RBS 2010 Annual Report Download - page 319

Download and view the complete annual report

Please find page 319 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

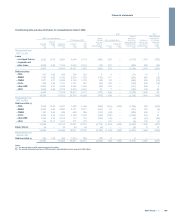

|

|

2010 2009

Sensitivity (2) Sensitivity (2)

Balance Favourable Unfavourable

Balance Favourable Unfavourable

£bn £m £m

£bn £m £m

Assumptions

Liabilities

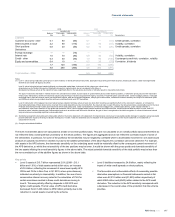

Customer accounts - other 0.1 60 (60) 0.1 — (10) Credit spreads, correlation

Debt securities in issue 2.2 90 (110) 2.3 50 (10) Volatility, correlation

Short positions 0.8 20 (50) 0.2 10 (20) Credit spreads, correlation

Derivatives

Foreign exchange — — (10) — — —

Interest rate 1.0 70 (90) 0.8 40 (60) Volatility, correlation

Credit - other 0.3 40 (40) 1.0 80 (100) Counterparty credit risk, correlation, volatility

Equity and commodities 0.4 10 — 0.2 20 (70) Correlation, dividends

1.7 120 (140) 2.0 140 (230)

4.8 290 (360) 4.6 200 (270)

Total liabilities - 2008 9.0 550 (490)

Notes:

(1) Level 1: valued using unadjusted quoted prices in active markets, for identical financial instruments. Examples include G10 government securities, listed equity shares, certain exchange-traded

derivatives and certain US agency securities.

Level 2: valued using techniques based significantly on observable market data. Instruments in this category are valued using:

(a) quoted prices for similar instruments or identical instruments in markets which are not considered to be active; or

(b) valuation techniques where all the inputs that have a significant effect on the valuations are directly or indirectly based on observable market data.

The type of instruments that trade in markets that are not considered to be active, but are based on quoted market prices, banker dealer quotations, or alternative pricing sources with reasonable

levels of price transparency and those instruments valued using techniques include most government agency securities, investment-grade corporate bonds, certain mortgage products, most bank

and bridge loans, repos and reverse repos, less liquid listed equities, state and municipal obligations, most physical commodities, investment contracts issued by the Group's life assurance (2009

and 2008) and certain money market securities and loan commitments and most OTC derivatives.

Level 3: instruments in this category have been valued using a valuation technique where at least one input which could have a significant effect on the instrument’s valuation, is not based on

observable market data. Where inputs can be observed from market data without undue cost and effort, the observed input is used. Otherwise, the Group determines a reasonable level for the input.

Financial instruments primarily include cash instruments which trade infrequently, certain syndicated and commercial mortgage loans, unlisted equity shares, certain residual interests in

securitisations, super senior tranches of high grade and mezzanine CDOs, other mortgage-based products and less liquid debt securities, certain structured debt securities in issue, and OTC

derivatives where valuation depends upon unobservable inputs such as certain credit and exotic derivatives. No gain or loss is recognised on the initial recognition of a financial instrument valued

using a technique incorporating significant unobservable data.

(2) Sensitivity represents the favourable and unfavourable effect on the income statement or the statement of comprehensive income due to reasonably possible changes to valuations using reasonably

possible alternative inputs to the Group's valuation techniques or models. Totals for sensitivities are not indicative of the total potential effect on the income statement or the statement of

comprehensive income.

(3) Comprise subordinated liabilities.

The level 3 sensitivities above are calculated at a trade or low level portfolio basis. They are not calculated on an overall portfolio basis and therefore do

not reflect the likely overall potential uncertainty on the whole portfolio. The figures are aggregated and do not reflect the correlated nature of some of

the sensitivities. In particular, for some of the portfolios the sensitivities may be negatively correlated where a downwards movement in one asset would

produce an upwards movement in another, but due to the additive presentation of the above figures this correlation cannot be observed. For example,

with assets in the APS scheme, the downwards sensitivity on the underlying asset would be materially offset by the consequent upward movement of

the APS derivative, so whilst the net sensitivity of the two positions may be lower, it would be shown with the gross upside and downside sensitivity of

the two assets inflating the overall sensitivity figures in the above table. The actual potential downside sensitivity of the total portfolio may be less than

the non-correlated sum of the additive figures as shown in the above table.

Key points

xLevel 3 assets of £15.7 billion represented 2.0% (2009 - £13.1

billion and 1.6%) of total assets carried at fair value, an increase

of £2.6 billion, reflecting the movement of some lower quality AFS

CDOs and CLOs in Non-Core in Q1 2010, where price discovery

indicated uncertainty in observability. In addition, the use of more

conservative internal recovery rates for the calculation of CVA for

certain monolines resulted in these credit derivatives moving to

level 3. This was partially offset by disposals in Q3 2010 and

tighter credit spreads. The fair value of APS credit derivative

decreased from £1,400 million to £550 million primarily due to the

reduction in overall assets covered by the scheme.

xLevel 3 liabilities increased to £4.8 billion, mainly reflecting the

impact of wider credit spreads on short positions.

xThe favourable and unfavourable effects of reasonably possible

alternative assumptions on financial instruments carried at fair

value were £2,310 million and (£1,820) million respectively of

which £860 million and (£940) million related to the APS credit

derivative. The reduction in the APS sensitivity corresponds with

adecrease in the overall value of the protection that the scheme

provides.

317RBS Group 2010

Financial statements