RBS 2010 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

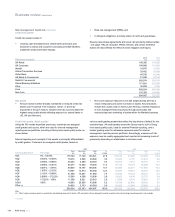

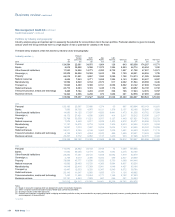

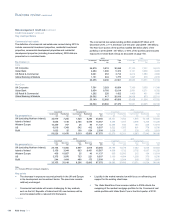

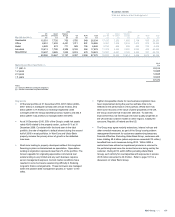

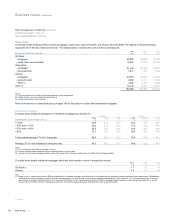

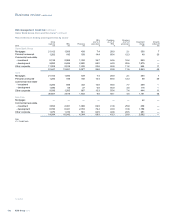

Key points

xExposure reductions occurred across most industry sectors and

geographic regions.

xModest growth in North America is attributable to the weakening of

sterling against the US dollar during the period and higher short-

term exposures to central banks.

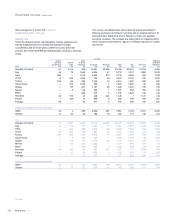

xAt 9.6% of total exposure, the banks sector is one of the largest in

the Group, although it is geographically diversified with activities

conducted in the Group's key markets across the world. Exposure is

predominantly to major global banks (23% of sector exposure),

defined as those with diversified domestic and international activities.

The product range is diverse and includes loans and advances,

treasury and capital markets products. Overall there has been a

gradual downward trend in exposures to banks, but exposures have

fluctuated markedly due to lines being drawn and repaid over short

periods and mark to market movements associated with trading

activity. Overall asset quality has stabilised in line with improving

economic conditions, although the sovereign crisis affecting several

eurozone countries has placed downward pressure on the asset

quality of banks in these countries (11% of sector exposure).

xExposures to the non bank financial sector are dominated by traded

products and spread across a wide range of financial institutions

including insurance companies, securitisations, financial

intermediaries, finance companies, unleveraged and leveraged

funds (including hedge funds). The majority of these are domiciled in

the UK, Western Europe and US with no other material geographic

or sector concentrations and business is developed selectively.

Asset quality has stabilised as the economic environment has

improved. Exposures to defaulted entities totalled £1.8 billion, 3% of

total exposure to this sector.

xSovereigns comprise activities with central governments, central

banks and sub sovereigns such as local authorities in the Group's

key markets in the UK, Western Europe and USA. The Group’s

exposure to sovereigns fluctuates according to the Group's liquidity

requirements and cash positions which determine the level of cash

placed with sovereign entities. The asset quality of the portfolios has

been impacted by the sovereign crisis in several eurozone countries

and the resultant multiple downgrading of these countries.

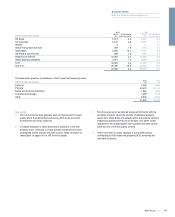

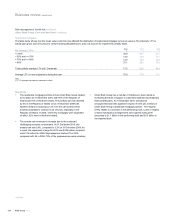

xThe Group’s exposure to the property sector totals £114 billion, a

reduction of 11% in the period, of which 76% is commercial real

estate (further detail on pages 156 and 157). The remainder

comprises lending to property-related sectors including housing

associations, estate agents and management companies. The

majority of property (with the exception of Non-Core) is within the

UK Corporate division (33%) and Ulster Bank (6%).

xExposure to the manufacturing sector is concentrated in the

industrial (40%), agriculture (24%) and food & consumer (21%) sub-

sectors. The overall reduction in exposure of £10.9 billion is partly

due to the run-off and restructuring of assets in Western Europe and

in the Non-Core portfolio. Portfolio asset quality has held up well

during the year but fluctuating commodity prices continue to pose a

key risk to the more cyclical sub-sectors. Manufacturing exposure in

default totals £1.5 billion (2009 - £3.7 billion).

xThe transport sector accounts for 6% of exposure and primarily

comprises loans and advances to borrowers in the shipping,

automotive and aviation segments in the Core bank. Aviation Capital

and a portfolio of shipping loans are held within Non-Core. Core

bank exposure resides primarily in Corporate Banking and Global

Banking & Markets and the portfolio is well diversified

geographically. In aggregate, the exposure within and asset quality

of the Core portfolio remained stable over the year. Global economic

conditions and related trends in trade flows and discretionary

consumer spending continue to inform the Group’s cautious stance.

Transport exposure in default totals of £1.7 billion (2009 - £1 billion).

xWhilst there have been no material impairment charges for shipping

to date, the exposure that is subject to a heightened level of

monitoring currently stands at approximately £2.8 billion out of a

total portfolio of £13 billion, which reflects the continued difficult

market conditions that have been experienced during 2010. Recent

quarterly vessel valuations undertaken by external shipbrokers show

that the majority of our exposures remain fully secured. Conditions

will remain challenging for the foreseeable future.

155RBS Group 2010

Business review

Risk and balance sheet management