RBS 2010 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

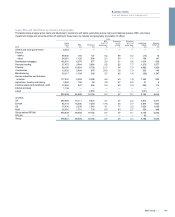

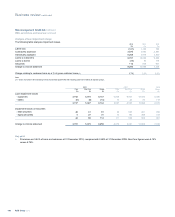

Market risk

All the disclosures in this section (pages 193 to 198) are audited unless

indicated otherwise with an asterisk (*).

Market risk arises from changes in interest rates, foreign currency, credit

spread, equity prices and risk related factors such as market volatilities.

The Group manages market risk centrally within its trading and non-

trading portfolios through a comprehensive market risk management

framework. This framework includes limits based on, but not limited to,

value-at-risk (VaR), stress testing, positions and sensitivity analyses.

The majority of market risk exposure is in GBM and Non-Core. The

Group is also exposed to market risk through interest rate risk on its non-

trading activities. There are additional non-trading market risks in the

Retail and Commercial businesses of the Group, principally interest rate

risk and foreign exchange risk. These aspects are discussed in more

detail in Balance sheet management - Interest rate risk on page 143 and

structural foreign currency exposures on page 144.

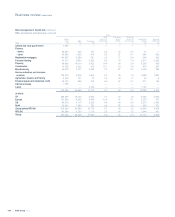

Organisation and structure

The Executive Risk Forum approves market risk appetite for trading and

non-trading activities. The Global Head of Market & Insurance Risk is

responsible for the Group Market Risk Control Framework and under

delegated authority from the Executive Risk Forum, sets a limit

framework within the context of the approved market risk appetite, which

is cascaded down through legal entity, division, business and desk level

market risk limits.

Adaily report summarises the Group’s market risk exposures against

agreed limits. This daily report is sent to the Head of Restructuring & Risk,

Global Head of Market & Insurance Risk, business Chief Risk Officers

and appropriate business Risk Managers.

The head of each business, assisted by the business risk management

team, is accountable for all market risks associated with its activities.

Oversight and support is provided to the business by the Global Head of

Market & Insurance Risk, assisted by the Group and business Market

Risk teams. The Global Market Risk Committee reviews and makes

recommendations concerning the market risk profile across the Group,

including risk appetite, limits and utilisation. The Committee meets

monthly and is chaired by the Global Head of Market Risk & Insurance

Risk. Attendees include respective business Risk Managers and Group

Market Risk.

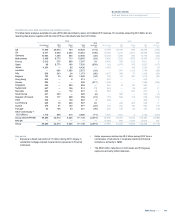

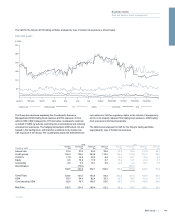

Risk measurement and control

At the Group level, the risk appetite is expressed in the form of a

combination of VaR, sensitivity and stress testing limits. VaR is a

technique that produces estimates of the potential change in the market

value of a portfolio over a specified time horizon at given confidence

levels. For internal risk management purposes, the Group’s VaR

assumes a time horizon of one trading day and a confidence level of 99%.

The Group's VaR model is based on a historical simulation model,

utilising data from the previous two years.

The VaR model has been approved by the FSA to calculate regulatory

capital for the trading book. The approval covers general market risk in

interest rate, foreign exchange, equity and limited commodity products

and specific risk in interest rate and equity products.

As the VaR model is an important market risk measurement and control

tool and is used for determining a significant component of the market

risk capital, it is regularly assessed. The main approach employed is the

technique known as back-testing which counts the number of days when

aloss (as defined by the FSA), exceeds the corresponding daily VaR

estimate, measured at a 99% confidence interval. The FSA categorises a

VaR model as green, amber or red. A green model is consistent with a

good working model and is achieved for models that have four or less

back-testing exceptions in a 12 month period. For the Group’s trading

book, a green model status was maintained throughout 2010.

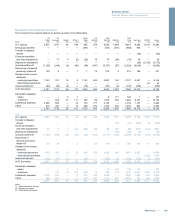

The Group’s VaR should be interpreted in light of the limitations of the

methodology used, as follows:

xHistorical Simulation VaR may not provide the best estimate of

future market movements. It can only provide a prediction of the

future based on events that occurred in the 500 trading day time

series. Therefore, events that are more severe than those in the

historical data series cannot be predicted.

xThe use of a 99% confidence level does not reflect the extent of

potential losses beyond that percentile.

xThe use of a one-day time horizon will not fully capture the profit and

loss implications of positions that cannot be liquidated or hedged

within one day.

xThe Group computes the VaR of trading portfolios at the close of

business. Positions may change substantially during the course of

the trading day and intra-day profit and losses will be incurred.

These limitations mean that the Group cannot guarantee that losses will

not exceed the VaR.

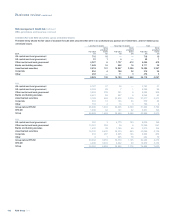

Arisk not in VaR framework has been developed to quantify those

market risks not adequately captured by the market standard VaR

methodology. Where risks are not included in the model, various non-

VaR controls (for example, position monitoring, sensitivity limits, triggers

or stress limits) are in place.

The Group undertakes daily stress testing to identify the potential losses

in excess of VaR. Stress testing is used to calculate a range of trading

book exposures which result from extreme market events. Stress testing

measures the impact of exceptional changes in market rates and prices

on the fair value of the Group’s trading portfolios. The Group calculates

historical stress tests and hypothetical stress tests.

Historical stress tests calculate the loss that would be generated if the

market movements that occurred during historical market events were

repeated. Hypothetical stress tests calculate the loss that would be

generated if a specific set of adverse market movements were to occur.

193RBS Group 2010

Business review

Risk and balance sheet management