RBS 2010 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

Business review continued

132 RBS Group 2010

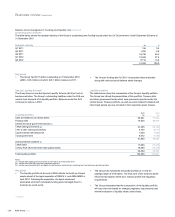

Balance sheet management: Capital* continued

Regulatory developments continued

Basel III capital deductions and regulatory adjustments

In addition to the changes outlined above, Basel III will also result in

revisions to regulatory adjustments and capital deductions. These will be

phased in over a five year period from 1 January 2014. The initial

deduction is expected to be 20%, rising 20 percentage points each year

until full deduction by 1 January 2018. However, this is subject to final

implementation rules determined by the FSA. The proportion not

deducted in the transition years will continue to be subject to existing

national treatments.

The major categories of deductions include:

xexpected loss net of provisions;

xdeferred tax assets not relating to timing differences;

xunrealised losses on available-for-sale securities; and

xsignificant investments in non-consolidated financial institutions.

The net impact of these adjustments is expected to be manageable as

most of these drivers reduce or are eliminated by 2014.

Other regulatory developments

Treatment of Systemically Important Financial Institutions (SIFIs)

Policy development around contingent capital and loss absorbency forms

part of a wider policy initiative on addressing systemic institutions. A

Financial Stability Board outline framework and plan of action was

endorsed by G20 leaders at the November 2010 Seoul Summit. This

now forms the main focus of global policy making following the

finalisation of the Basel III framework. Policy initiatives in this area may

include proposals for greater loss absorbency for systemic firms, the

development of enhanced supervision and resolution frameworks, as well

as recovery and resolution plans.

The EU Commission Consultation

Crisis management proposals

The EU Commission issued a consultation paper on crisis management

measures in January 2011. It covers prevention tools (such as recovery

planning requirements, supervisory powers and new ideas on intra-group

financial support mechanisms), as well as resolution tools (including

partial transfer powers and possible approaches to debt write-down. The

consultation will inform draft implementing legislation expected this

summer, and is intended to help shape the global framework for SIFIs.

Markets in Financial Instruments Directive Review

The EU Commission published a consultation on revising the Directive on

Markets in Financial Instruments (MiFID2). The main proposals in the

consultation are the extension of the transparency rules to include bonds

and over the counter derivatives, measures to reinforce regulation of

commodity derivatives and high frequency trading, strengthening investor

protection and detailing the role of the new European Securities and

Markets Authority.

Financial activities tax

In a recent speech, the EU Tax Commissioner talked about the

introduction of a potential Financial Activities Tax at a European level.

There will be an impact assessment in 2011 to review the cumulative

impact on financial institutions of new regulation, bank levy and taxes, as

part of the Commission's on-going examination of possible tax measures.

Dodd-Frank

In the United States the Dodd-Frank Wall Street Reform and Consumer

Reform Act (Dodd-Frank) contains very significant reforms the full effect

of which can only be assessed when the implementation rules are

finalised. There have also been numerous derivative proposals from the

Commodity Futures Exchange Commission (CFTC) and the Securities

and Exchange Commission (SEC) plus joint agency proposals to

implement minimum capital standards (Collins Amendment) and market

risk capital guidelines.

Project Merlin

On 9 February 2011, the UK Government and the major British banks

including the Group, announced the creation of an accord, known as

Project Merlin, aimed at demonstrating the clear and shared intent to

work together to help the UK economy recover and grow. The banks:

xwill work to foster credit demand, particularly among small and

medium-sized businesses, and will make available additional

lending capacity if demand should materialise above their current

expectations;

xexpect to contribute more in UK tax as their performance

strengthens and their profits grow and will jointly contribute an

additional £1 billion to the Business Growth Fund;

xconfirm that the aggregate 2010 bonus pool including deferrals for

their UK-based staff will be lower than that of 2009 and will reflect

the engagement each bank has had with the Financial Services

Authority, the UK Government and its shareholders, as well as their

duty to manage pay policy to protect and enhance the long-term

interests of shareholders; and

xwill extend disclosure of remuneration details of their most senior

executives beyond international norms.

The Government has in the light of the banks’ statements affirmed its

commitment to maintaining a strong, resilient, stable and globally

competitive UK financial services sector, and to implementing and

applying European and international regulation to create a level playing

field in both policy and practice.

*unaudited