RBS 2010 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

All the disclosures in this section (pages 199 to 203) are unaudited and

are marked with an asterisk (*).

Insurance risk*

Insurance risk arises through fluctuations in the timing, frequency and/or

severity of insured events, relative to the expectations at the time of

underwriting. Insurance risk is managed in four distinct ways:

xunderwriting and pricing risk management is managed through the

use of underwriting guidelines which detail the class, nature and

type of business that may be accepted, pricing policies by product

line and brand, and centralised control of wordings and any

subsequent changes;

xclaims risk management is handled using a range of automated

controls and manual processes;

xreserving risk management is applied to ensure that sufficient funds

have been retained to handle and pay claims as the amounts fall

due, both in relation to those claims which have already occurred or

will occur in future periods of insurance. Reserving risk is managed

through the detailed analysis of historical and industry claims data

and robust control procedures around reserving models; and

xreinsurance risk management is used to protect against adverse

claims experience on business which exceeds internal risk appetite.

The Group uses various types of reinsurance to transfer risk that is

outside the Group's risk appetite, including individual risk excess of

loss reinsurance, catastrophe excess of loss reinsurance and quota

share reinsurance.

Overall, insurance risk is predictable over time, given the large volumes

of data. However, uncertainty does exist, especially around predictions

such as the variations in weather for example. Risk is minimised through

the application of documented insurance risk policies, coupled with risk

governance frameworks and the purchase of reinsurance.

The Group underwrites retail and SME insurance with a focus on high

volume, relatively straightforward products. The key insurance risks are

as follows:

xmotor insurance contracts (private and commercial): claims

experience varies due to a range of factors, including age, gender

and driving experience together with the type of vehicle and location;

xproperty insurance contracts (residential and commercial): the major

causes of claims for property insurance are weather (flood, storm),

theft, fire, subsidence and various types of accidental damage; and

xother commercial insurance contracts: risk arises from business

interruption and loss arising from the negligence of the insured

(liability insurance).

Most general insurance contracts are written on an annual basis, which

means that the Group's liability extends for a twelve month period, after

which the Group is entitled to decline to renew the policy or can impose

renewal terms by amending the premium, terms and conditions.

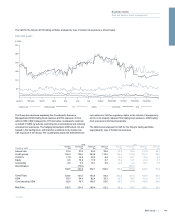

An analysis of gross and net insurance claims can be found in the notes

on the financial statements (see page 347).

Operational risk*

Operational risk is the risk of loss resulting from inadequate or failed

internal processes, people and systems, or from external events.

Operational risk is an integral and unavoidable part of the Group’s

business as it is inherent in the processes it operates in to provide

services to customers and generate profit for shareholders. An objective

of operational risk management is not to remove operational risk

altogether, but to manage the risk to an acceptable level, taking into

account the cost of minimising the risk as against the resultant reduction

in exposure. Strategies to manage operational risk include avoidance,

transfer, acceptance and mitigation by controls.

Group Policy Framework (GPF)

The GPF supports a consistent approach to how we do business and

helps everyone understand their individual and collective responsibilities.

It is a core component of the Group’s Risk Appetite Framework; it

supports the risk appetite setting process, and also underpins the control

environment.

Work to design, implement and embed an enhanced GPF has continued

throughout 2010 and will extend into 2011. The Group’s plans for ongoing

development of GPF will support increased consistency in risk appetite

setting across all risk types faced by the Group, including alignment to

the Group’s strategic business and risk objectives. The Group will use

relevant external reference points such as peers and rating agencies to

challenge and verify the content of the Policy Standards making up GPF.

Appropriate and effectively implemented Policy Standards are a

fundamental component of GPF and support attainment and

maintenance of an ‘upper quartile’ control framework as compared

against the Group’s relevant peer set.

The GPF requires consideration and agreement through Group

governance of the level of risk appetite we have and how this is justifiable

in the context of our strategic objectives.

There will be ongoing reassessment of risks, risk appetite and controls

within the GPF and where appropriate, potential issues will be identified

and addressed to ensure the Group moves in line with the set objectives

and remains constantly aligned with the ‘upper quartile’ objective and

market practice at all times.

*unaudited

199RBS Group 2010

Business review

Risk and balance sheet management