge for 2010 was £336 million compared

with £116 million for 2009. Repossessions totalled 76 in 2010,

compared with 96 in 2009; 75% of the repossessions were voluntary.

xUlster Bank Group has a number of initiatives in place aimed at

increasing the level of support to customers experiencing temporary

financial difficulties. At 31 December 2010, forbearance

arrangements had been agreed in respect of 5.8% (£1.2 billion) of

Ulster Bank Group’s residential mortgage portfolio. The majority

(79%) relates to customers in the performing book. Loans in respect

of which forbearance arrangements were agreed during 2010

amounted to £1.7 billion in the performing book and £0.5 billion in

the impaired book.

*unaudited

RBS Group 2010164

Business review continued