RBS 2010 Annual Report Download - page 322

Download and view the complete annual report

Please find page 322 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

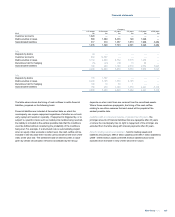

12 Financial instruments - valuation continued

Commercial mortgage backed securities

CMBS are valued using an industry standard model and the inputs,

where possible, are corroborated using observable market data.

Collateralised debt obligations

CDOs purchased from third-parties are valued using independent, third-

party quotes or independent lead manager indicative prices. For super

senior CDOs which have been originated by the Group no specific third-

party information is available. The valuation of these super senior CDOs

therefore takes into consideration outputs from a proprietary model,

market data and appropriate valuation adjustments.

Acollateral net asset value methodology using dealer buy side marks is

used to determine an upper bound for super senior CDO valuations. An

ABS index implied collateral valuation is also used to provide a market

calibrated valuation data point. Both the ABS index implied valuation and

the collateral net asset value methodology apply an assumed immediate

liquidation approach.

Collateralised loan obligations

To determine the fair value of CLOs purchased from third parties, the

Group uses third-party broker or lead manager quotes as the primary

pricing source. These quotes are benchmarked to consensus pricing

sources where they are available.

For CLOs originated and still held by the Group, the fair value is

determined using a correlation model based on a Monte Carlo simulation

framework. The main model inputs are credit spreads and recovery rates

of the underlying assets and their correlation. A credit curve is assigned

to each underlying asset based on prices from third-party dealer quotes

and cash flow profiles, sourced from an industry standard model. Losses

are calculated taking into account the attachment and detachment point

of the exposure. Where the correlation inputs to this model are not

observable, CLOs are classified as level 3.

Other asset-backed and corporate debt securities

Where observable market prices for a particular debt security are not

available, the fair value will typically be determined with reference to

observable market transactions in other related products, such as similar

debt securities or credit derivatives. Assumptions are made about the

relationship between the individual debt security and the available

benchmark data. Where significant management judgment has been

applied in identifying the most relevant related product, or in determining

the relationship between the related product and the instrument itself, the

instrument is classified as level 3.

Equity shares

Private equityinvestments include unit holdings and limited partnership

interests primarily in corporate private equity funds, debt funds and fund

of hedge funds. Externally managed funds are valued using recent prices

where available. Where not available, the fair value of investments in

externally managed funds is generally determined using statements or

other information provided by the fund managers.

The Group considers that valuations may rely significantly on the

judgments and estimates made by the fund managers, particularly in

assessing private equity components. Given the decline in liquidity in

world markets, and the level of subjectivity, these are included in level 3.

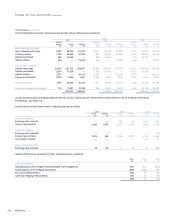

Derivatives

Derivatives are priced using quoted prices for the same or similar

instruments where these are available. However, the majority of

derivatives are valued using pricing models. Inputs for these models are

usually observed directly in the market, or derived from observed prices.

However, it is not always possible to observe or corroborate all model

inputs. Unobservable inputs used are based on estimates taking into

account a range of available information including historic analysis,

historic traded levels, market practice, comparison to other relevant

benchmark observable data and consensus pricing data.

Credit derivatives - APS

The Group purchased credit protection over a portfolio of specified assets

and exposures (covered assets) from HMT. The Group has a right to

terminate the APS at any time provided that the Financial Services

Authority has confirmed in writing to HMT that it has no objection to the

proposed termination. On termination the Group must pay HMT the

higher of the regulatory capital relief received and £2.5 billion less

premiums paid plus the aggregate of amounts received from the UK

Government under the APS. In consideration for the protection provided

by the APS, the Group paid an initial premium of £1.4 billion on 31

December 2009. A further premium of £700 million was paid on 31

December 2010. Quarterly premiums of £125 million will be payable from

31 December 2011 and subsequently until the earlier of 2099 and the

termination of the agreement.

The APS is a single contract providing credit protection in respect of the

covered assets. Under IFRS, credit protection is treated either as a

financial guarantee contract or as a derivative financial instrument

depending on the terms of the agreement and the nature of the protected

assets and exposures. The Group has concluded, principally because the

covered portfolio includes significant exposure in the form of derivatives,

that the APS does not meet the criteria to be treated as a financial

guarantee contract. The contract has therefore been accounted for as a

derivative financial instrument. It was recognised initially and measured

subsequently at fair value with changes in fair value recognised in profit

or loss within income from trading activities. There is no change in the

recognition and measurement of the covered assets as a result of the

APS.

Where protection is provided on a particular seniority of exposure, as is

the case with the APS, which requires initial losses to be taken by the

Group, it is termed ‘tranched’ protection. The model being used to value

the APS - a Gaussian Copula model with stochastic recoveries - is used

by the Group to value tranches traded by the exotic credit desk and is a

model that is currently used within the wider market.

The option to exit the APS is not usually present in such tranched trades

and consequently, there is no standard market practice for reflecting this

part of the trade within the standard model framework. The approach that

has been adopted assumes that the Group will not exit the trade before

the minimum level of fees has been paid and at this point it will be clear

whether it should exit the trade or not. The APS derivative is valued as

the payment of the minimum level of fees in return for protection receipts

which are in excess of both the first loss and the total future premiums.

RBS Group 2010320

Notes on the accounts continued