RBS 2010 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2010 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

|

|

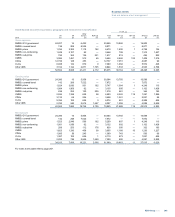

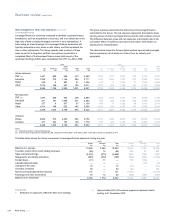

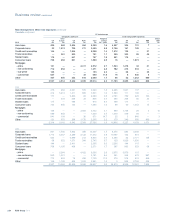

Risk management: Other risk exposures continued

Credit derivative product companies continued

The table belowdetails CDPC exposures by rating.

2010

Notional:

protected

assets

£m

Fair value:

reference

protected

assets

£m

Gross

exposure

£m

Credit

valuation

adjustment

£m

Net

exposure

£m

AAA 213 212 1 — 1

Ato AA- 644 629 15 4 11

Non-investment grade 20,066 19,050 1,016 401 615

Unrated 4,165 3,953 212 85 127

25,088 23,844 1,244 490 754

2009

AAA 1,658 1,637 21 5 16

BBB- to A- 1,070 1,043 27 9 18

Non-investment grade 17,696 16,742 954 377 577

Unrated 3,926 3,653 273 108 165

24,350 23,075 1,275 499 776

2008

AAA 6,351 4,780 1,571 314 1,257

AA to AA+ 1,195 1,116 79 16 63

Ato AA- 13,092 10,891 2,201 657 1,544

BBB- to A- 4,601 3,676 925 324 601

25,239 20,463 4,776 1,311 3,465

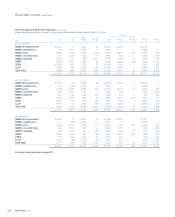

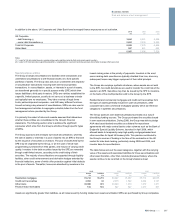

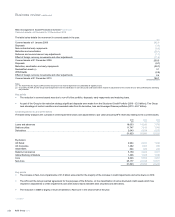

The table below details the net income statement effect arising from CDPC exposures.

2010 2009 2008

£m £m £m

Credit valuation adjustment at 1 January (499) (1,311) (44)

Credit valuation adjustment at 31 December (490) (499) (1,311)

Decrease/(increase) in credit valuation adjustment 9812 (1,267)

Net (debit)/credit relating to realisations, hedges, foreign exchange and other movements (150) (1,769) 652

Income from trading activities - net losses (141) (957) (615)

Key points

xLosses reduced significantly in 2010 due to smaller exposures and

reduced losses on hedges that were introduced to cap the

exposures.

xThe CVA decrease for the year reflected exposure reductions, due

to trade commutations, tighter credit spreads of the underlying

reference portfolios, partially offset by an increase in the relative

value of senior tranches compared with the underlying reference

portfolios and foreign currency movements.

xCounterparty and credit RWAs and capital deductions decreased in

line with the exposure.

xCertain CDPCs, where the Group has hedges in place to cap the

exposure, are excluded from the RWA calculations with capital

deduction taken instead.

Other counterparties

The CVA for all other counterparties is calculated on a portfolio basis

reflecting an estimate of the amount a third party would charge to assume

the credit risk.

Expected losses are determined from the market implied probability of

defaults and internally assessed recovery levels. The probability of

default is calculated with reference to observable credit spreads and

observable recovery levels. For counterparties where observable data do

not exist, the probability of default is determined from the average credit

spreads and recovery levels of baskets of similarly rated entities. A

weighting of 50% to 100% is applied to arrive at the CVA. The weighting

reflects portfolio churn and varies according to the counterparty credit

quality.

RBS Group 2010214

Business review continued