RBS 2010 Annual Report Download - page 288

Download and view the complete annual report

Please find page 288 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

283 -

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Accounting developments

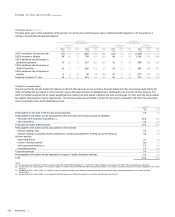

International Financial Reporting Standards

The IASB issued ‘Improvements to IFRS’ in May2010 implementing

minor changes to IFRS, making non-urgent but necessary amendments

to standards, primarily to remove inconsistency and to clarify wording.

The revisions are effective for annual periods beginning on or after 1 July

2010 and are not expected to have a material effect on the Group or the

company.

The IASB issued IFRS 9 ‘Financial Instruments’ in November 2009

simplifying the classification and measurement requirements in IAS 39

‘Financial Instruments: Recognition and Measurement’ in respect of

financial assets. The standard reduces the measurement categories for

financial assets to two: fair value and amortised cost. A financial asset is

classified on the basis of the entity's business model for managing the

financial asset and the contractual cash flow characteristics of the

financial asset. Only assets with contractual terms that give rise to cash

flows on specified dates that are solely payments of principal and interest

on the principal amount outstanding and which are held within a business

model whose objective is to hold assets in order to collect contractual

cash flows are classified as amortised cost. All other financial assets are

measured at fair value. Changes in the value of financial assets

measured at fair value are generally taken to profit or loss.

In October 2010, IFRS 9 was updated to include the classification and

measurement of liabilities. It is not markedly different from IAS 39 except

for liabilities measured at fair value where the movement is due to

changes in credit rating of the preparer it is recognised not in profit or loss

but in other comprehensive income.

The standard is effective for annual periods beginning on or after 1

January 2013; early application is permitted.

This standard makes major changes to the framework for the

classification and measurement of financial assets and will have a

significant effect on the Group's financial statements. The changes

relating to the classification and measurement of liabilities carried at fair

value will have a less significant effect on the Group. The Group is

assessing these impacts which are likely to depend on the outcome of

the other phases of IASB's IAS 39 replacement project.

The IASB issued ‘Disclosures - Transfers of Financial Assets

(Amendments to IFRS 7 Financial Instruments: Disclosures)’ in October

2010 to extend the standard’s disclosure requirements about

derecognition to align with US GAAP. The revisions are effective for

annual periods beginning on or after 1 July 2011 and will not affect the

financial position or reported performance of the Group or the company.

The IASB issued an amendment to IAS 12 ‘Income Taxes’ in December

2010 to clarify that recognition of deferred tax should have regard to the

expected manner of recovery or settlement of the asset or liability. The

amendment and consequential withdrawal of SIC 21 ‘Deferred Tax:

Recovery of Underlying Assets’, effective for annual periods beginning on

or after 1 January 2012, is not expected to have a material effect on the

Group or the company.

The International Financial Reporting Interpretations Committee issued

IFRIC 19 ‘Extinguishing Financial Liabilities with Equity Instruments’ in

December 2009. The interpretation clarifies that the profit or loss on

extinguishing liabilities by issuing equity instruments should be measured

by reference to fair value, preferably of the equity instruments. The

interpretation, effective for the Group for annual periods beginning on or

after 1 January 2011, is not expected to have a material effect on the

Group or the company.

RBS Group 2010286

Accounting policies continued